Base Chemical Global Analysis

Global Weekly Catalyst No. 335

- General Thoughts: Lower costs only become margin when prices hold, leaving commercial terms to separate temporary procurement relief from durable margin control across chemicals, fuels, and agriculture.

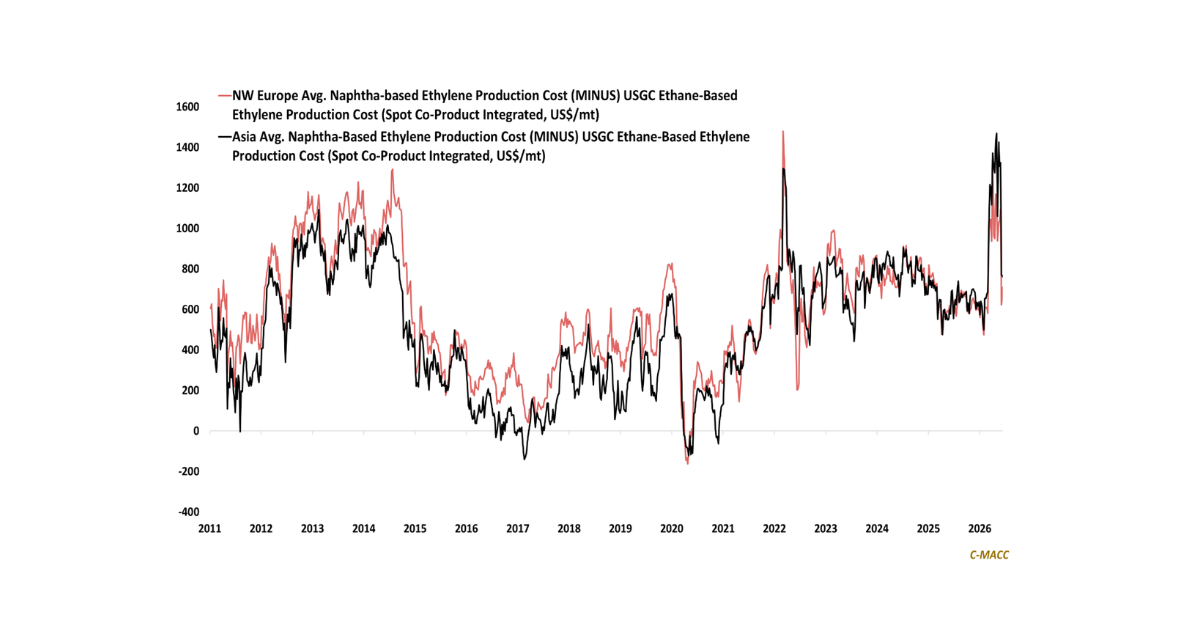

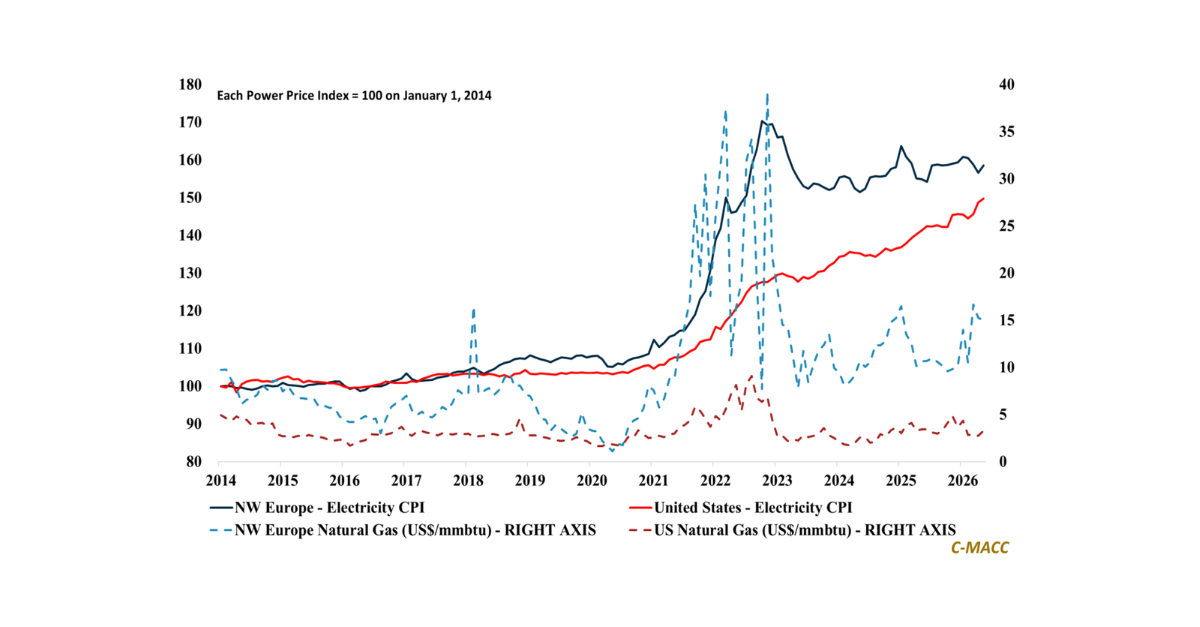

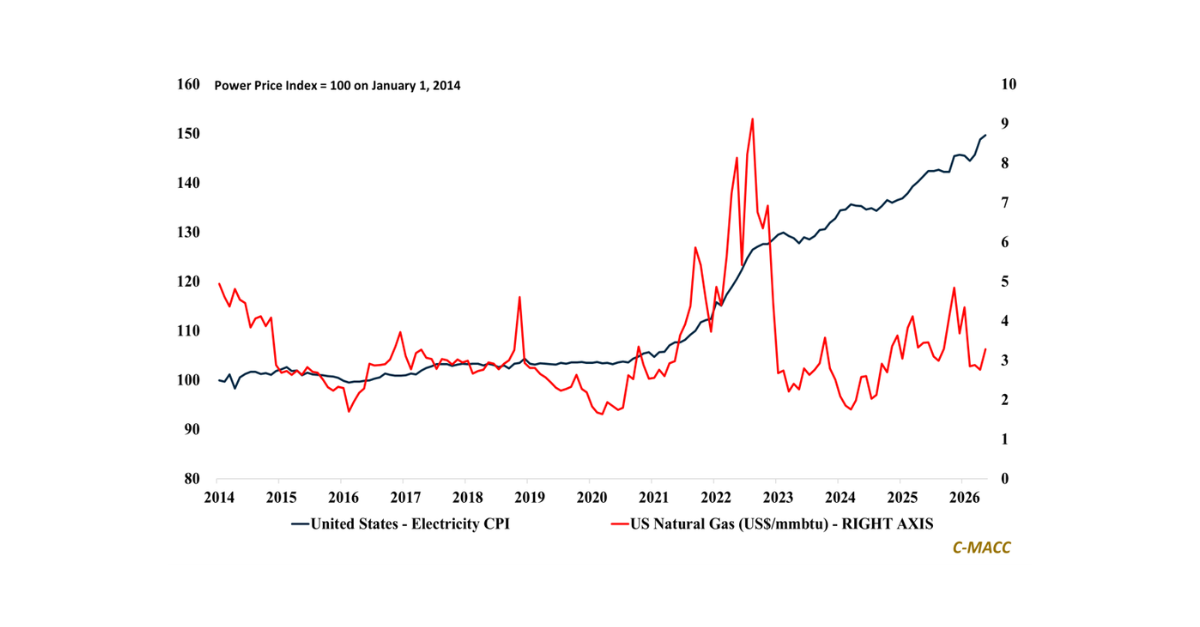

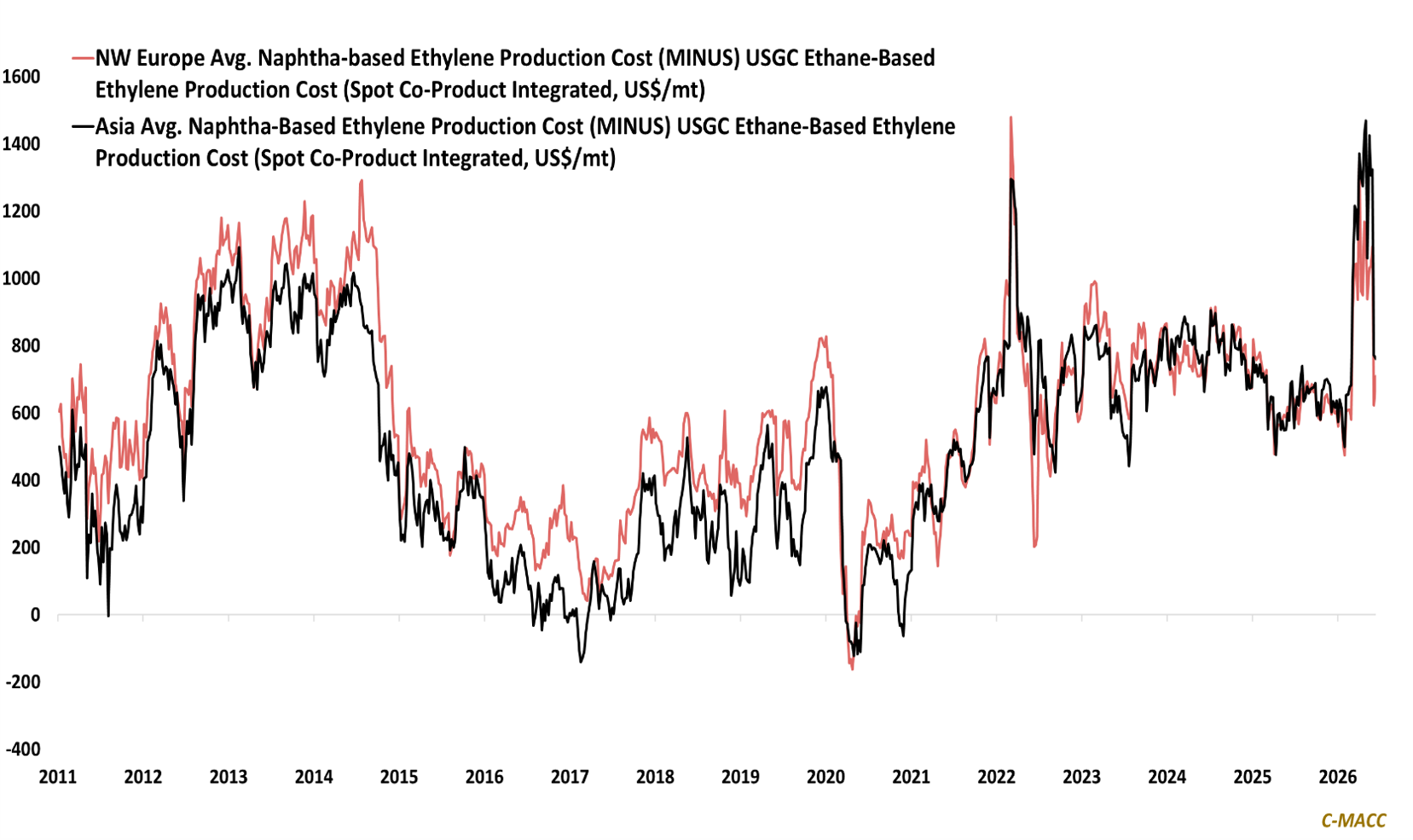

- Feedstocks & Energy: Lower naphtha reduces oil-linked feedstock costs, but China’s return and low inventories limit crude downside, while wide gas spreads preserve North America’s advantage over Europe and Asia.

- Olefins: Lower costs support olefin margins only when producers hold derivative pricing, making Dow’s Terneuzen restart and USGC production reliability a market test for conversion control.

- Other Base Chemicals: Base chemicals reward suppliers with pass-through power, as weakness in methanol and uneven benzene and chlor-alkali pricing show that spot relief has not restored confidence in demand.

- Agriculture: Nitrogen remains necessary, but affordability now dictates timing, leaving secure gas and inland distribution to separate advantaged producers from import buyers who risk waiting too long.

- Refining & Biofuels: Refining margins favor exporters with distillate reach, while ethanol’s marine-fuel path gives low-carbon producers a new demand channel beyond gasoline blending if carbon data supports procurement.

Exhibit 1 – Chart of the Day: Lower Naphtha Compresses Olefin Cost Gaps But Access Still Decides Margin Capture

Source: C-MACC Estimates, June 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!