C-MACC Sunday Executive Summary

The Cover Charge: Lower Prices, Lower Inventories, and Waiting’s Risk Premium

- Chemical and polymer prices have retreated from peak 1H26 levels, but many remain above January levels, leaving buyers to judge whether relief is temporary or durable.

- Wide oil-to-gas spreads still favor USGC petrochemical producers, while firm crude keeps naphtha-linked competitors exposed if inventories rebuild against a higher global cost curve.

- A below-normal Atlantic outlook can reduce urgency, but lower inventories make a meaningful USGC outage more costly if it disrupts production, logistics, or export flows.

- Regional MDI spreads show price defense can survive feedstock relief where qualification, formulation fit, and reliable delivery limit substitutes, while affordability constrains downstream pass-through.

- Additionally, we discuss why apparent relief can mislead buyers when secure routes, qualified supply, delayed cost recovery, and end-market affordability determine who keeps margin.

- Companies Mentioned: CF Industries, Nutrien, Woodside, BASF, Energy Transfer, ONEOK, BW LPG, Santos, Granges, Cobre Panama, Tia Maria, Vale, Rio Tinto, Lifezone, SQM, Standard Lithium, Asian Paints, AkzoNobel, Axalta, Nippon Paint, Sherwin-Williams, Westlake

- Products Mentioned: Ethylene, PE, PP, PVC, PS, MDI, Crude Oil, Ammonia, Natural Gas, Naphtha, Ethane, Benzene, Lithium, Copper, Nickel, Aluminum, Freight, Nitrogen, Propylene

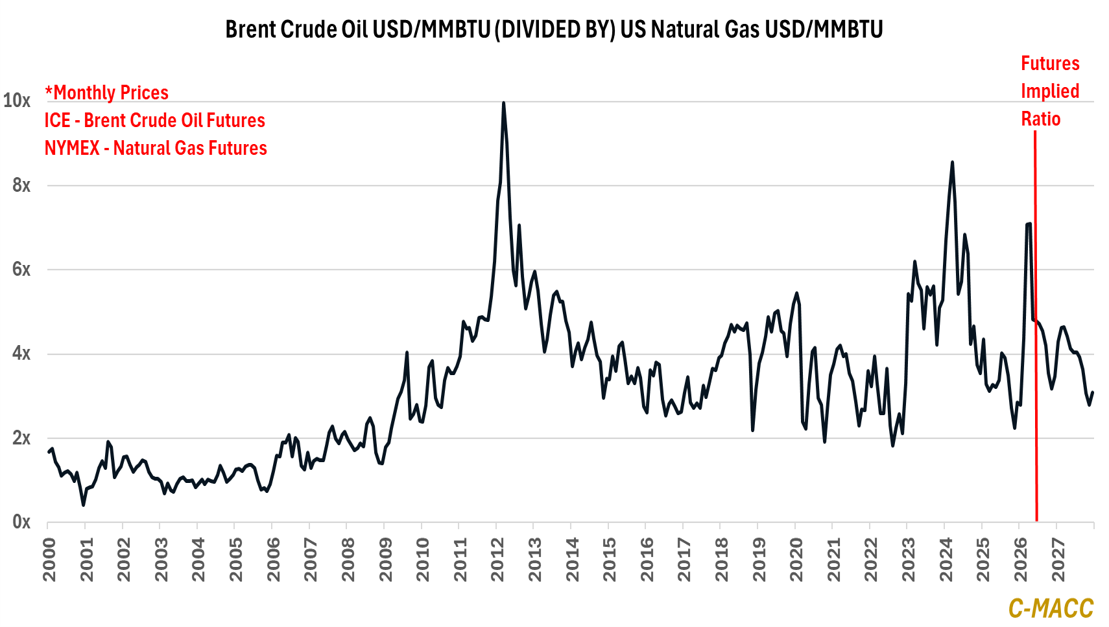

Exhibit 1: Forward Oil-to-Gas Spreads Preserve USGC Cost Advantage as Reported Inventories Decline.

Source: Bloomberg, C-MACC Analysis, June 2026

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!