C-MACC Weekly Sustainability and Energy Transition Report

It Could Be Worse; We Could Be in Europe!

- 1st Topic of the Week: Planning departments within European chemical companies are likely trying to understand how their business has a future and, for some, whether it has one at all. Outside of chemicals, plenty of other energy-intensive industries face some of the same challenges. We struggle to find solutions for many.

- 2nd Topic of the Week: The China manufacturing dominance headlines continue, and clearly, the country’s best interest is not served by cutting back manufacturing at a time when the local economy has been underperforming and other key sectors, such as construction, are suffering.

- Otherwise: We study the challenges of competing with the food chain for fuels and the high cost of lowering carbon intensity, the need for global carbon values, why the electrical equipment/control companies could do well, and spending estimates.

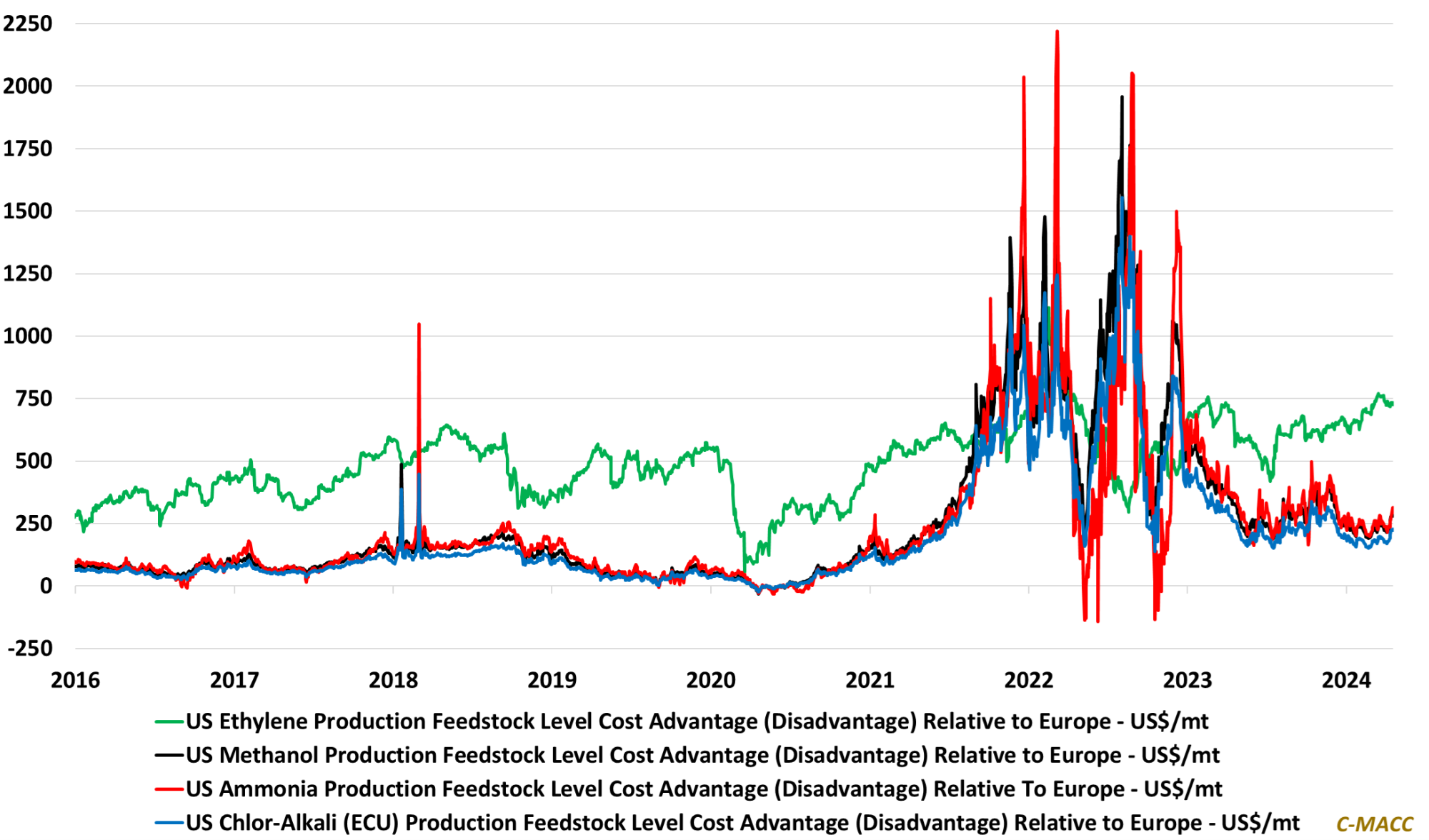

Exhibit 1: We highlight a few examples of US chemical production cost advantages relative to Europe, with ethylene continuing to hold the most pronounced advantage relative to most other upstream petrochemicals.

Source: Bloomberg, C-MACC Analysis, April 2024

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!