No love for transition and sustainability

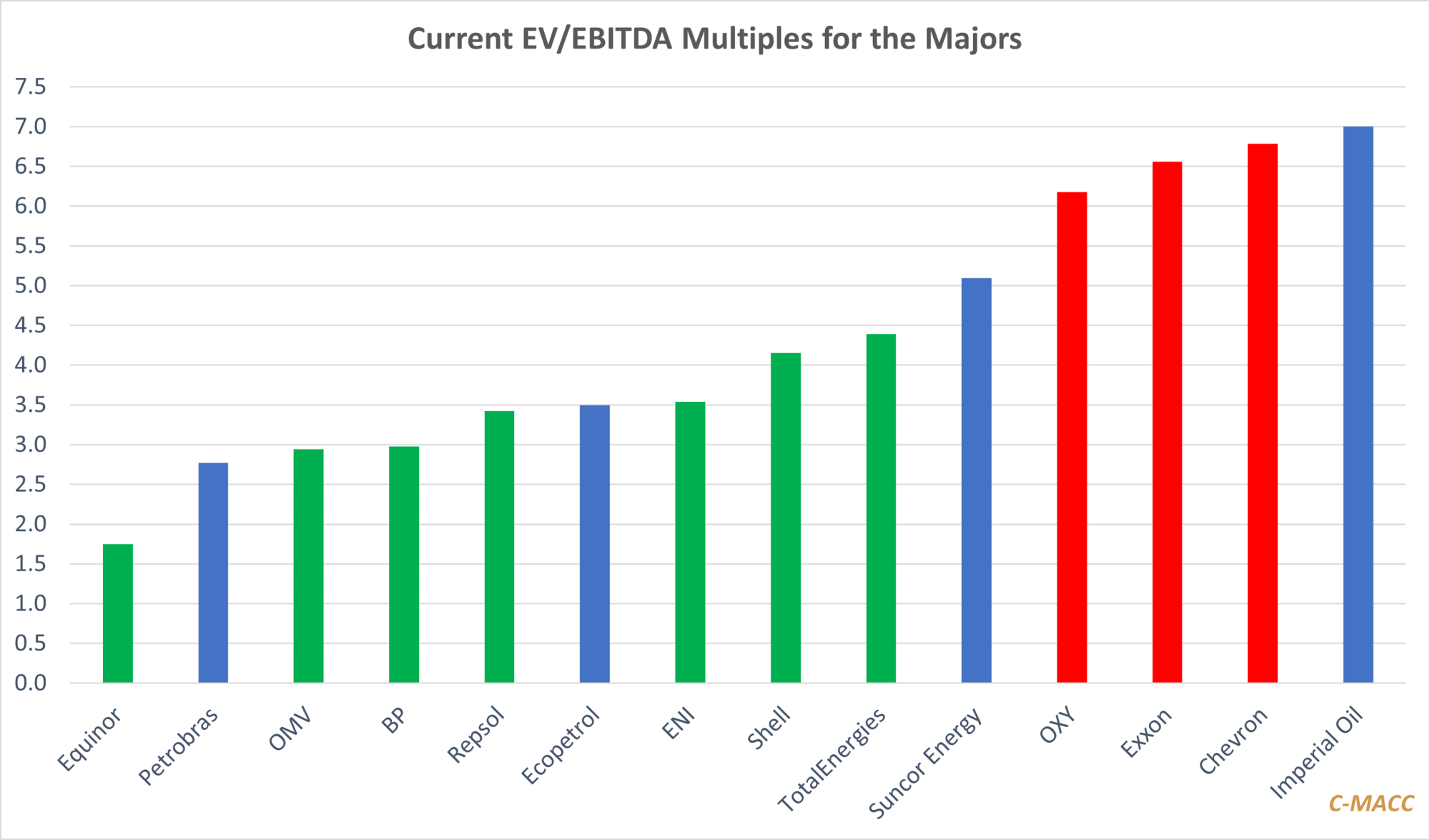

US integrated oil companies command a much higher premium than many of their European peers.

Source: Capital IQ, C-MACC Analysis, April 2024

In an interview this week the former CEO of Shell, Ben van Beurden, talked about the valuation disconnect between the US and Europe for energy companies and the possible attraction of listing Shell in New York versus London. This is a topic that we have raised a couple of times in our market research service, but it is part of an overall finance issue facing many aspects of energy transition, and in many cases, it is making the path forward very challenging for companies across many industries and of all sizes. For the oil majors in Europe, the US is too expensive for M&A, multiples are too high in the US and any acquisition from a European company would be horribly dilutive, whether the currency was stock or cash. This leaves the Europeans only able to play with each other, in jurisdictions where they are not loved from an environmental perspective and where they might face unreasonable anti-trust scrutiny. Whether moving to the US would unlock all the value suggested above is unclear, as those energy companies with the most progressive energy transition strategies have been penalized more that those with the least, and both Shell and BP would likely face some of this challenge if they moved. Still, the valuation differences as shown above are significant and are handicapping the lower valued companies. Every company above and most of the independents in the E&P space is being valued at a steep discount to its reserve values, and this might make some of the European companies even more attractive to the US companies if the US companies could stall plans to lower either production or reserve replacement.

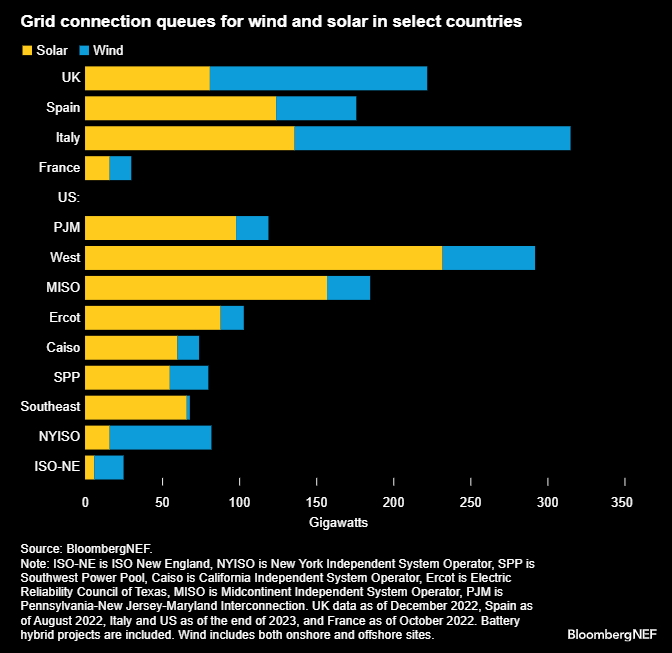

But financing and valuation is also astray in many of the new energy initiatives, and hopeful front running because of too much optimism is the problem. In our hydrogen report, The Hydrogen Optimists – Often in “La La Land” and Always Unhelpful we talk about the optimism driving premature investment in hydrogen technology, but there are plenty of other examples within energy transition, and we note the grid-interconnectivity chart below to show how projects can be delayed for reasons well outside the control of the operators. We see electrolyzer capacity being built well ahead of any reasonable demand expectations, we talked about battery makers investing at 3x the rate of expected demand growth in our reports last week and we see the same with power.

Grid connection cues are increasing, slowing down clean power developments, and connection costs are also rising, which is pinching project margins, per BloombergNEF, whose view in this area generally aligns with ours.

Source: BloombergNEF, April 2024

To read the complete report, fill the form below and get in touch.