Global Market Analysis

Snap, Crackle, & Flop: Crude Shock, Petrochemical Capacity Chop

Key Findings

- General Thoughts: Global energy shocks, narrowing sanctioned crude oil discounts, and persistent olefin oversupply converge to lift marginal costs, accelerate restructuring, and benefit gas-advantaged producers.

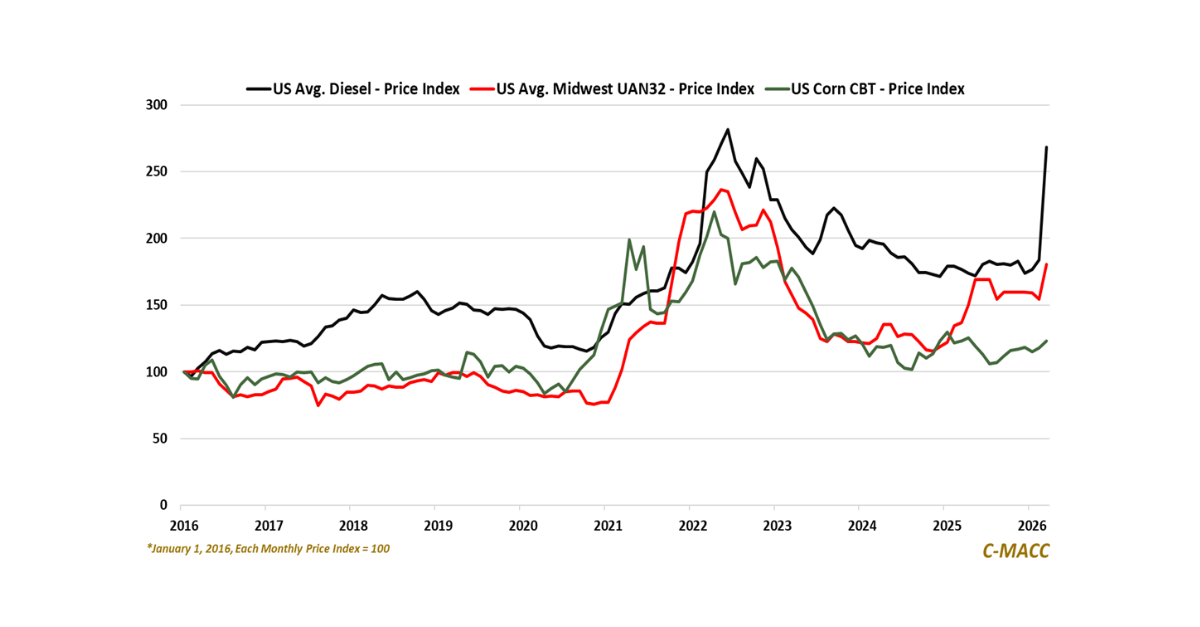

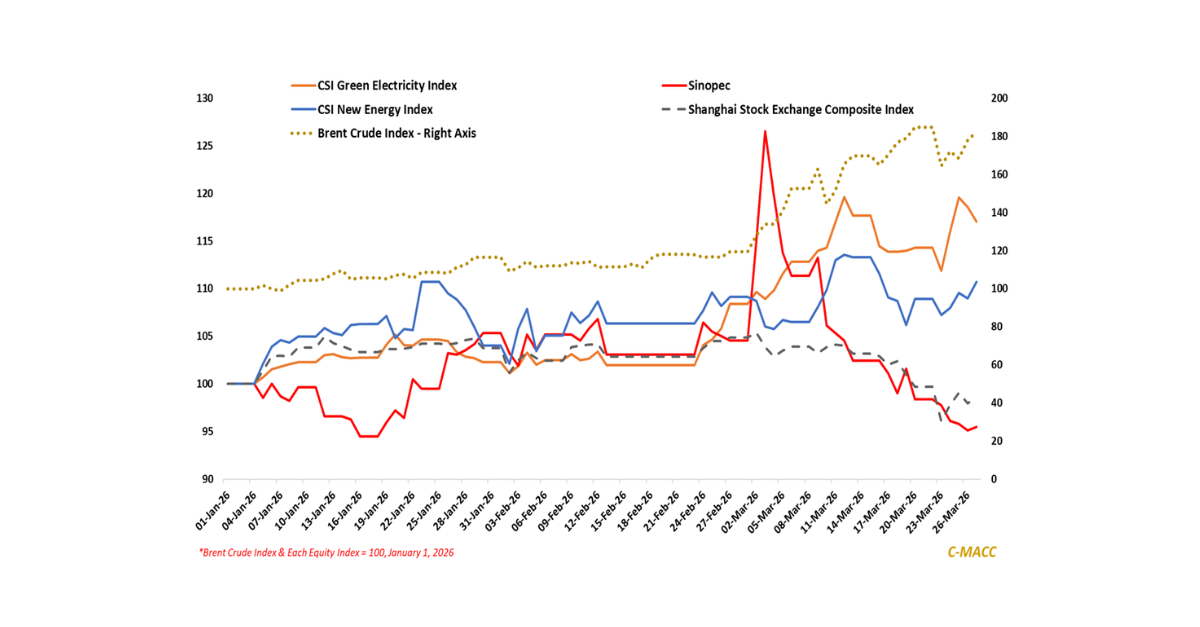

- Supply Chain/Commodities: Shrinking discounted crude flows push China higher on the global petrochemical cost curve, aligning its cost position with Asian and European naphtha crackers under margin pressure.

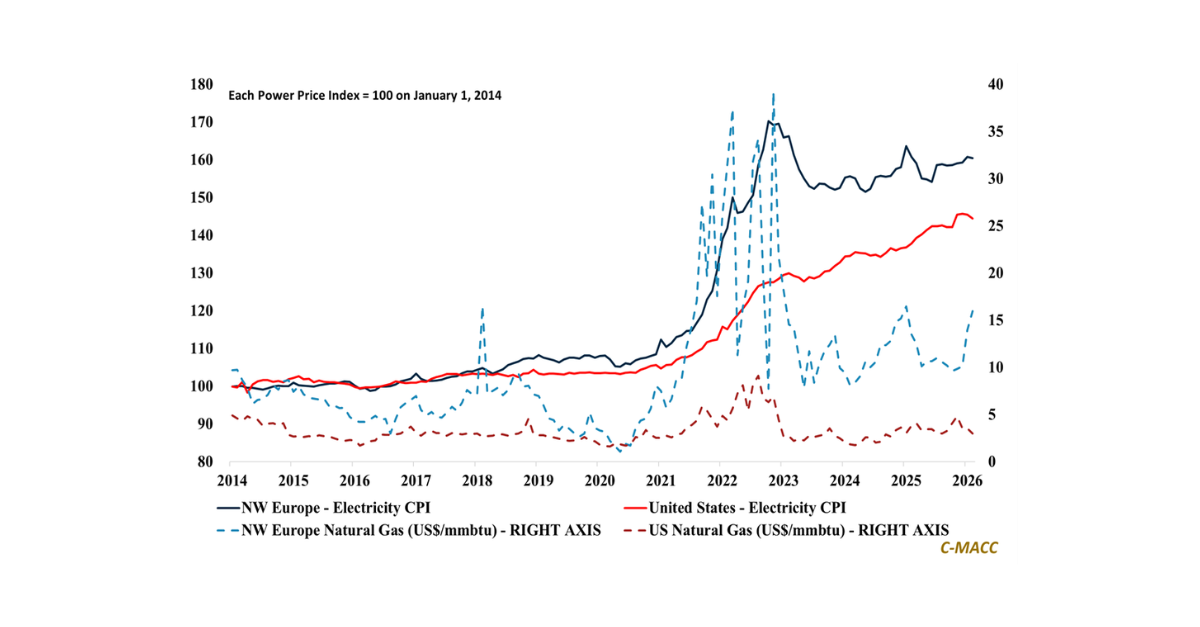

- Energy/Upstream: Global energy spreads have abruptly widened as shipping constraints and LNG rigidity prolong disruption, steepening chemical production cost curves and reinforcing higher price realizations.

- Sustainability/Energy Transition: Grid-scale storage growth and refining bottlenecks, not mine supply alone, will determine whether rising volumes cap lithium prices or sustain elevated volatility into late 2026.

- Downstream/Other Chemicals: US Dollar volatility has increased in 2026, yet widening energy spreads and feedstock differentials reinforce US competitive cost advantages despite episodic currency strength.

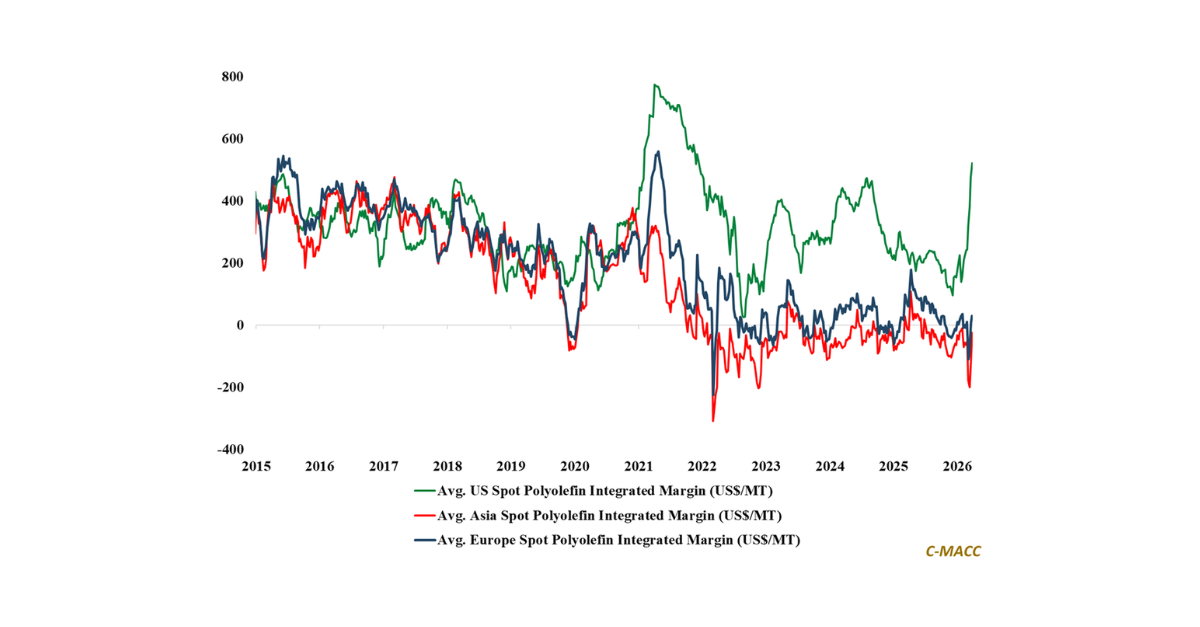

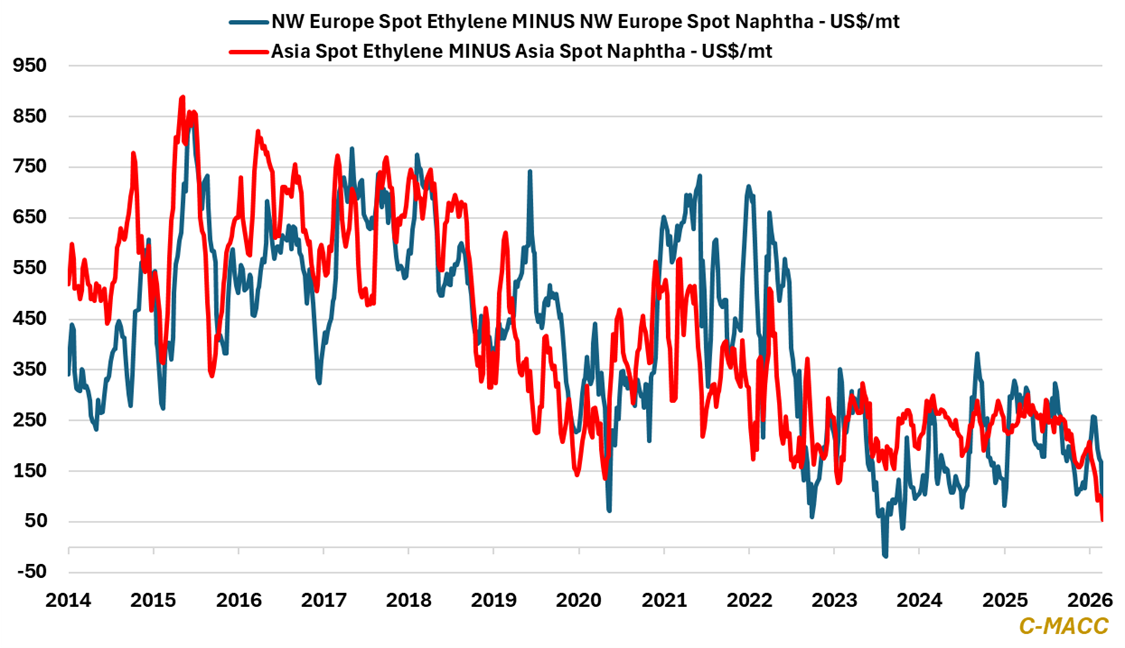

Exhibit 1: European and Asian spot ethylene-to-naphtha spreads plunge, intensifying restructuring discussions.

Source: Bloomberg, C-MACC Analysis, March 2026

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!