Global Market Analysis

Chemicals Duck and Cover: Broken Flexibility Locks in Global Cost Gaps, For Now

Key Findings

- General Thoughts: Escalating Middle East disruption scale is reducing system flexibility faster than it can be restored, shifting pricing power, capital allocation, and competitive positioning across global chemicals.

- Supply Chain/Commodities: Capital allocation selectivity, not demand alone, is driving restructuring, as volatile costs and uncertain returns constrain reinvestment across high-cost chemical systems globally.

- Energy/Upstream: Reduced LNG swing supply availability and constrained shipping capacity extend energy tightness, with disruption scale and supply reliability outweighing duration in determining cost structures.

- Sustainability/Energy Transition: EU carbon price weakness signals shift toward managed ETS, easing industrial costs while weakening decarbonisation incentives and delaying low-carbon investment globally.

- Downstream/Other Chemicals: Energy-driven freight inflation entrenches low-cost advantage, widens global cost gaps, and confines high-cost producers to domestic markets as export competitiveness erodes.

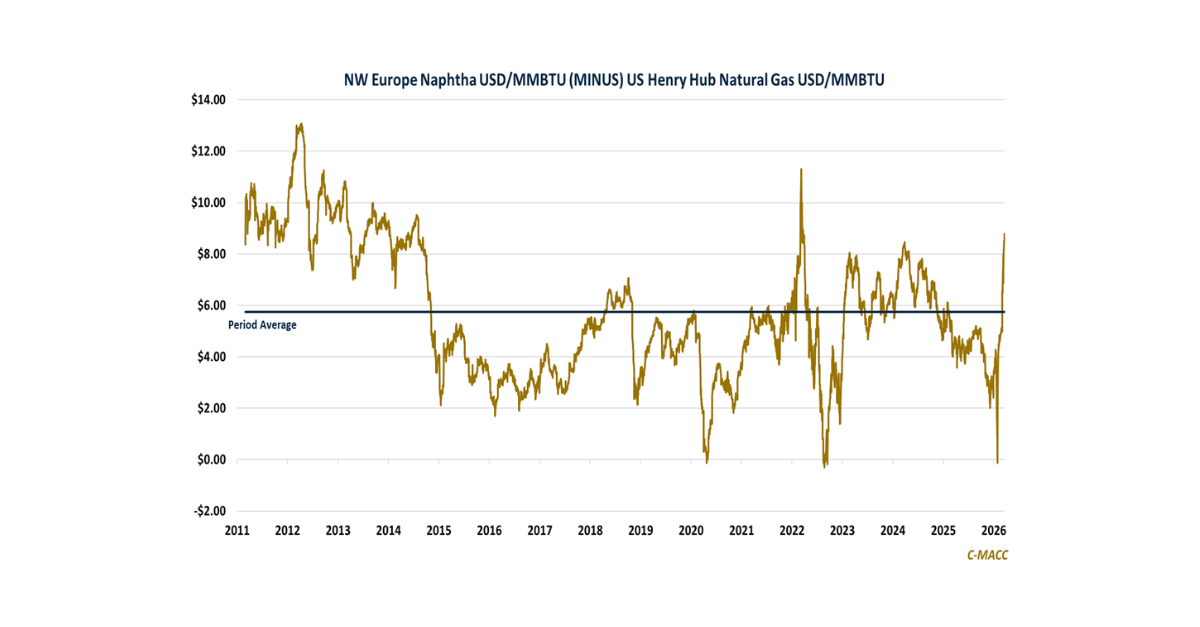

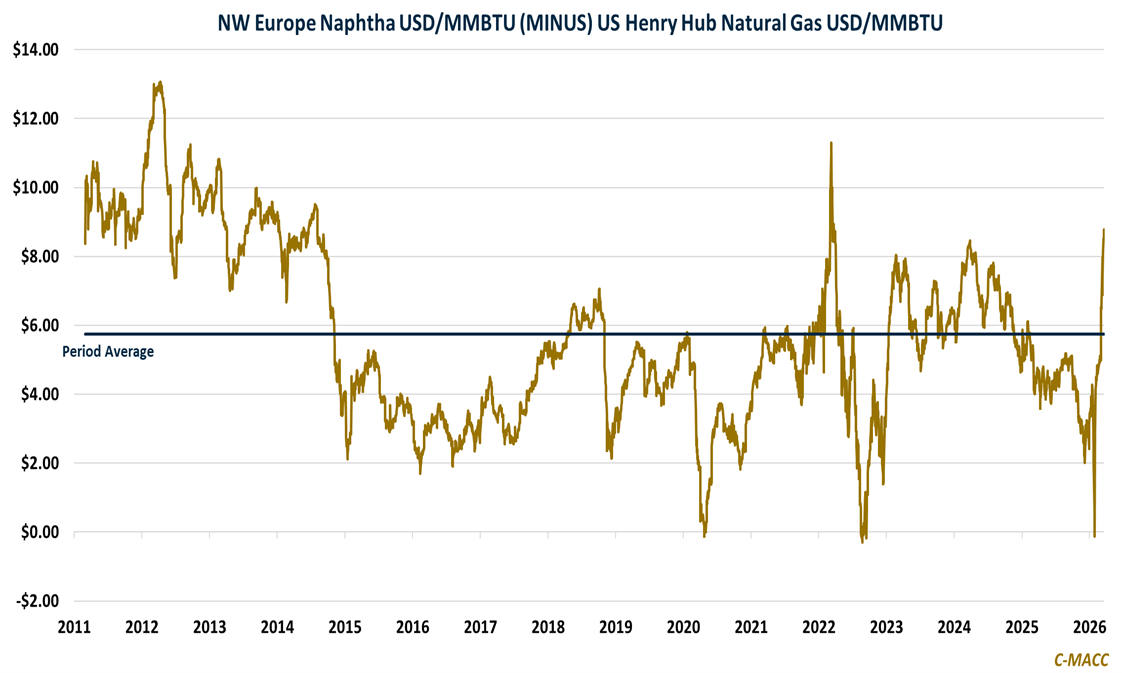

Exhibit 1: European naphtha price surge relative to US gas reflects persistent feedstock-driven cost divergence.

Source: C-MACC Analysis, March 2026

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!