Global Market Analysis

General Thoughts: Most chemical producers anticipate a better year in 2024, driven by improving end-demand outside the US, notably in 2H24 – the impact of

General Thoughts: Most chemical producers anticipate a better year in 2024, driven by improving end-demand outside the US, notably in 2H24 – the impact of

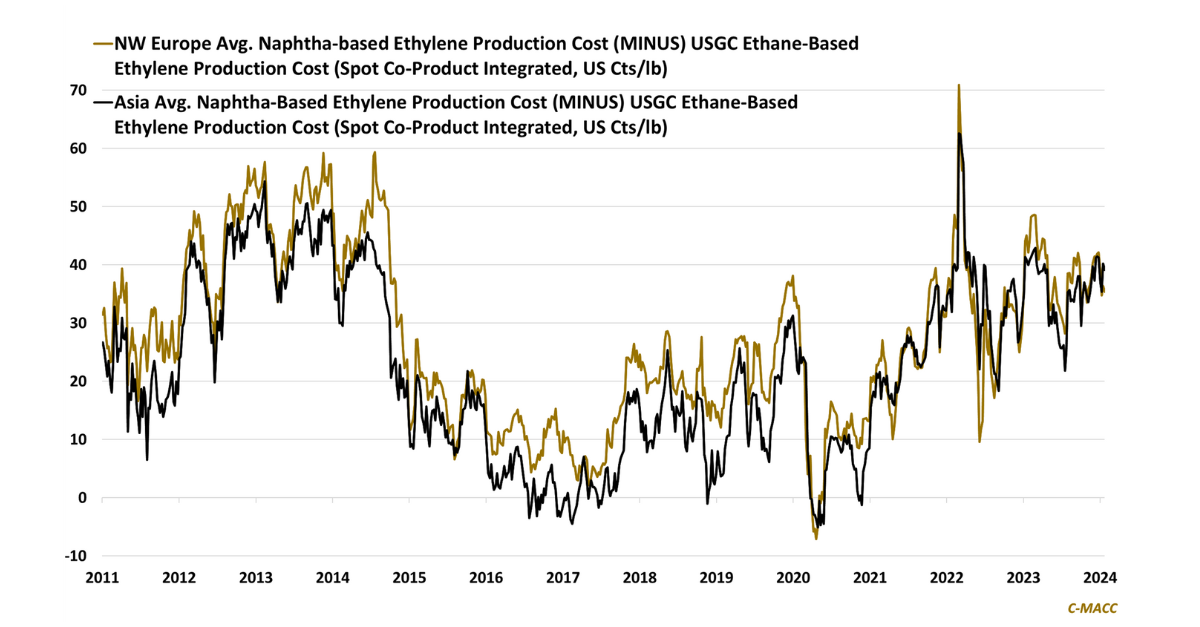

Global chemical markets will likely remain oversupplied in 2024. However, the trade balances between regions will likely further shift, with Europe being one of the

C-MACC Co-Founder Cooley May is attending the Ammonia Energy Association conference this week, with his meetings spanning ammonia suppliers, buyers, and their support industries.

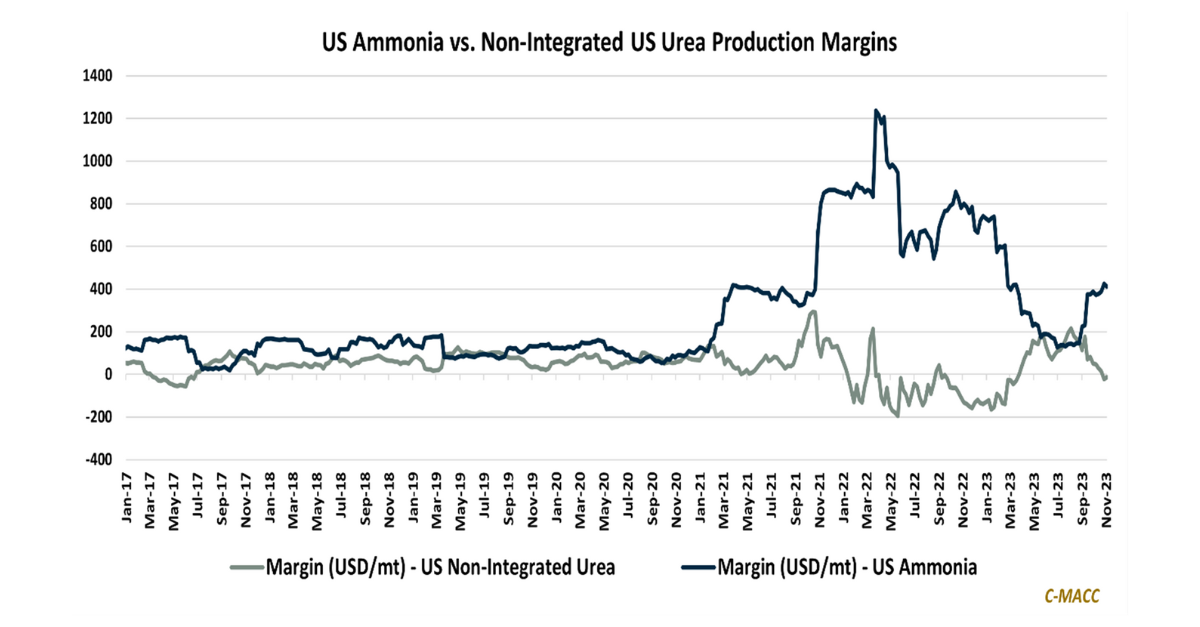

Ammonia

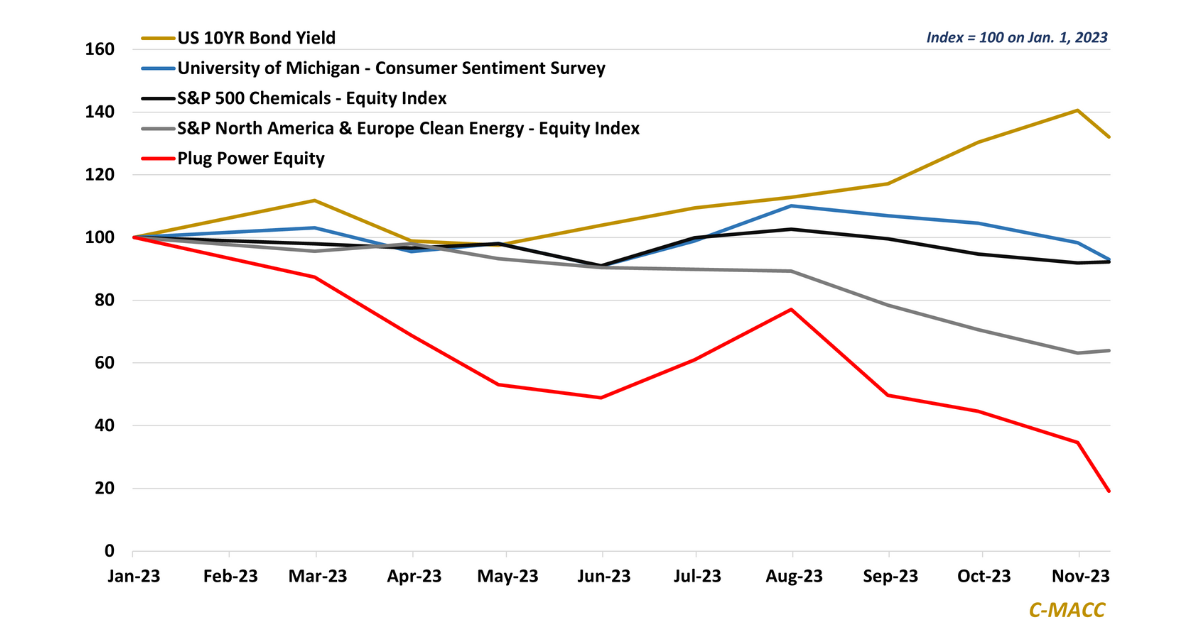

US consumer sentiment fell for the fourth consecutive month in November, and adverse clean energy participant notices have risen – both favor lower energy transition

The C-MACC Clean Energy Minerals Monthly Price Index fell ~6% MoM in April to reflect a 34% lower YTD level, with falling lithium values being

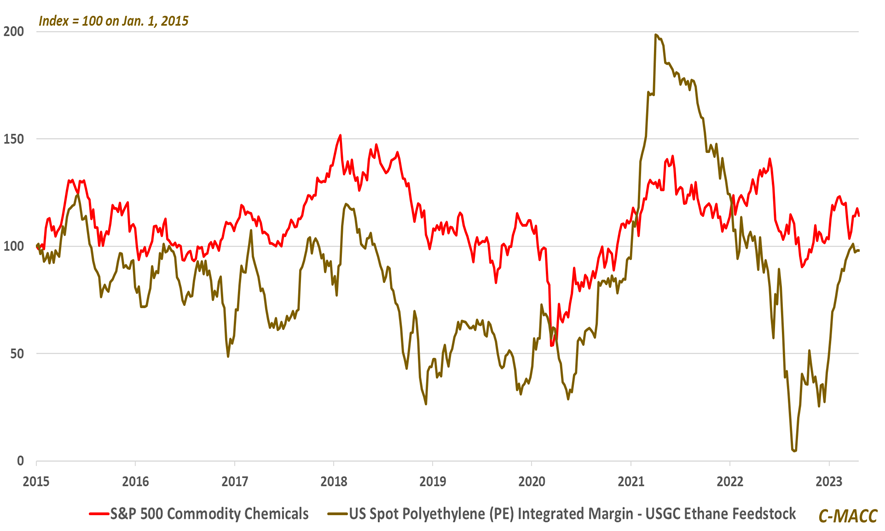

Falling production costs and higher prices favored the US commodity chemical sector in 1Q, beating most estimates – we see more potential to disappoint than

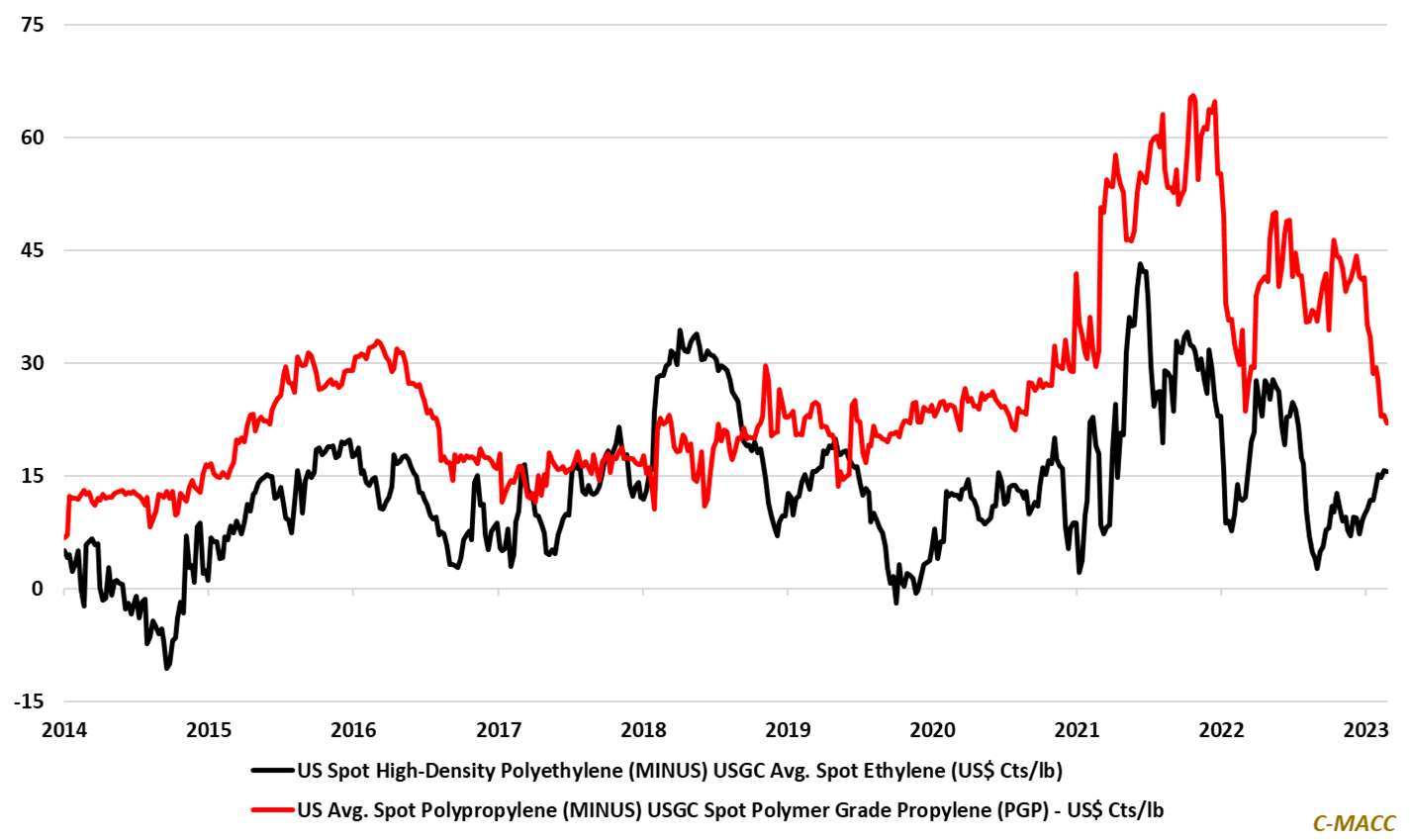

North American petrochemical margins have improved YTD, but volume trends suggest most producers are still at sub-optimal rates despite the global cost curve shifting further

Both C-MACC co-founders will attend CERAWeek. Our initial view of the agenda suggests a heavy focus on energy transition, but other relevant themes are present.

US and Asia polymer prices have risen YTD but for different reasons. A steep global chemical cost curve and rising China demand will help limit

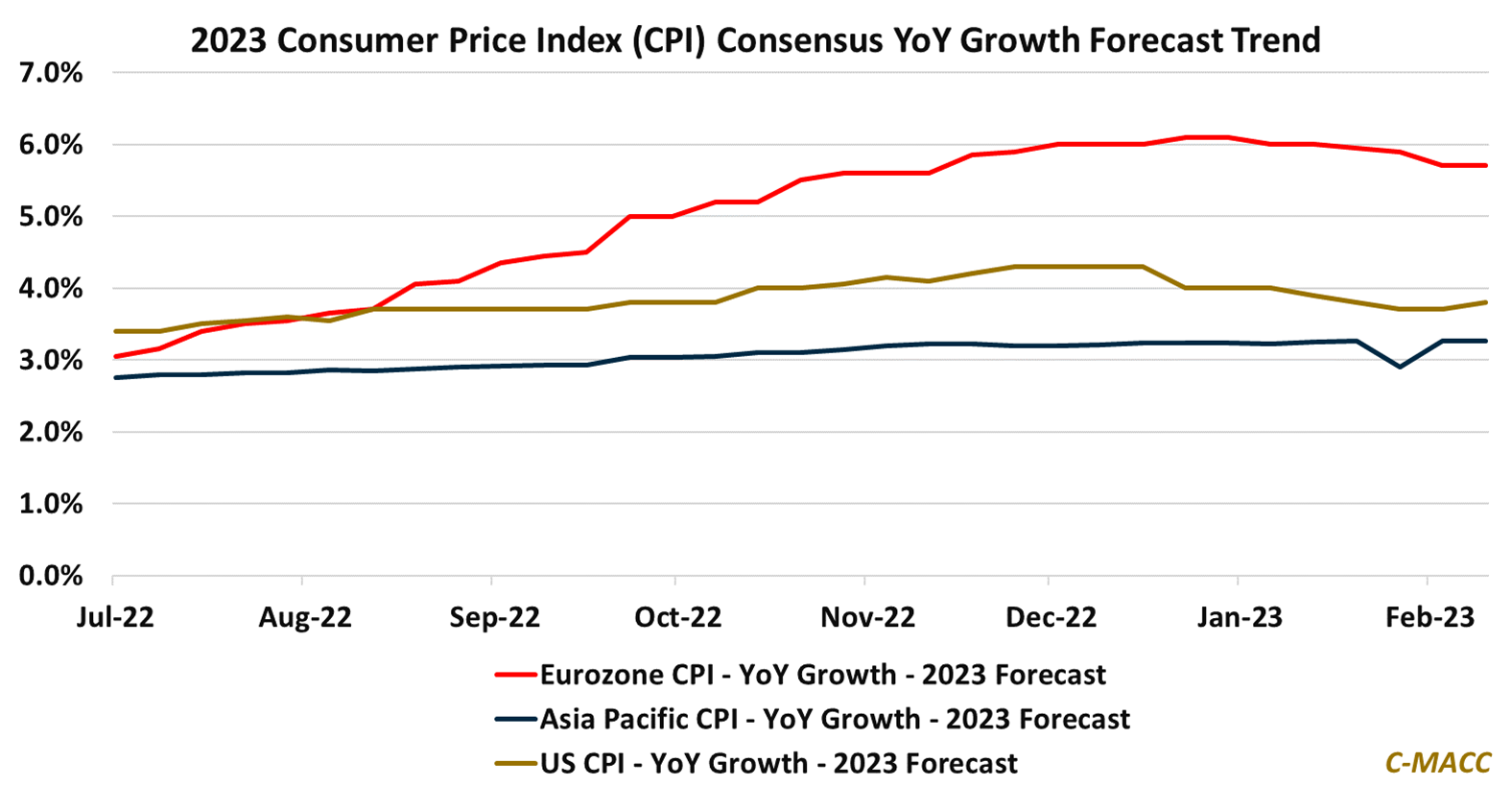

Western consumers will likely face another year of higher prices relative to Asia, but it puts European producers most at risk with its cost disadvantage