Base Chemical Global Analysis

Global Weekly Catalyst No. 336

- General Thoughts: Global chemical feedstock cost relief is tempting chemical producers back into production, but the real call is whether fresh supply meets demand or returns the late 2Q26 margin benefit to buyers through 2H26.

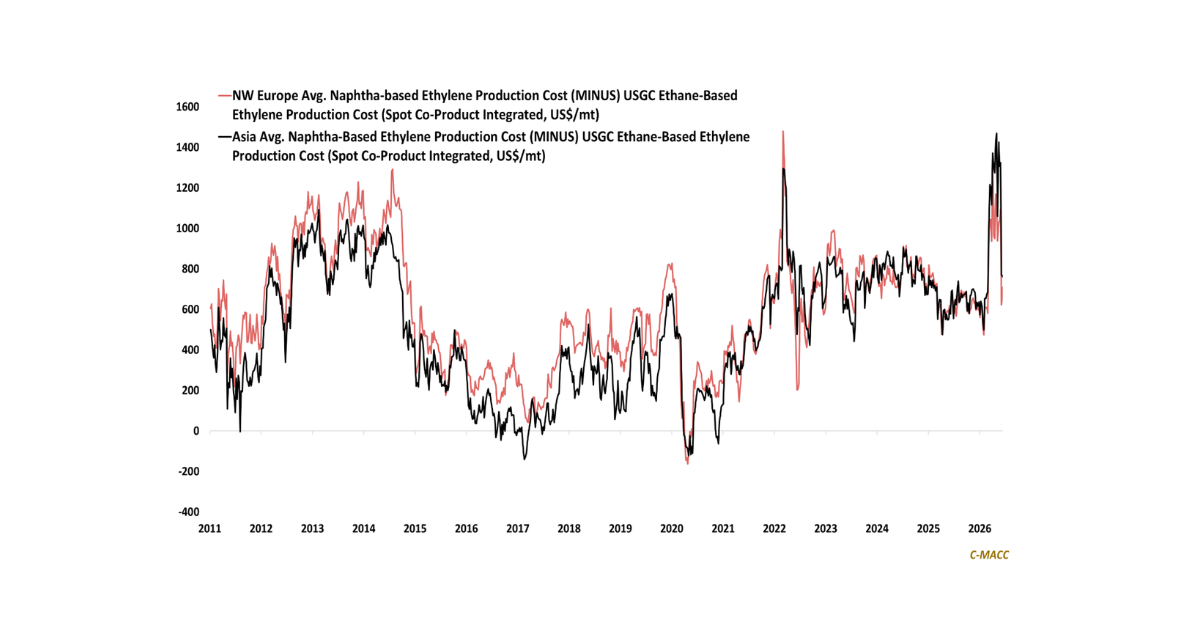

- Feedstocks & Energy: Feedstock cost relief abroad, not in the US, persists as crude oil, naphtha, and ex-US natural gas prices fall WoW, further flattening global chemical cost curves toward pre-Middle East conflict levels.

- Olefins: Global olefin markets are moving from cost squeeze to supply test, as cheaper naphtha invites higher runs before derivative demand has proven it can protect pricing across regions through year end.

- Other Base Chemicals: Base chemicals now reward sellers with customers, contracts, and freight access, because lower inputs only help producers that can resist immediate giveback demands from weaker buyers across regions.

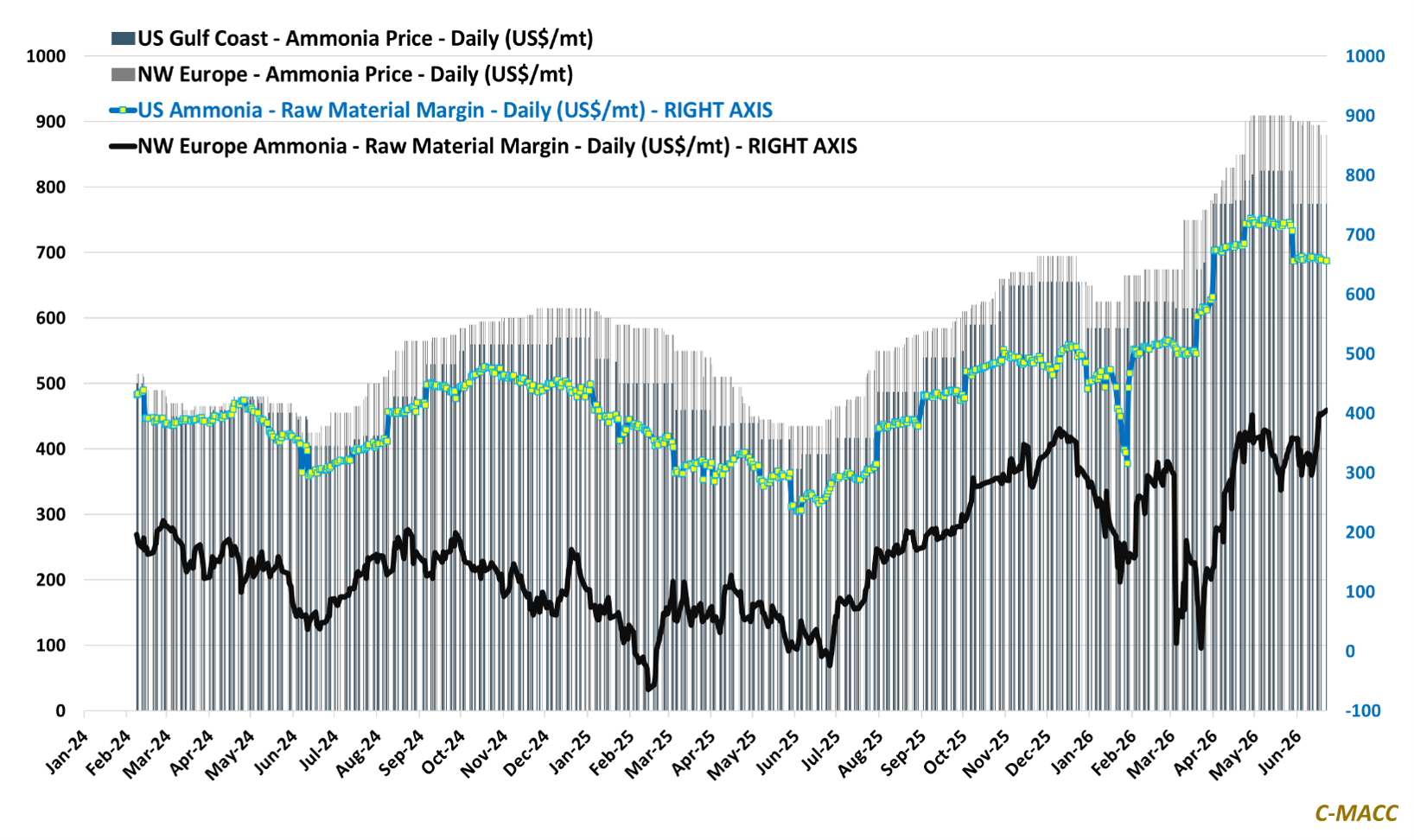

- Agriculture: Nitrogen’s near-term upside sits with producers, as cheaper ex-US natural gas lifts ammonia margins before farmers see enough delivered relief to change purchase timing or cash planning this season.

- Refining & Biofuels: Refining and biofuels still favor route owners, as lower crude supports runs, distillate protects margins, and ethanol gains another path through marine fuel demand beyond gasoline blending growth.

Exhibit 1 – Chart of the Day: Falling European natural gas prices push regional ammonia margins to multi-year highs.

Source: C-MACC Estimates, June 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!