Daily Chemical Reaction

Weights & Measures – Moderating End-Product Prices to Hurt Supplier Margins; Can Capacity Meet Surging Power Needs?

Key Findings

- General Thoughts: US wholesale good price inflation is slowing, and the global consumer push toward cheaper goods is underway, which we view as unfavorable for margin improvement in many chemical chains in 2H24.

- Supply Chain/Commodities: We discuss recent strength in copper prices, announced technologies, and capacity growth in critical minerals to lift supply, as well as consensus views for tightness to favor oversupply in some areas.

- Energy/Upstream: US power capacity additions will likely set a record in 2024, with most of the additions being in wind and solar. However, capacity growth through 2030 appears likely to struggle to meet the demand surge.

- Sustainability/Energy Transition: We discuss the anti-ESG movement in the US and its developments across a few states, and we view perceived issues with project incentives and permitting as unfavorable for energy transition.

- Downstream/Other Chemicals: US and Europe interest rates surged post-COVID relative to China, and we discuss the potential for falling Western rates to stoke consumer demand and a likely push toward cheap Chinese goods.

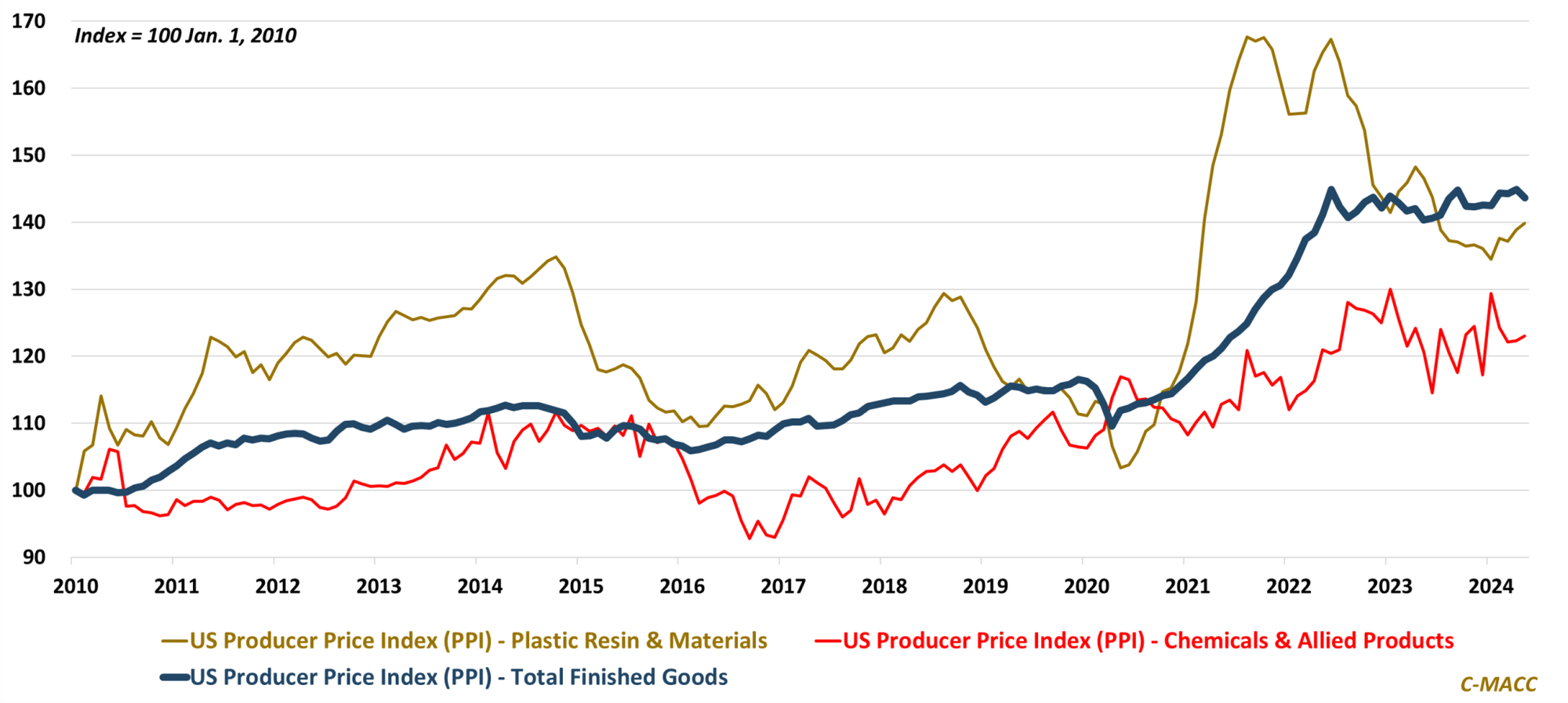

Exhibit 1: The US PPI for Plastics Resin & Materials has risen YTD relative to upstream chemicals and the overall PPI.

Source: Bloomberg, C-MACC Analysis, June 2024

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!