C-MACC Sunday Thematic & Weekly Recap

Two Different Views of Chemicals This Week – Global Oversupply, but Still Attracting Capital

- A week of conflicting messages is likely ahead with chemical companies discussing the extreme weakness in margins in Europe and Asia, while the oil and gas companies still express interest in expanding capacity.

- A longer life for LNG; the theme of restated oil majors’ strategies, likely means more NGLs and temptation to build more chemical capacity in low-cost locations, while refinery integration is driving other new capacity.

- At the same time, the US competitive edge gets stronger for ethylene as ethane values weaken, while crude oil rallies – co-product values are rising because of lower production, and this may encourage more ethylene.

- Otherwise, we look at different views of oil demand, rising power demand, how and why Linde is bolstering chemical stock indices, the bankability of US blue hydrogen, and more profitability challenges in Europe.

- We are attending CERA this week and, as a result, some of our reports will be curtailed and focused on specific feedback from the event, including meetings that we have set up.

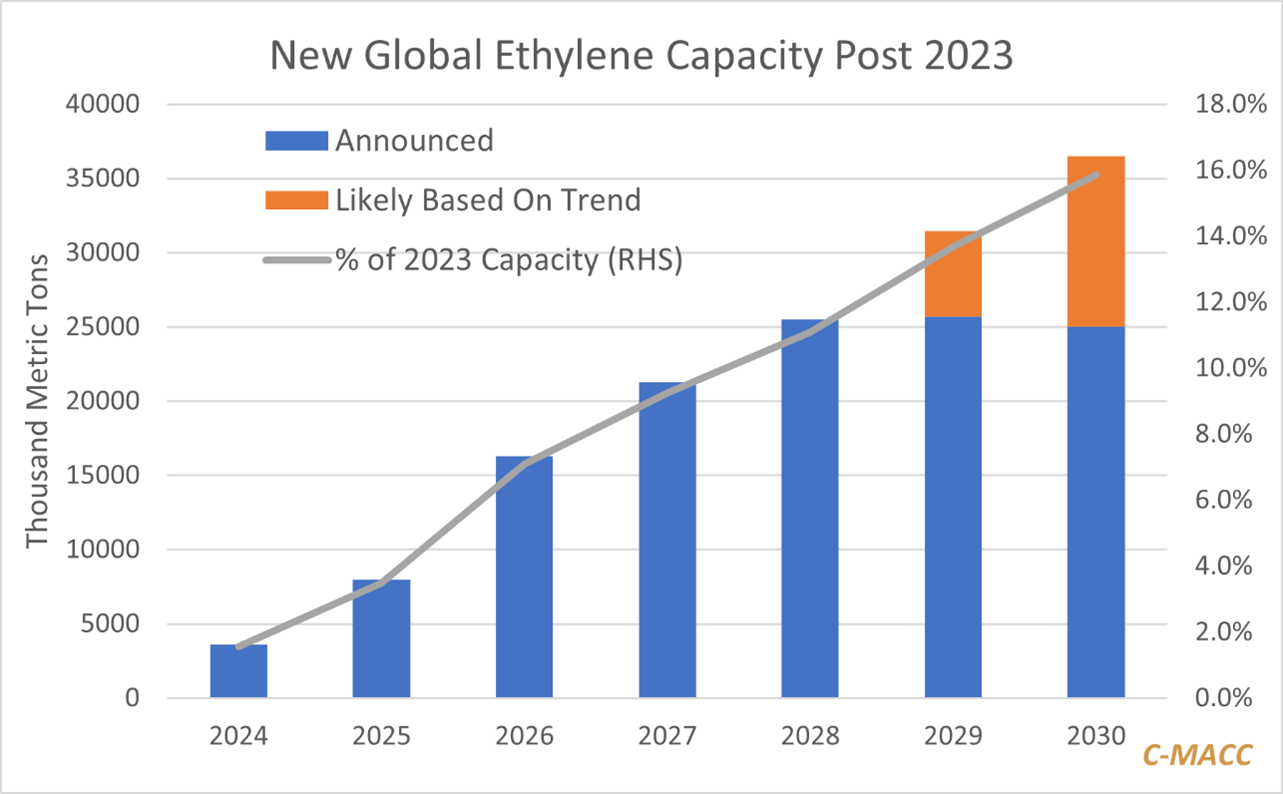

Exhibit 1: A lot of this new capacity is being built in parts of Asia, especially China, where stand alone economics suggest you should not build – see Exhibit 2

Source: Bloomberg, C-MACC Analysis, March 2024

In our sustainability piece on Friday, we talked about the likely CERA and WPC week talking points around energy transition, but there will be plenty to discuss around the base energy and chemical businesses, outside of transition targets and challenges. In a very well-attended (and positively reviewed – thanks) webcast last week, we talked about one of the factors that we believe will make this basic chemical cycle particularly challenging and possibly quite long, which is not only a growing surplus of feedstocks for chemicals, but at the same time, a desire by many in the oil and gas business to expand their presence in chemicals as a means to consume more captive hydrocarbons. We have tended to focus on ethylene when we have been talking about global oversupply, but the risk for propylene and aromatics is also very real if refiners see lower demand for gasoline – eventually – and start reconfiguring to make more chemicals – aromatics from reforming and propylene (and possibly ethylene) from higher selectivity catalysts and higher temperatures on FCC units. As we noted in both the webcast and in other recent work, you could see chemical companies lamenting the low profitability of the business – outside the US and the Middle East – while oil and gas producers see positive margins in upgrading either oil or gas that they might otherwise not be able to produce. We are beginning to see closures – a styrene plant here and a polymers plant there – but the moves are incremental relative to the oversupply. We are also seeing assets available for sale, and if these get acquired by companies looking to upgrade crude oil as opposed to stand alone chemical profitability, then we have the potential for very low prices and prolonged marginal economics. This could be an interesting week, as on one side we could see a group lamenting the weakness in chemicals while others see an opportunity.

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!