Global Market Analysis

No Free Flow: Gas, Power, Freight, and the Fight to Capture the Spread

Key Findings

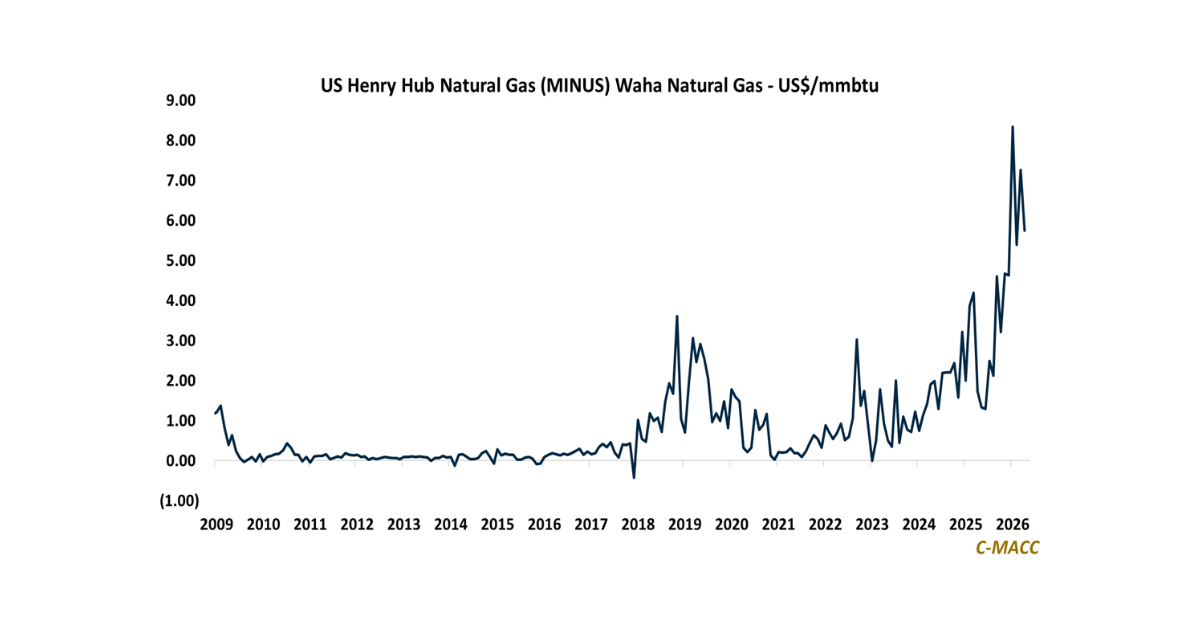

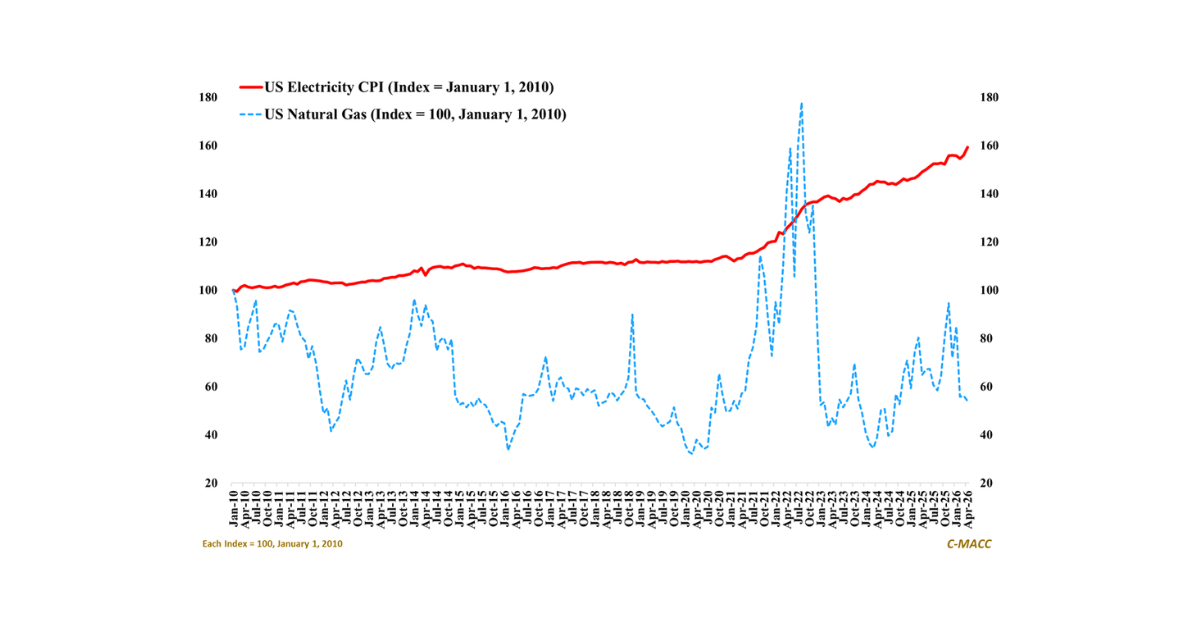

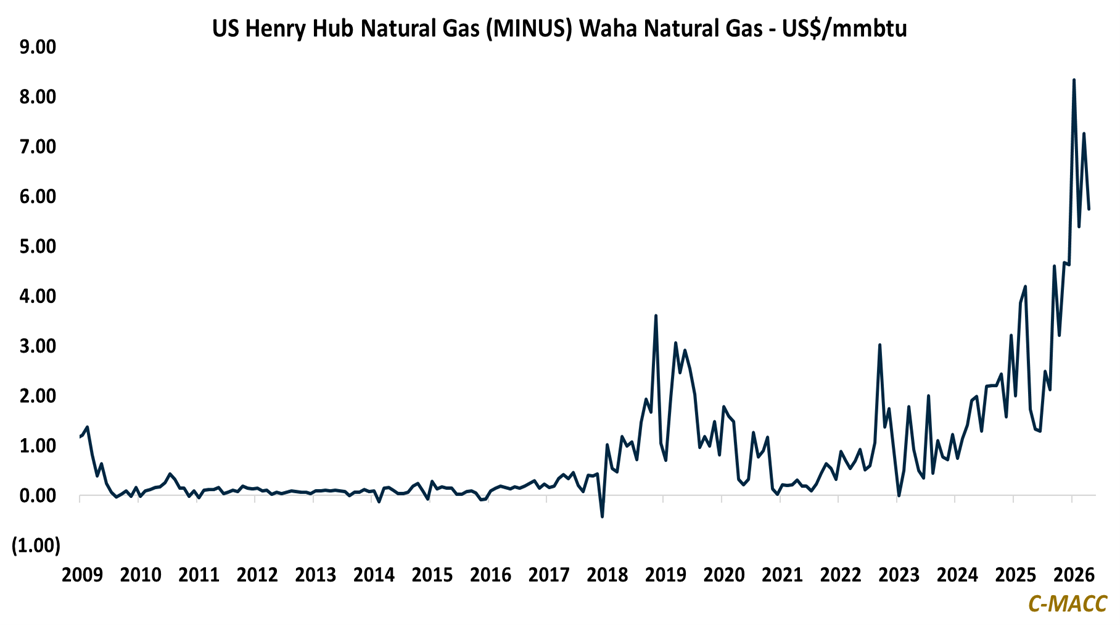

- General Thoughts: Waha’s discount reflects trapped Permian gas value, but lower crude, new takeaway, and rising demand could shift more of the upside to pipeline owners and firm-capacity holders than to end users.

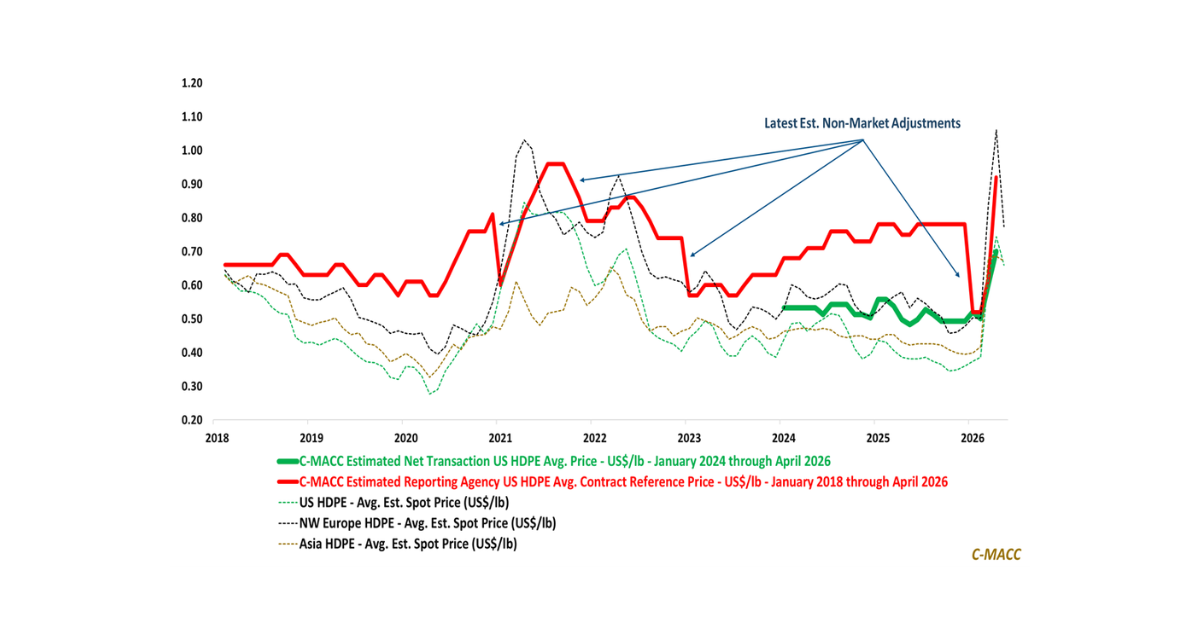

- Supply Chain/Commodities: Aluminum’s rally is testing which buyers truly control delivered cost, not just metal exposure, as power scarcity, trade friction, and financing pressure reset margins across markets.

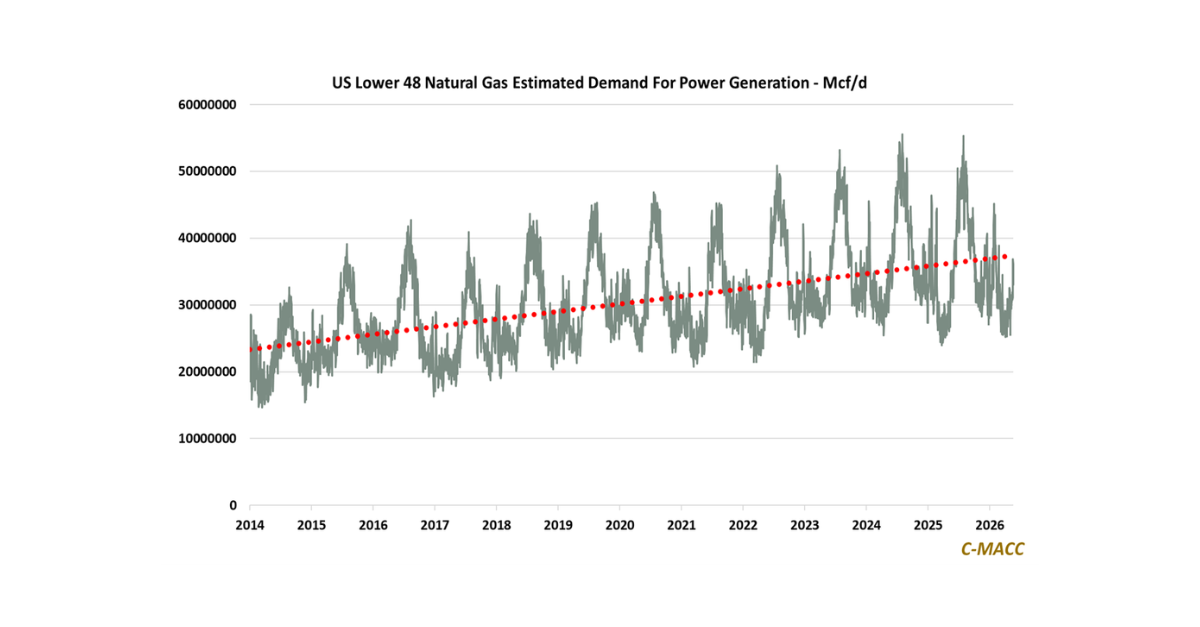

- Energy/Upstream: Flat 2026 US power-sector gas burn versus 2025 masks rising reliability value as regional deliverability, AI load, electrified industry, renewables, and pipeline limits reshape power risk.

- Sustainability/Energy Transition: AI power scarcity is turning clean-air systems into pricing leverage as gas turbines, permits, catalyst service, uptime risk, and qualification history decide usable capacity.

- Downstream/Other Chemicals: Freight volatility is separating margins earned through durable value from those protected by slow qualification, limited alternatives, and unfinished customer redesign.

Exhibit 1: Waha’s Discount Is the Prize for Access Builders, Not a Promise to Consumers.

Source: C-MACC Estimates, May 2026

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!