Base Chemical Global Analysis

Global Weekly Catalyst No. 332

- General Thoughts: Global chemical markets remain fractured by feedstock access, credit quality, logistics control, and affordability, turning weak pricing power into restructuring pressure through 2026.

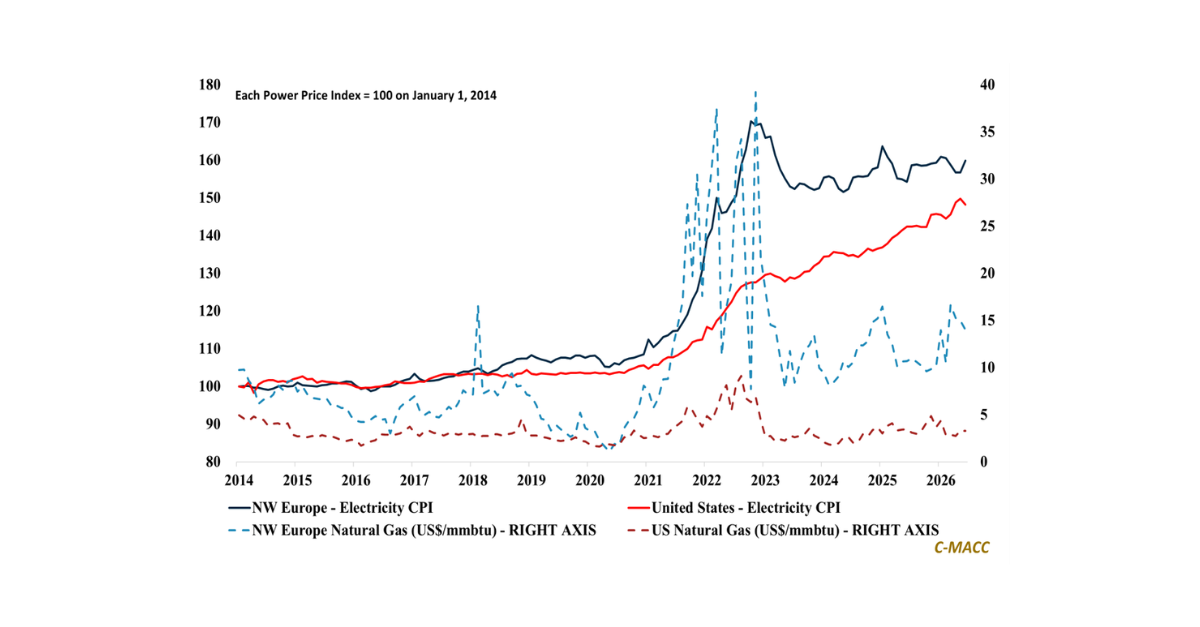

- Feedstocks & Energy: Asia’s feedstock inflation beyond coal is shifting access to low-cost gas, ethane, LPG, and naphtha from procurement preference to margin defense across exposed, import-dependent chemical chains.

- Olefins: Global olefins prices fell last week, but US export strength and NE Asian closures show weak margins are forcing capacity realism, not genuine global normalization, especially for exposed naphtha-based assets.

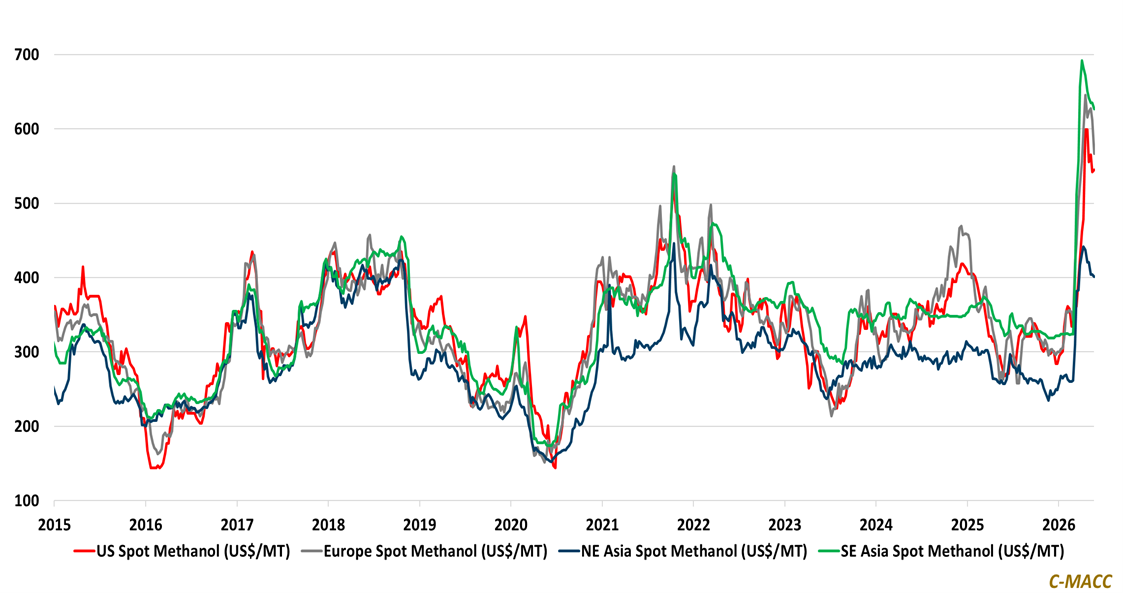

- Other Base Chemicals: Global base chemicals are splitting by supply quality, with benzene tied to refinery economics, methanol to outages, and credit stress exposing weak downstream absorption despite weaker spot pricing WoW.

- Agriculture: Global nitrogen’s scarcity premium has shifted from supply fear to affordability risk as tariff relief and phosphate cuts expose stress beneath firm prices across import-dependent buyers and farmers.

- Refining & Biofuels: Global refining margins are concentrating in coastal distillate exporters, as stronger ethanol margins and biofuel credits add upside without removing feedstock risk.

Exhibit 1 – Chart of the Day: Methanol’s regional spreads show supply access is repricing value-chain risk.

Source: C-MACC Estimates, May 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!