Daily Chemical Reaction

Shifting Gears – Many 1Q24 Chemical Demand Views Similar To 4Q23, Costs Notably Different

Key Findings

- General Thoughts: We discuss recent movements in global commodity chemical production costs in light of a few recent producer reports, as those seeing a flatter cost curve and falling prices face more tepid growth investment.

- Supply Chain/Commodities: We discuss the Methanex G3 facility delay, flag Celanese 1Q24 and 2024 outlook commentary, and highlight Westlake 4Q results, US PVC margin trends, and other relevant chemical trends.

- Energy/Upstream: We highlight recent movements in Brent Crude oil prices and US, Asia, and European natural gas, note impacts to LNG movements due to Suez Canal issues, and flag 2024 US power market curtailments.

- Sustainability/Energy Transition: We discuss rising concerns with the availability of low-cost and green power to meet surging demand and comment on the IEA World Energy outlook that, in pockets, could prove too aggressive.

- Downstream/Other Chemicals: We highlight freight rate movements showing still high rates between China, the US, and Europe, and we flag the recent rebound in mortgage rates and Home Depot outlook commentary.

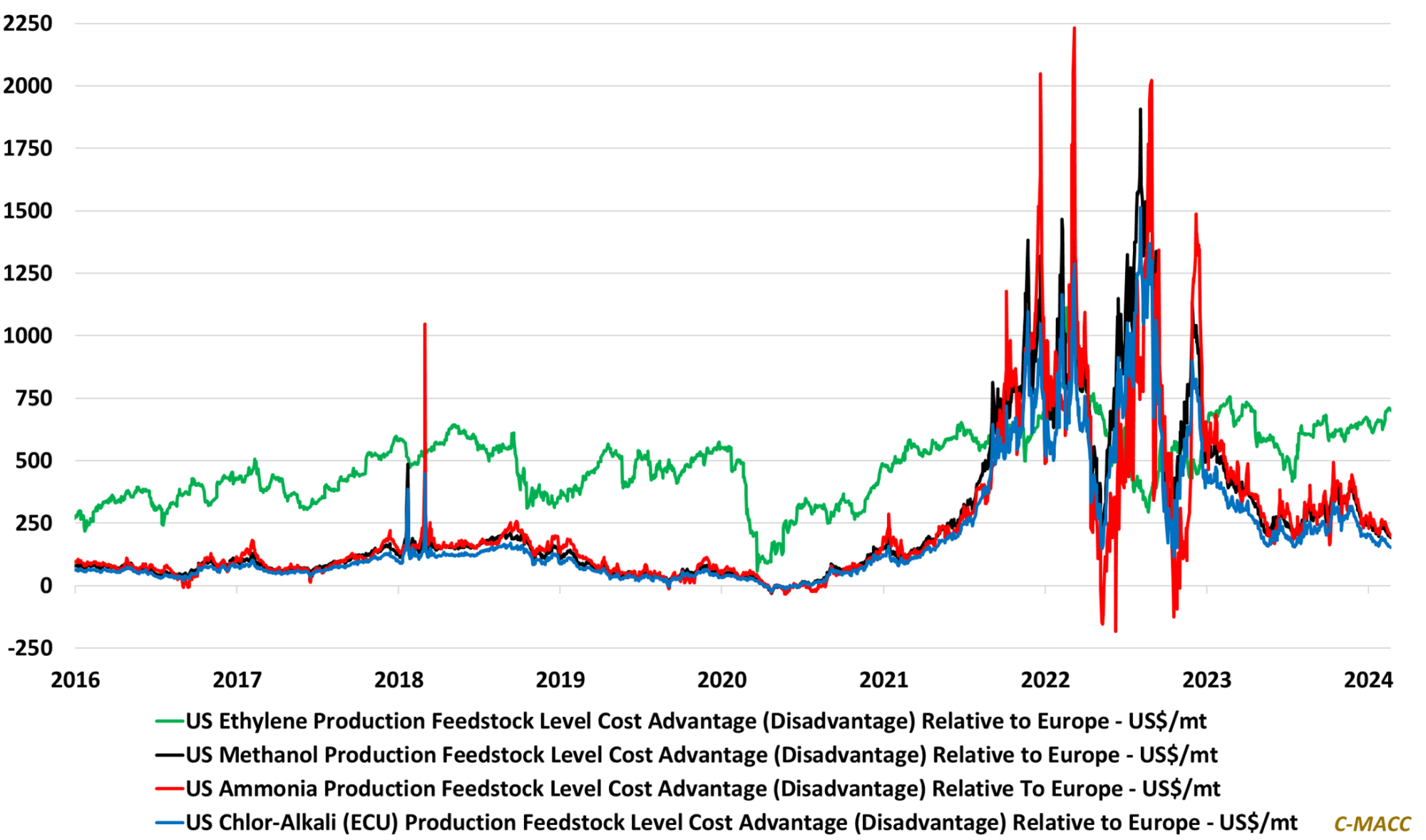

Exhibit 1: The US ethylene production cost advantage relative to Europe has moved in the opposite direction YTD of its methanol, chlor-alkali, and ammonia advantage as crude oil has held up while global natural gas prices weakened.

Source: Bloomberg, C-MACC Analysis, February 2024

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!