C-MACC Sunday Theme and Weekly Recap

The Temptation and Need to Build in The US

- This week, we hit another high in the relative attractiveness of producing ethylene and natural gas derivatives in the US versus the rest of the world. With more LNG coming, gas prices may rise, but NGL surpluses will grow.

- ExxonMobil and others reported record Permian-based crude production in recent results. The immediate net effect is too much natural gas and too many NGLs, and prices are returning to recent lows.

- While natural gas demand will pick up with the wave of LNG capacity expected over the next 4-5 years, NGLs, especially ethane, need either more ethylene capacity (in an already surplus US) or terminal capacity for export.

- While production economics favor adding chemical and polymer capacity in the US, investing seems obvious when you overlay the potential for lower decarbonization costs in the US, cheaper power, and sequestration.

- Otherwise, we look at the swings in the US propylene market and anticipate another one, we look at end market strength and weakness with more focus on Ag, and why both hydrogen and recycling belong with the big boys.

Exhibit 1: Note that the more recent wave of US ethylene capacity was approved and built during the shaded period

Source: Bloomberg, C-MACC Analysis, August 2024

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!

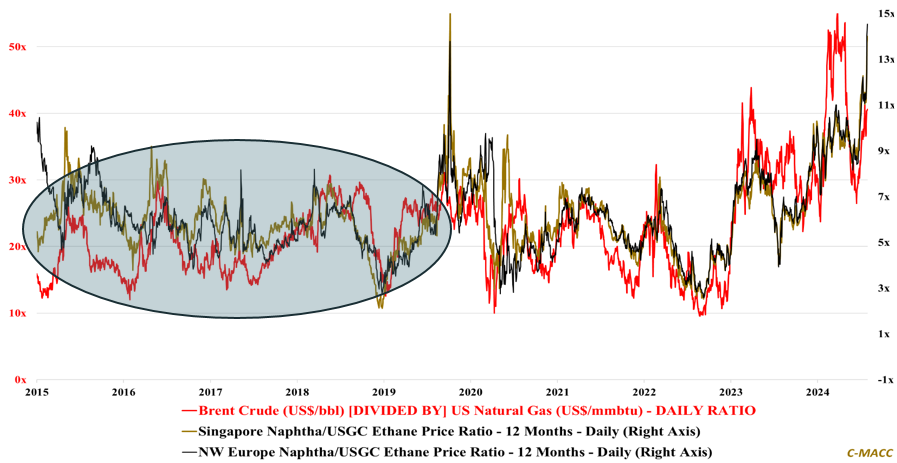

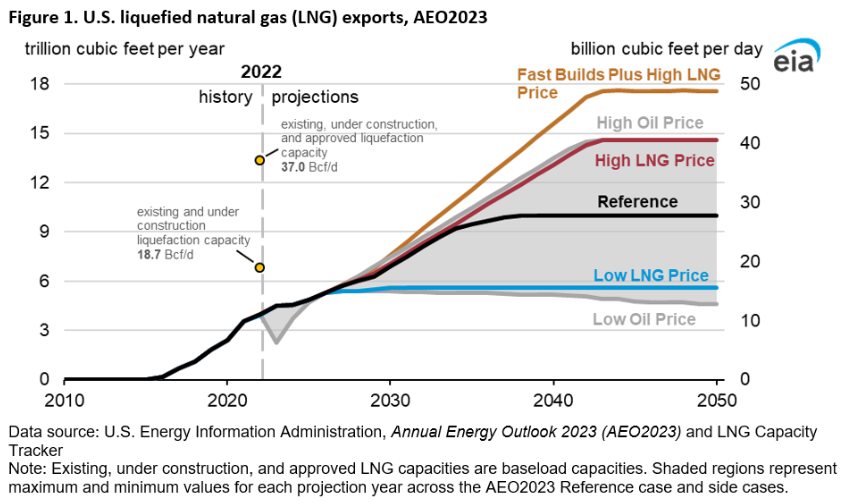

The low current price of ethane versus natural gas and the low price of US natural gas versus crude oil are not enough on their own to encourage more investment to consume in the US – availability is key, and it is rising. The motivation for the wave of ethylene, methanol, and ammonia investments that we saw in the 2015-2021 period was not just the price of natural gas, it was the expectation of much more natural gas and NGL availability, because of expansions in the Permian and Marcellus oil and gas fields. Today we have very profitable oil in the Permian, and consolidation which will only lower the development costs further. This oil brings more associated gases, and the Permian is very rich in associated methane and NGLs. However, we also have a demand driver on the natural gas side, which is another wave of LNG facilities in the US. The recent Texas LNG offtake agreement with EQT shows that there are buyers still willing to lock into longer term take or pay contracts, and clearly of the view that energy transition cannot move fast enough to prevent further growth in LNG demand for many years – a view that we share. In the “high LNG” case below which is likely the better reference, we double LNG capacity in the US, and this does not include capacity in Canada and Mexico, which will impact demand for US natural gas also. If the World keeps underinvesting in crude oil production, we give OPEC+ a relatively easy task in maintaining oil prices, even if absolute demand for oil begins to fall, which will maintain the incentive to produce in the Permian for many years, keeping natural gas and NGL production high.

Exhibit 2: This EIA analysis is a year old, but it shows approved capacity for LNG at twice the existing and under construction levels.

Source: Bloomberg, C-MACC Analysis, July 2024

While it is not clear that crude oil prices will fall, and you can make a strong case for them rising, it is likely that US natural gas prices will rise. We will likely need more production from the Marcellus to meet LNG demand and the Marcellus and other gas rich plays are not profitable with pricing below $3.00 per MMBTU – see Chesapeake’s Q2 2024 expectations/results. NGL prices will rise with natural gas prices, but unless infrastructure to consume the NGLs is built, they will remain in surplus and at a discount to fuel value – remember that the Marcellus is NGL rich and the further you move West in the formation (as a rule of thumb) the more NGLs. Competition between LNG facilities, local utilities, and methane-based chemicals (including what could be a wave of blue ammonia by 2035) could drive up US natural gas prices, and close the arbitrage suggested in Exhibit 1. Still, the ratios could move a long way before the cost advantage in the US shrank too far. Plus, this still does not get away from the likely very large surpluses of NGLs, especially ethane. As the chart below notes – we already have a surplus, and in Exhibits 4 and 5 we show how a lower ethylene spot price in the US still creates a much higher ethylene margin.

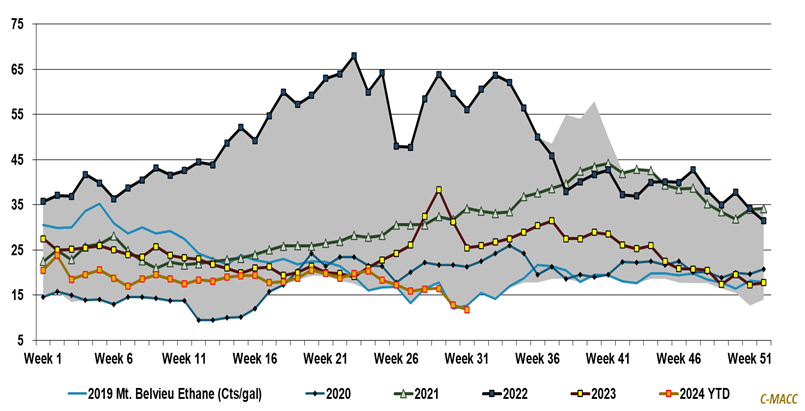

Exhibit 3: USGC ethane prices hit a YTD low this week, notably benefiting ethylene producers with facilities online – also see article, US Ethane Prices Hammered by Strong Production, Lower demand and Crushed Gas Prices.

Source: Bloomberg, C-MACC Analysis, July 2024

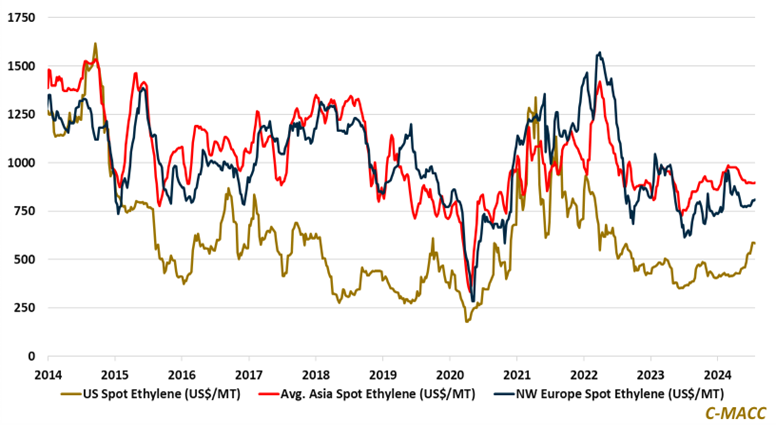

Exhibit 4: US spot ethylene prices have surged but remain significantly below spot ethylene prices in Asia and Europe, and we expect increased domestic ethylene production later this year to likely reverse some of the recent strength.

Source: Bloomberg, C-MACC Analysis, July 2024

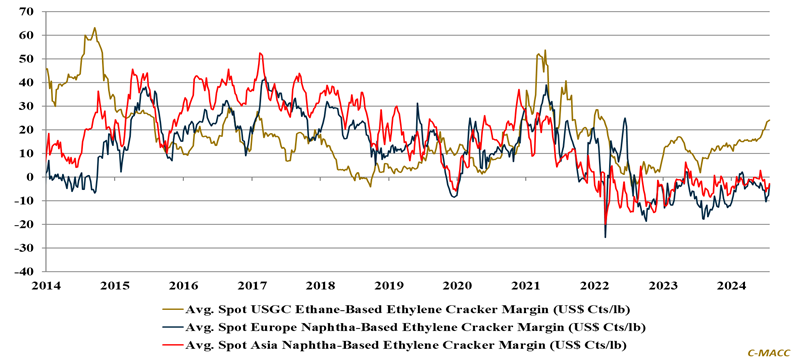

Exhibit 5: US spot ethylene margins hit a fresh 2024 YTD high this week; Europe and Asia remain under pressure.

Source: Bloomberg, C-MACC Analysis, July 2024

The ethylene price arbitrage shown in Exhibit 4, justifies moving US ethylene to Europe and Asia, but the cost arbitrage in Exhibit 5 would suggest that if you have the production capacity and logistic flexibility, moving US ethane to Europe or Asia is more profitable. It is not surprising to see investments in Europe aimed at consuming US ethane and there are already ethylene units in Asia consuming US ethane. Several years ago, before we were distracted by COVID, we were involved in a very early stage look at the opportunity to build a second large ethylene/ethane export terminal in the US, and most of the offtake opportunity at the time was ethylene for Southeast Asia. If you do not export ethane or ethylene from the US, you have very limited options, as there are very clear limits to which you can blend ethane in the natural gas stream if you cross state borders and even tighter limits (like zero) of you are feeding an LNG plant. There would be the possibility of burning ethane in a dedicated power facility, but this would need to be custom designed to capture CO2, as the CO2 footprint would be higher than a methane-based unit.

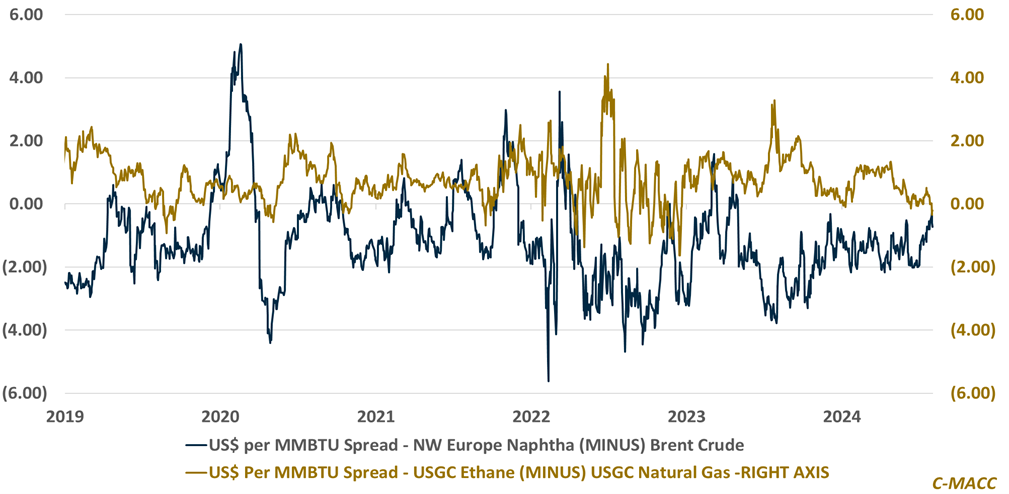

Exhibit 6: USGC ethane prices fell relative to natural gas in July, while Europe naphtha rose relative to Brent crude oil.

Source: Bloomberg, C-MACC Analysis, August 2024

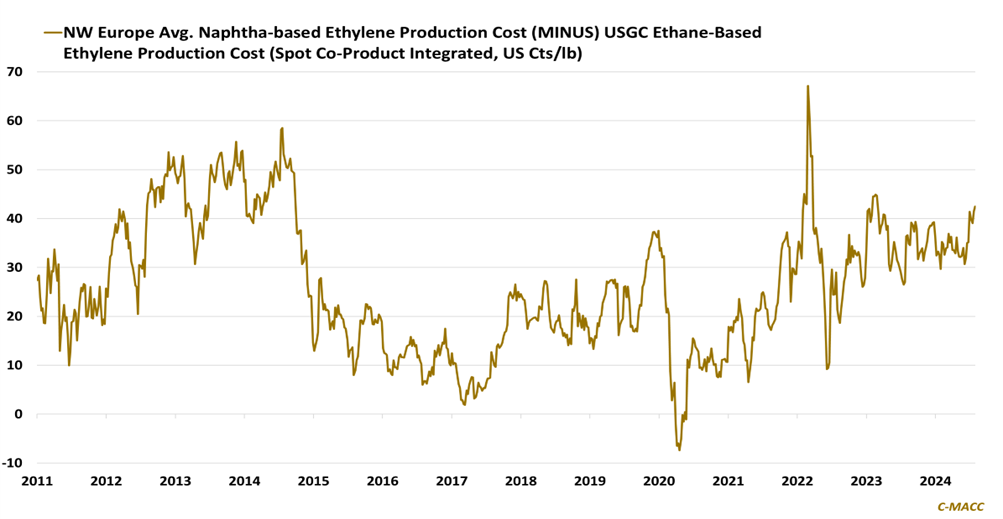

Exhibit 7: Europe is the more obvious place to put US ethane and derivatives.

Source: Bloomberg, C-MACC Analysis, August 2024

Rays of hope in Europe – likely to cloud over: LyondellBasell is one of several companies that have posted better European results in 2Q 2024 than might have been expected three or four months ago. While still very weak compared to US profits, there was a margin improvement in Europe because energy prices fell incrementally for most of the quarter, and some price initiatives were successful. One of the supporting factors for US polyethylene in recent months has been higher export netbacks from Europe, for example. While we can see a reason to be near-term bullish in the US, as companies maintain inventory and are unwilling to get too aggressive with suppliers through the hurricane season, the read-through for Europe is not there unless you conclude that exports of polymers could be severely impacted by storm damage. The economic backdrop in Europe is weak, and while crude oil prices remain well off their highs, the LNG market has picked up again, which could adversely impact European natural gas and power prices. The fundamental disadvantage of making basic chemicals in Europe is unlikely to go away, and we see US ethane prices falling more rapidly than crude oil prices today, with the chart above showing that relative costs of naphtha-based chemicals are hitting an extreme again relative to the US. Adjusting for the significant step down in refining margins, the LyondellBasell results were not bad. The only criticism we would have with the presentation is that we think the company is trying to save too many operations in Europe, and the “under review” list should lengthen. That said, the exhibit below is well thought through and very helpful.

Exhibit 8: LyondellBasell displays its efforts and strategy to create a sustainable European products business.

Source: LyondellBasell – 2Q24 Earnings Presentation, August 2024

Then there is the low carbon argument, which would support going all the way from ethane to polyethylene in the US and increasing the exports from the US of polymer even further. The sequestration and blue hydrogen opportunities in the US suggest that low carbon polymers will be significantly cheaper to make in the US than most other regions, except some Middle East countries and possibly China. We have noted in plenty of recent research that the biggest geopolitical risk to US chemicals and plastics, is changes in trade policy, and not any variability in carbon emission goals or legislation. We suspect that there are a couple of plans, either for new ethylene for export, or new polyethylene for export, or just terminals for ethylene and/or ethane export, sitting at the pre-FID stage, waiting for policy clarity – trade more so that carbon.

We note the Enterprise expansion announcement below and link it to the possible LyondellBasell closures discussed above. As operations become too expensive in Europe, we will continue to see shutdowns, but unless consumer demand falls in Europe, the materials and their precursors will have to come from somewhere. Some will come from higher operating rates from other European facilities, but dependence on exports, from the Middle East and North America will rise. We see specific terminal expansion plans from Enterprise (in partnership Navigator for C2s) for more ethylene, ethane, propylene, and propane expansions, but given the cost advantage in the US and what is likely to be a surplus of NGLs in the US for the foreseeable future, there is likely an opportunity for larger export terminal expansions and possibly a competitor to Enterprise. The more LNG growth we see in the US, the greater the availability of ethane and propane and the greater the incentive to find markets outside the US, either for the ethane and propane or for derivatives, which would mean more ethylene and propylene capacity. But it is worth noting the Chesapeake results as the company is very Marcellus and natural gas based, and the weak natural gas prices that we are seeing this year are too low to drive profits, which means they are too low to drive further investment. It is likely wrong to model US natural gas prices longer term below $3.00 per MMBTU, as this will curtail investment where crude oil is not the driver of the investment.

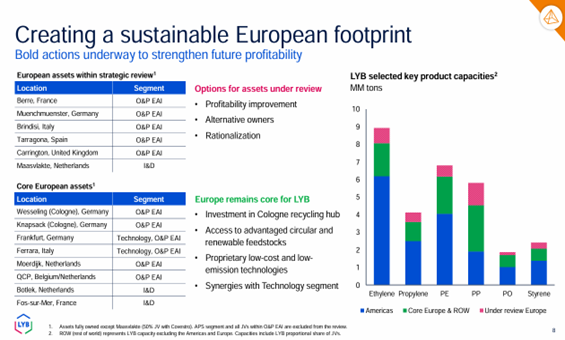

Exhibit 9: Near-term strength in oil and LNG – but not in US natural gas

Source: Bloomberg, C-MACC Analysis, August 2024

The US NGL surplus – cheap ethane for everyone? In one of the headlines below, there is commentary around increased ethane consumption in China for ethylene production. As we note in our ethylene economic work, the discount in US ethylene is giving producers a huge competitive edge today in addition to the crude oil/natural gas spread. If you could take it, you would be encouraged to import ethane from the US as a cracker feedstock almost anywhere in the world. But the challenge is logistics as well as ethylene plant design. Most ethylene units can expand the amount of ethane feed taken, but not by much, unless they were specifically designed to do so. There have been some expensive conversions to take more ethane feed and SABIC is in the midst of one in the UK. The logistics challenge is that ethane is expensive to ship and needs dedicated terminal investment both on the export and import sides. The import investment is likely the more challenging, as it needs to be site specific – focused on the ethylene units that can use ethane. In the US, there are ethane pipeline networks across the Gulf Coast, which means you have plenty of possible locations to expand export capacity. For more ethane to be used outside North America and the Middle East there will need to be a lot more infrastructure investment. Then the question for the exporters will be whether ethane is the right way to go – should you export ethane, ethylene, or polymer, for example. This was a more straightforward debate 10 years ago, but as we think about the trend towards lower carbon materials, the lower decarbonization costs in the US may tip the scales towards more polymer exports versus ethane. That said, anyone in Europe or Asia switching from a naphtha feed to an ethane feed is lowering the CO2 produced per ton of ethylene and this may be used as a “lower carbon” argument.

Otherwise, Last Week

The calm before the propylene storm – unless there is a storm! One of the issues we noted in today’s monthly C-MACC/PXi Polymer Price Expectations report was the possible reversal of the US propylene price trend, as noted in the first chart below. The US has several very large production facilities for propylene, PDH, and refinery propylene splitters, and when some of these are offline – as was the case for some of July, the market is short. Propylene supply is tight, leading to a higher spot and sometimes contract price if the outages are severe enough. This development has become frequent in the US, as PDH unit production has proven notably unreliable. At the time of writing this report, the US facilities are either back online or coming back online, and this is almost always negative for US propylene prices, so while the chart below shows a short pricing spike, it could reverse quickly. The clear wild card at this time of the year in the US is storm activity, and we saw production and logistic issues with the recent hurricane, although not nearly as severe as we have seen with storms in the past. The forecasters are calling for a strong storm season, and Beryl was a bad omen because of its early timing. Consumers will likely want to hold more inventory to mitigate possible storm-related losses, which has provided demand and pricing support over the last couple of months across the chemical and polymer space. If we do not have more storm-related losses, we will have a supply overhang that will likely drive weaker markets in 4Q 2024. The flip side is that any bad storm that hits the industry directly – or series of storms – could disrupt supply more seriously than can be countered by recent inventory moves.

Source: Bloomberg, C-MACC Analysis, July 2024

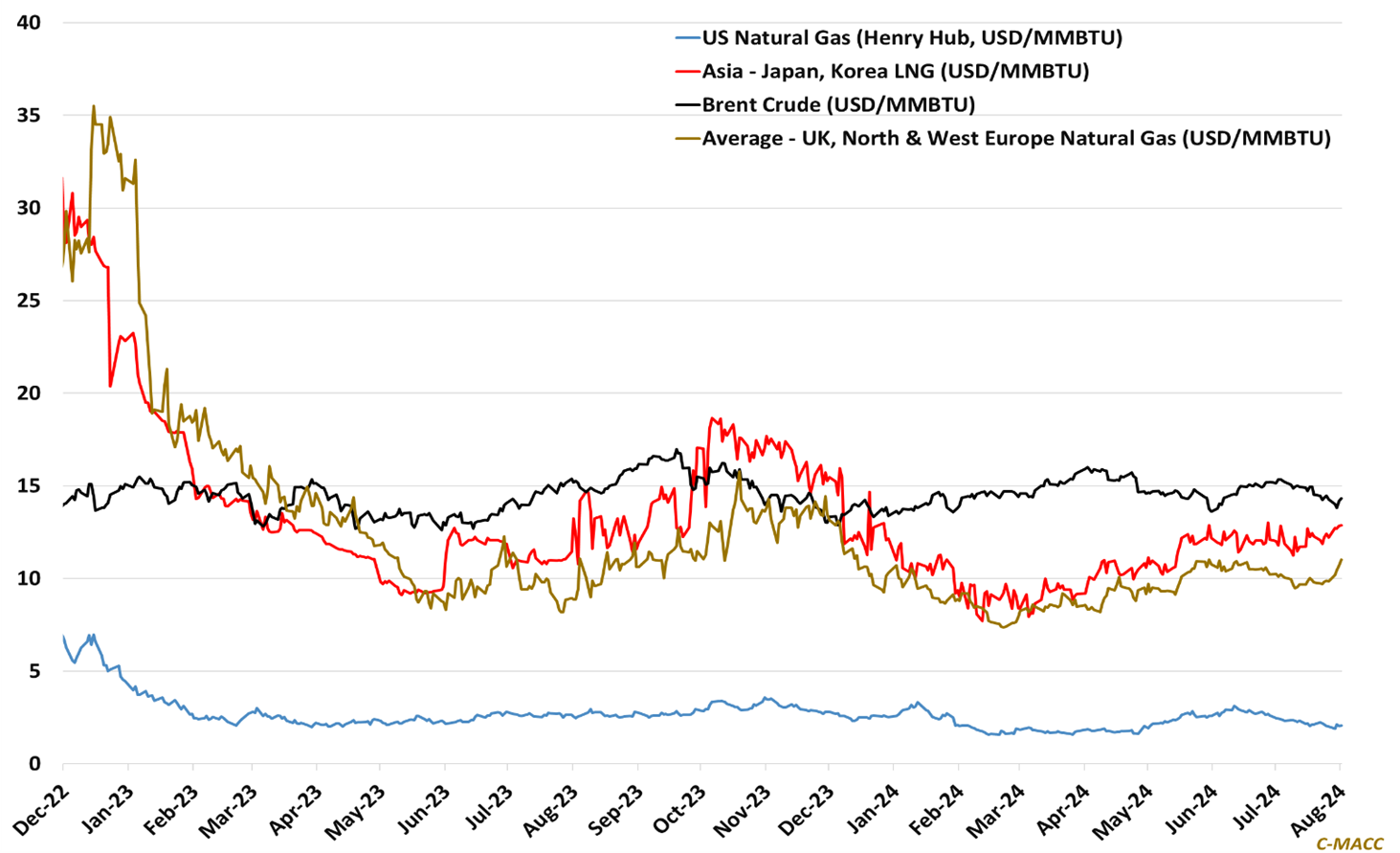

Exhibit 11: US propylene prices reflect a premium to ex-US levels as shown above.

Source: Bloomberg, C-MACC Analysis, July 2024

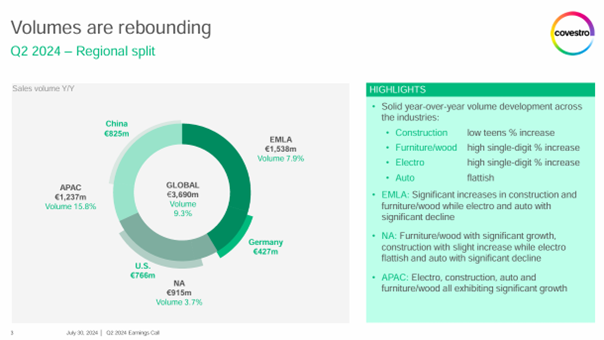

Strength in construction and furniture, weakness in electronics, autos and Ag. A major takeaway from the Covestro 2Q24 earnings call last week, beyond confirming that it has opened its books to discuss a potential transaction with ADNOC, is the mixed health of durable good market end demand. Overall, Covestro estimates volume up ~9.3% YoY, with construction showing the greatest growth followed by furniture and electronics and auto markets being the weakest. Part of the growth uptick is due to improved availability of MDI and TDI to serve construction and furniture end markets, though we find auto end-market weakness being the greatest concern. This adds to concerns with EV market growth relative to expectations, and the lack of pricing power in this industry, which we think could worsen rather than improve in 2H24. Beyond this, we flag the Clariant views below, and we also highlight end-market views from ADM, as crop demand has also taken a hit, and McDonald’s and P&G, as we observe much of the pushback from consumers being toward still high downstream prices.

Exhibit 12: Covestro broadly highlights volume improvement across its end markets

Source: Covestro – 2Q24 Earnings Presentation, July 2024

Exhibit 13: Clariant flags the most volume improvement in Europe, with more mixed results in Asia and North America

Source: Clariant – 2Q24 Earnings Presentation, July 2024

- ADM misses profit estimates on US demand dip and lower crush margins

- China’s manufacturing activity seen extending decline in July

- Corning sees weak Q3 profit on slow demand for clean-air tech

- P&G posts surprise sales drop as demand slows despite price restraint

- Product demand surges in Germany after prices dip

- US consumers show signs of flagging, companies and analysts warn

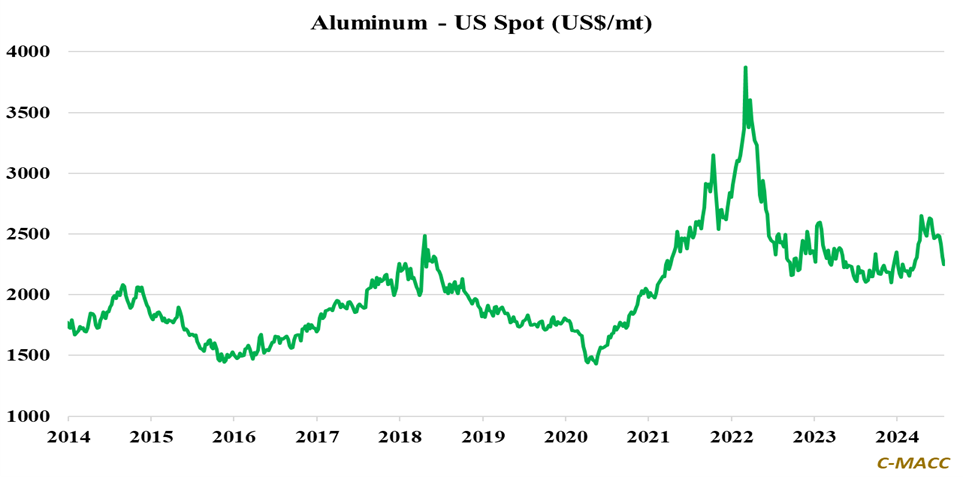

Exhibit 14: Aluminum prices have fallen from YTD highs, returning to 2023 levels as demand falls below expectations.

Source: Bloomberg, C-MACC Analysis, July 2024

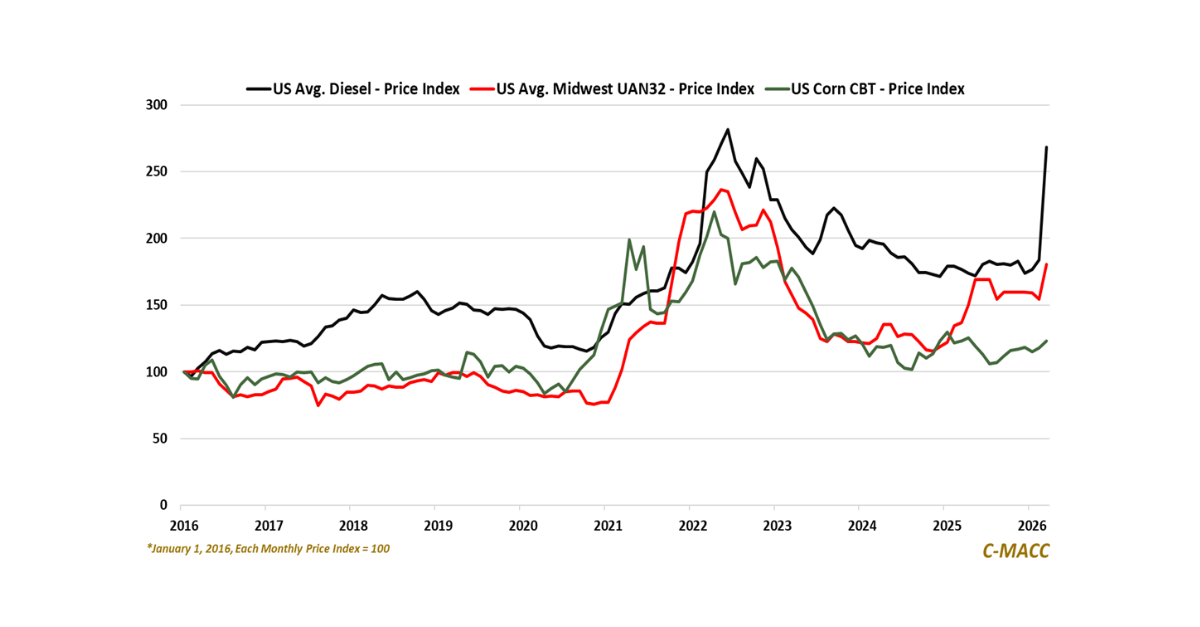

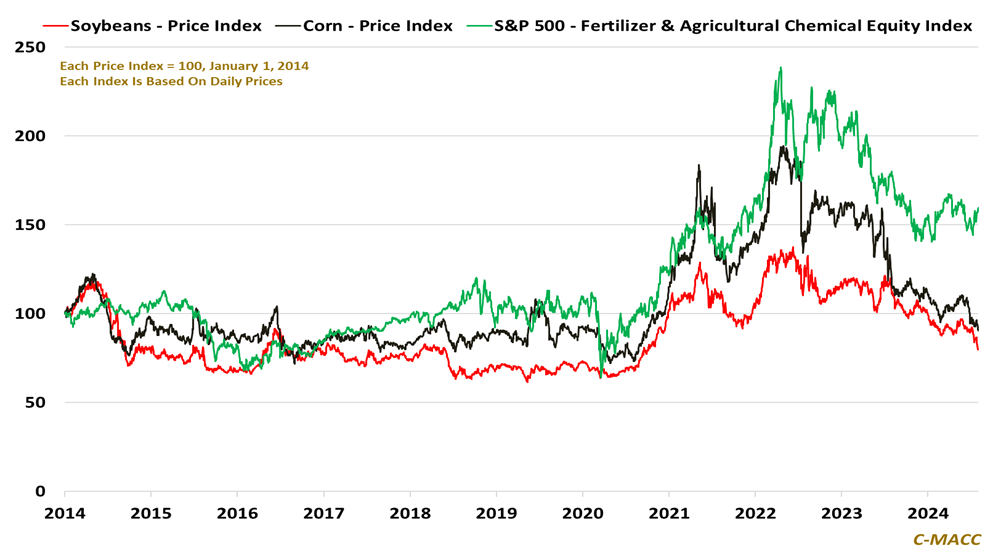

Exhibit 15: US soybean and corn prices hit a YTD low this week, implying lower farmer income, a key gauge for on-farm input & other spending. In contrast, the S&P 500 Fertilizer & Agricultural Chemical equity index reflects support.

Source: Bloomberg, C-MACC Analysis, August 2024

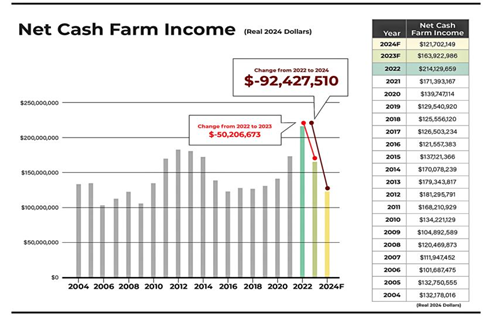

The set up in the agriculture space is quite concerning: With the collapse in corn and soy prices, we will likely see some consequences that pull the markets back in the opposite direction quite dramatically, although perhaps not immediately. We were discussing in the office yesterday one possible comparison that may be relevant – with the US electric power balance, and efficiency. For years, power demand growth has been kept low because of power use efficiency gains – these are now falling away, and power demand is rising more quickly. For years the corn and soy markets have been kept in balance because of productivity gains, largely driven by farming technique breakthroughs, more resilient seeds, and better crop protection products – most of these gains are behind us and future growth in demand will need to be met through more land use. When we then consider the possibility of more crops being used as feedstocks for renewable fuels, we have the potential for a step change in demand (power with AI would be the comparison) and limited resources to address that gain. The current low corn and soy prices will only encourage more investment to use the inputs for fuels and materials – the cost of ethanol for example is falling steadily as corn prices fall. As noted above, perhaps now is the time to pick up cheap farmland. We stand by our “buy corn” recommendation, even if we may have been a bit early!

Exhibit 16: The Ugly Truth: 2023 and 2024 Will Go Down As the Two Largest Declines in Net Farm Income Ever

Source: AgWeb, USDA, August 2024

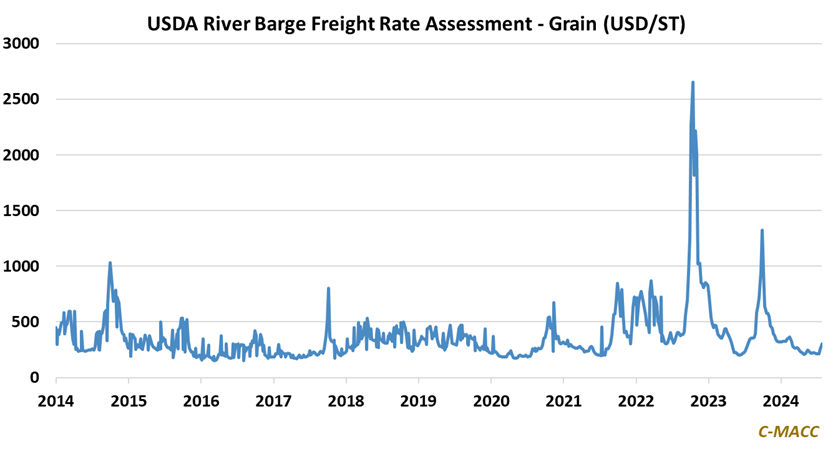

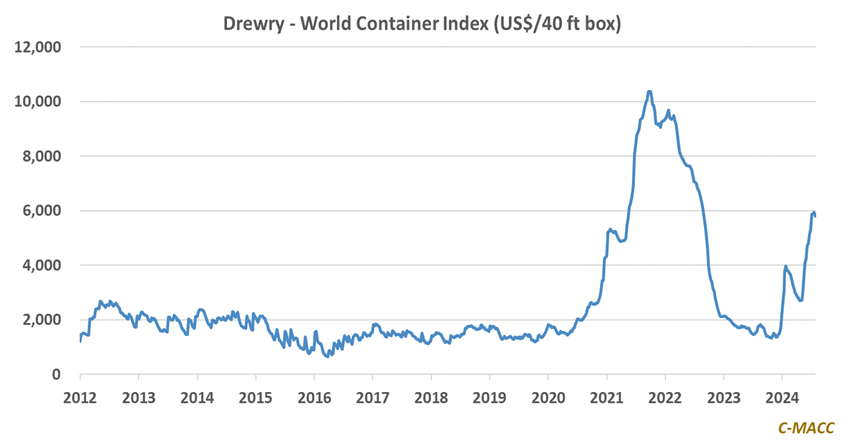

Elevated global freight rates are impacting many industries, including agriculture! A typical rule of thumb is that the US exports around ~20% of its agriculture sector production, which can range from 75% for cotton to 10% for beef, and we flag an article from earlier this year, US Dominance in Corn Exports on the Wane Due to Brazilian Competition, which notes that almost 60% of world corn exports come from the US and Brazil. Though diesel prices and the ability to move crops between US states have fallen back to normal, the uptick in global freight rates, shown below, is something worth considering in terms of the cost of moving excess crops from the US to other regions. And, we now point you to another article, Ripple Effects of Shipping Lane Disruptions on U.S. Agriculture, to show the more direct impact on the exportability of US grain into harvest, which could work to keep domestic markets well supplied compared to net importing regions. As highlighted above, farmer income is already taking a hit with lower crop prices, and we also flag the CNH Industrial views below that suggest that farmer spending in some categories is taking a hit, which is also supported by recent updates from agriculture equipment seller Deere. All in, given higher costs to export and the potential for domestic crop demand to not take off further in many areas near term, regarding bio-product production and considering this article from yesterday noting that EIA: US fuel ethanol production reaches record high 1.109 million barrels per day, we see a long crop market in 2H24, on average, absent a production disruptive weather event before likely improved conditions in 2025/26.

- Bunge Reports Second Quarter 2024 Results

- Bunge shares slide after quarterly profit miss

- CNH Industrial lowers profit forecast on slow farming products demand

- Hershey trims annual forecasts as higher prices dent demand

Exhibit 17: US domestic barge freight rates for grain are within the 2014-2021 range, suggesting domestic movements of crops between states and to exporting facilities is unlikely an issue… however, …

Source: Bloomberg, C-MACC Analysis, August 2024

Exhibit 18: …global freight rates remain elevated, and particularly between certain routes, such as between the US and Europe, and China. We also flag that Maersk hiked its 2024 outlook again as Red Sea disruption boosts profit

Source: Bloomberg, C-MACC Analysis, August 2024

Someone is making money in the food chain! When you compare news about the weakness in crop prices with the continued rise of grocery prices, someone must be doing well within the chain. Still, the industry has other inflationary inputs, which include labor and logistic costs, although not enough to fully offset the better ingredient pricing. As we noted yesterday, and in a couple of recent reports, we see the Ag and farming slump setting up for a robust recovery possibly as soon as 2025, because we are running out of farming yield gain levers and we are seeing another potential demand vector for crops, as feedstocks into renewable fuels and materials. For now, however, farmers are making little money, and the consequences for Deere and other equipment suppliers is that we will go into a period of minimal purchases, especially as recent high farm incomes likely means that the equipment fleet is quite young. 2025 could be a better year for crop prices but not much of an improvement for input and equipment producers – who would then see a rebound in 2026.

- Corn and Soybeans Make Fresh Lows: Is the Pressure From Supply or Demand?

- EXCLUSIVE: John Deere Speaks Publicly For the First Time About Layoffs, New Challenges in the Ag Economy

- Layoffs pile up in US, Canada as companies uncertain of economy

Hydrogen Economy – Weekly Theme: Stacking the hydrogen odds in your favor means low-cost everything

- The economic challenges of hydrogen require critically important economies of scale in any business model that stands a chance of working; this is the arena of well-financed companies, not start-ups.

- At our very well-attended dinner last week, there was broad consensus that buyers willing to pay a lot more for products with a clean hydrogen component are elusive, but cost-competitive products will take share.

- Companies bringing unique technology to the hydrogen party, whether on the production or consumption side, should look for deep-pocketed partners or simply license what they have – less risk and more chance of success.

- We continue to see a wave of green European projects passing FID, as companies look to capitalize on grants and government incentives geared to see which country can subsidize the most – blue is so much cheaper.

- With crop prices weaker, grey ammonia pricing is not strong (although far from a cyclical low), and this market is influencing price discovery for other colors. We see a grey price rebound, possibly in 2025.

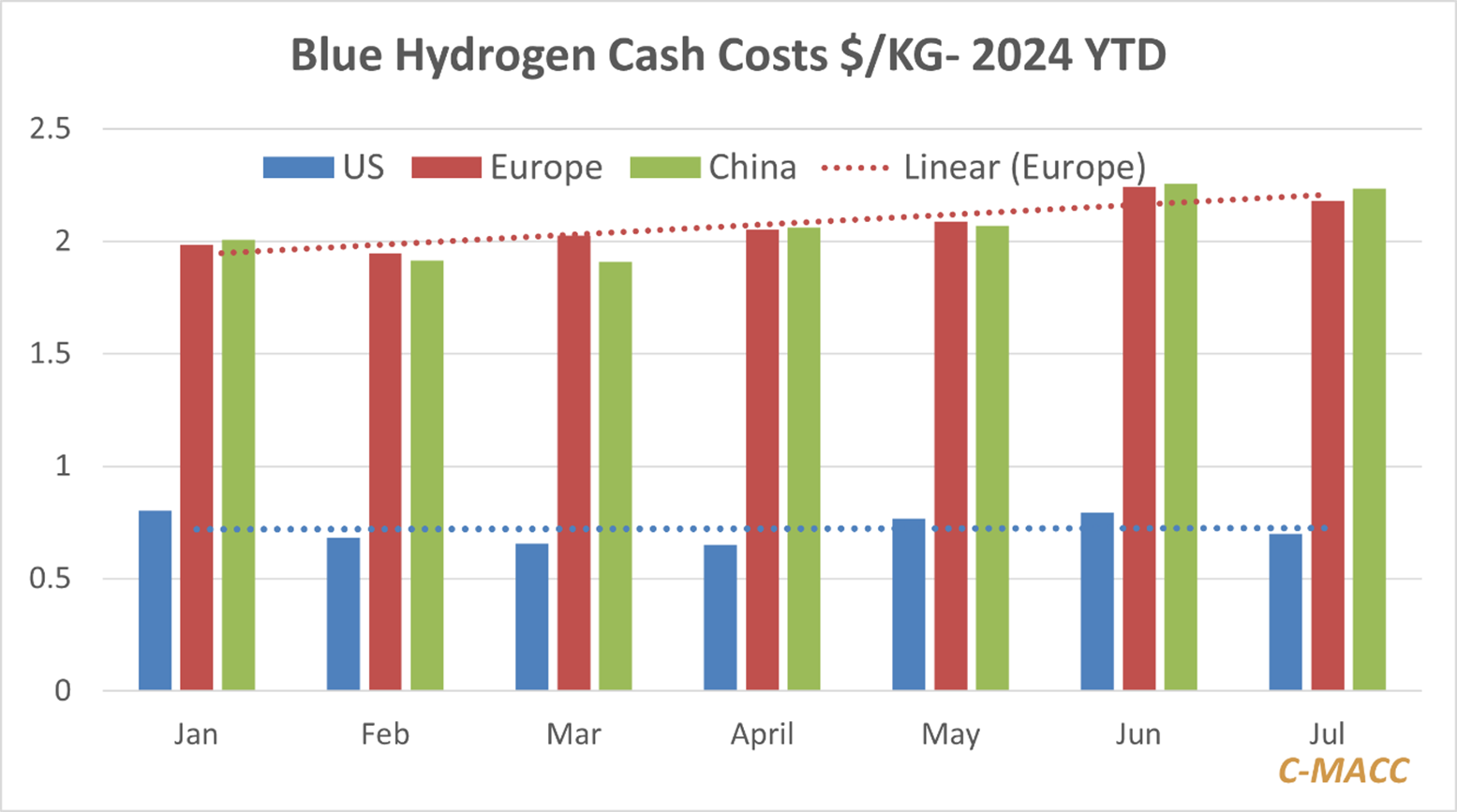

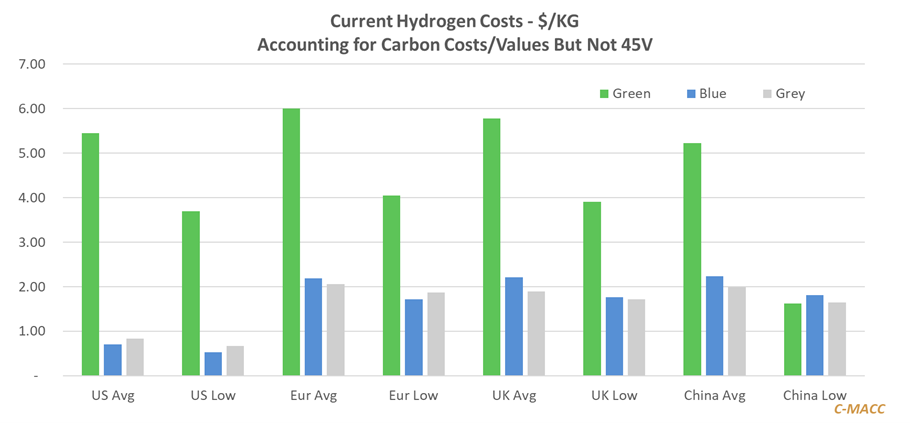

Exhibit 19: Despite the US competitive edge in blue hydrogen, only the best positioned can make the math work.

Source: Bloomberg and C-MACC Analysis – This chart shows our high ranges for each region.

The chart above suggests that all the blue hydrogen investments should be in the US and the chart below suggests that blue is the way to go unless you are in the low-cost region of China. Yet, even with the advantaged natural gas position in the US, we see blue hydrogen and ammonia struggling to compete with grey hydrogen and ammonia and potential buyers who feel that it should. If Europe had a better feeling towards blue versus green, then the exhibits would support building blue in the US to support Europe all day long, saving Europe billions of dollars versus the local green path today. Germany accepts the challenges of local production by acknowledging that 70% of 2030 supply will be imported – see headline below – but by insisting that it is green will keep prices very high. With a bit of local price support, the US could build a large and very competitive decarbonized industrial and chemical sector based on blue hydrogen, but for now, most of the US projects are building FID-focused economics based on export netbacks from Asia and, in some cases, Europe. Note that the rising trend in Europe in Exhibit 19 is a function of both the increase in natural gas prices and the decline in carbon values. Carbon values in Europe and the UK are falling as industrial production slows, which is negatively impacting the economics of many proposed projects.

Exhibit 20: Green makes little sense on a cash-cost basis, and when you account for capital costs and capacity factor adjustments, the costs move much higher.

Source: Bloomberg and C-MACC Analysis

But blue economics today only work if you can optimize everything – the cost of capture and sequestration, hydrogen logistics, capital, and operating synergies. The independent projects in the US (blue or green) need guaranteed construction costs to get financing, and this drives higher costs because the EPC companies build in higher contingencies than they would for a time and materials contract. If you are paying someone to handle your CO2 capture and disposal, that third party needs a margin, and if you then need hydrogen logistic support, that can also eat into a margin. The consequence of all this is the need for take-or-pay contracts with prices that are too high. You need the balance sheet so that you are not hostage to funding challenges, and you need optimal logistics so that you do not give up some of your limited margins. The obvious players in this market are the incumbents, and it is not surprising to see CF Industries, LSB Industries, OCI, Air Products, Air Liquide, Linde, and ExxonMobil in the lead, although not all these projects are yet through FID. There are a host of other plans for blue hydrogen and some for green hydrogen in the US Gulf and for the moment the odds are stacked against all of them.

When you look at the project we are covering today, and most of the recent announcements, they are in Europe and green and are very expensive, much more than we suggest in Exhibit 20, which only looks at cash costs. As we have noted in recent research and covered in our webcast, a recent audit of projects in the Netherlands found actual costs of hydrogen on a full-cost basis in excess of €13 per kg. Most of the green projects we see in Europe are backed by majors, such as TotalEnergies and BP in the projects below, but the grants and subsidies remain huge, or none of the investments would be moving forward. But with European subsidies so high and almost competition between countries to see who can encourage the most uneconomic green hydrogen, there are plenty of independents also pursuing projects and these companies will not have the balance sheets to handle either cost over-runs or customers who find they are no longer competitive with the high input prices.

But one of the exceptions to all this may be the SAF market, coming out of its dive. In some recent reports, we suggested that the SAF market may recover from its steep dive, avoiding some real trouble. The sentiment dive was based on the failure of Fulcrum and the Shell pullback, and the first green shoots of the recovery came from Lufthansa, with its decision to add clean fuel surcharges from January 2025 – today, paying the surcharge is voluntary. The Airbus initiative below is another positive move, but we would argue that the investment in LanzaJet is misplaced, as the real work needs to be done on inputs, such that technologies like LanzaJet can be deployed more broadly. The airline industry is working out that it needs to solve its own fuel problem by investing in the right place and supporting initiatives. The EV industry did this by supporting battery investments and the battery and EV industries did this collectively with lithium – driving much lower lithium pricing today. With corn prices low in the US and ethanol exports high, this suggests an ethanol surplus in the US that could be decarbonized and converted to jet fuel in line with the plans at Gevo. We think this has an important but limited opportunity because the volumes of jet fuel needed could drive corn demand much higher and drive higher pricing – competing with the food chain – which would be politically unacceptable. As noted in prior work, we see one of the most promising routes to SAF through waste and biomass gasification – Fulcrum had the right idea but the wrong technology/process.

- Airbus and partners invest in SAF financing fund

- Airbus Announces Strategic Investment in SAF Technology Company LanzaJet

- Can corn ethanol really help decarbonize US air travel?

- HIF Global and Airbus announce eSAF production partnership

- Singapore launches $90 million SAF and renewables research program

- UK confirms plans to set SAF mandate at 2% for 2025

- HIF Global and Airbus announce eSAF production partnership

Sustainability and Energy Transition: First: Is Any Polymer to Polymer Recycling the Best Use for Plastic Waste

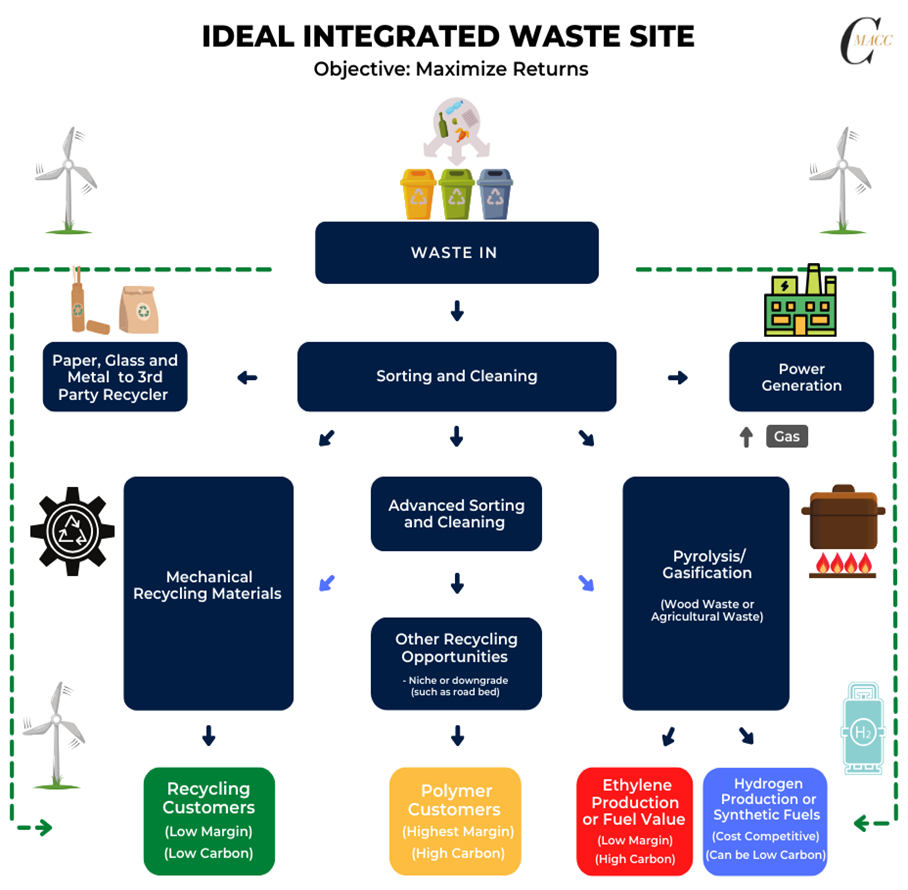

Exhibit 21: C-MACC Ideal Waste Site

Recycle initiatives – too few and too small: We sense that the recycling market has lost momentum, as the news flow around new projects has slowed, and our clients are talking to us far more about the challenges of recycling rather than the opportunities, and this is a reversal of where we were 18 months ago. It is both an expense and a logistic challenge (which, at the end of the day, is also an expense) that is driving a slower pace. As with all sustainability initiatives, if the customer was willing to pick up the tab, things would still be moving quickly, but customers are pushing back on pricing, and this is a large part of the challenge. But we think there is a bigger issue here: the reasonableness of having a circularity goal for plastics when a better objective might be the most value-added way of disposing of plastic waste while maintaining a focus on low-cost and lower carbon polymer production. Chemical recycling of polymers (pyrolysis) is not a low-carbon process, which will likely raise significant challenges for some of these projects going forward. Mechanical recycling will continue to find a home as long as the price is right and the quality of the product is high, but getting enough high-quality input to drive enough high-quality output will also be challenging unless we can improve design, collection, and sorting, all issues that are outside the control of polymer producers.

- Shell calls its chemical recycling goals ‘unfeasible’

- Shell quietly backs away from pledge to increase ‘advanced recycling’ of plastics

- Waste to wealth: unlocking circular value chains

- Plastics sustainability goals pushed back

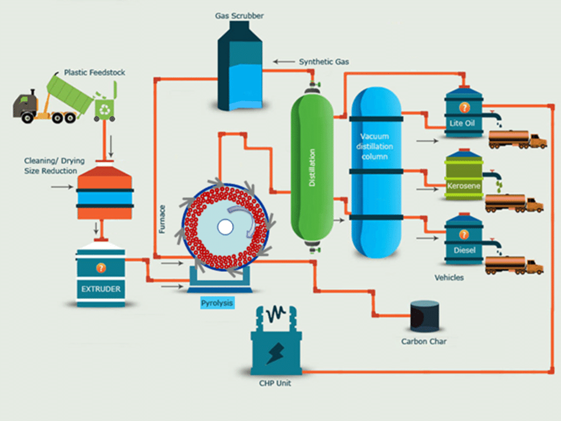

Exhibit 22: This process is high heat and has a high carbon footprint – in some cases higher than virgin production

Source: Researchgate

Trying to get a small amount of adequately pure and clean polymer from a large waste stream to satisfy a focused customer need (food-grade recycled polyethylene, for example) is inherently very expensive. Optimizing the use of the full waste stream could provide much cheaper plastic. The overall challenge with our “ideal” waste site above, is that no one is interested in managing the whole system. Different companies want different pieces or have technologies that can address different aspects of the challenge. The efficiency would come from managing the whole process holistically, optimizing each step to drive the most value for the lowest cost. Simpler still would be a heterogeneous waste stream feeding as a gasification process with a syngas output – many have tried, but all so far have failed, or failed at a cost that makes sense.

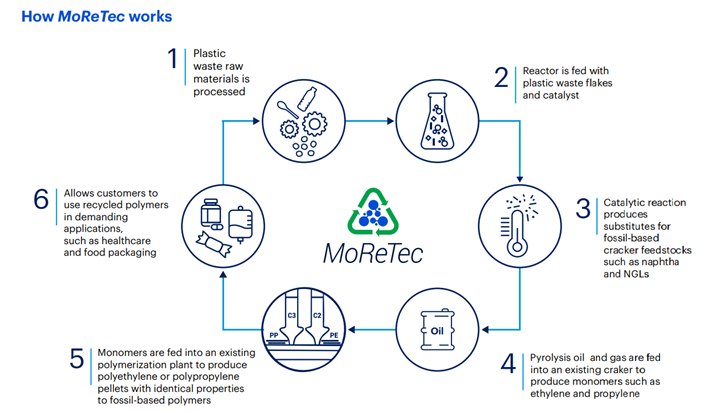

Exhibit 23: In this LyondellBasell flow diagram, the heat component is missing – it will need catalyst and heat

Source: LyondellBasell

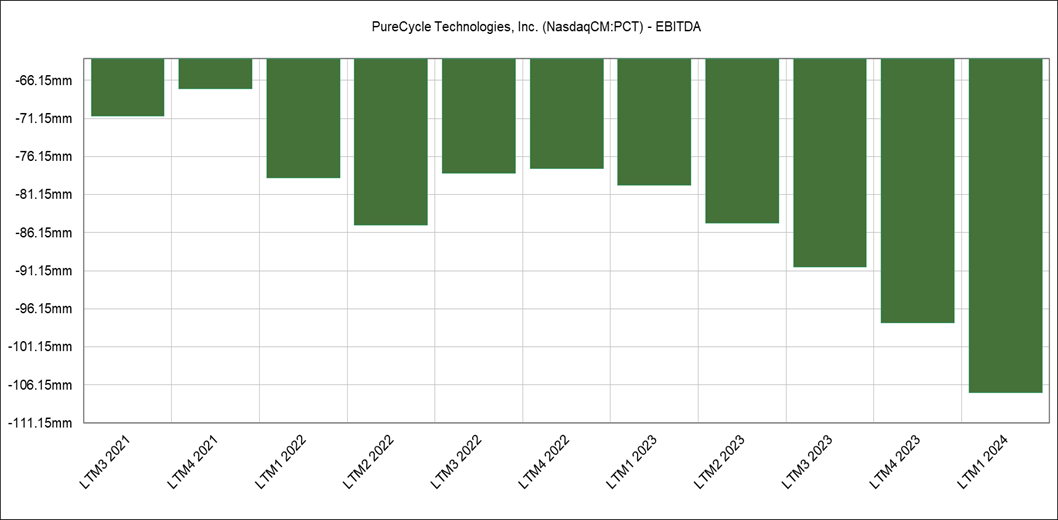

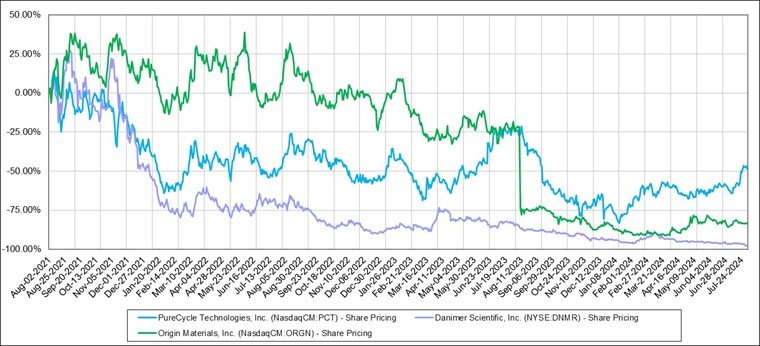

But at the other end of the spectrum, the fortunes of PureCycle suggest that trying to refine a recycling process that is targeting just one polymer is unlikely to succeed. PureCycle is having challenges with technology, access to feed and overall economics. As the charts below note, the stock is doing better than the financials would suggest, especially relative to others.

Exhibit 24: PureCycle Technologies – Losing More Money Each Quarter…..

Source: Capital IQ, 2024

Exhibit 25: …Yet the share price is doing much better than some of the renewable polymer companies.

Source: Capital IQ, 2024

Who will pay for Eastman’s expensive recycled PET. We continue to struggle with the economics of the Eastman molecular route to PET recycling as the capital costs per ton of PET recycled seem far too high to generate a positive return unless the PET produced is selling for a significant premium to virgin polymer. Working in Eastman’s favor is the even higher cost of trying to get to PET from renewable resources, but the Eastman process is much more expensive than the simple collection and mechanical recycling of PET bottles. Having a successful route to recycle PET products that might not be as straight forward as bottles, such as other food packaging, might allow PET to penetrate other markets where circularity is key, displacing products like polystyrene, but polypropylene would likely be a better product given that it can be both mechanically recycled and chemically recycled with polyethylene.

Exhibit 26: Eastman provides an update on the ramp-up of its methanolysis facility in Kingsport with 2Q24 results.

Source: Eastman – 2Q24 Earnings Presentation, July 2024

This is not a business for independents, something that we have noted for other energy transition sectors. Until economies of scale can be developed, this business needs the larger balance sheets of the larger polymer companies, and it is not surprising to see some of the independents selling to the majors. Still, it is not clear that the major polymer producers will make money at this any time soon. Most are in recycling because they have customers demanding recycled content, but at the same time, customers are not willing to cover the full cost of recycling. None of the major polymer producers is likely to be interested in managing the type of integrated business that we suggest in Exhibit 21, as this would mean moving off-piste into broader waste management and technologies beyond pyrolysis and mechanical recycling. Perhaps the ideal site we suggest is better placed with a waste company like Waste Management, but then there would need to be off-take partners to make the business profitable. We have seen private equity dabble in every part of the chain in Exhibit 21, unhappily in most cases. We see the potential for high R&D and development spending returns pushing waste gasification technologies further, marrying the best solid handling technology with the best gasifier and the best syngas capture and use technology. We still think that the better path for all waste is to produce SAF.

The week of July 29th – click on the day or the report title for a link to the full report on our website.

Monday – Weekly Margin and Pricing Analysis

August & Everything After – North American Chemical Producers Benefit from Improved Cost Positions in July; At A 2H24 High?

- Polymer Market Trends: North American polymer production margins, on average, rose WoW, helped by export market support and an improved cost position. US spot PE integrated margins are near a YTD high.

- Chemical Market Trends: US ethylene and propylene prices held up WoW, following strength since the start of the year amid outages and rising derivative demand, and base chemical prices rose in Asia relative to Europe.

- Feedstock Market Trends: USGC ethane prices led global feedstock cost declines WoW, falling considerably relative to Ex-US naphtha values. US natural gas prices declined relative to Brent Crude oil values WoW.

- Agriculture Market Trends: Crop prices, following weakness for most of July, held their ground last week. Western ammonia prices rose last week while US production costs declined, a plus for producers.

US Spot Ethylene & Propylene Margins Strengthened In July, Both To Weaken In 2H24 – Propylene Derivative Prices Most At Risk

- General Thoughts: US spot ethylene and propylene production margins significantly strengthened in July, and we discuss why we see more risk in US spot propylene derivative prices relative to ethylene derivatives in 2H24.

- Supply Chain/Commodities: The North American ethylene chain advantage, in our view, is much more durable relative to propylene, with integrated economics holding less risk than non-integrated economics for propylene.

- Energy/Upstream: We highlight recent strength in overseas natural gas prices relative to Brent Crude oil and US natural gas, USGC ethane at a YTD low, and show the still wide price spread between Asia and US spot propane.

- Sustainability/Energy Transition: We flag BP EBITDA growth drivers supporting its 2025 guidance and strategic and business shifts during the past 12 months and discuss other relevant global sustainability updates.

- Downstream/Other Chemicals: We highlight volume strength by geography at Covestro and Clariant, flag the ADM 2Q24 report showing a crop demand dip and lower crush margins, and discuss other end-market views.

Low Prices Keep Many Green Ambitions In Check; Low Costs Keep Existing Manufacturers In-Play

- General Thoughts: Aluminum is an example of a critical mineral that saw a sharp price decline in July as green sector and Chinese demand failed to meet expectations; it shares similar drivers with many other critical minerals.

- Supply Chain/Commodities: We highlight the DuPont 2Q24 earnings release, highlighting its electronics business, show OMV olefin and polyolefin margin views, and discuss rising global commentary surrounding USGC ethane.

- Energy/Upstream: We highlight US refinery margin trends, which have increased from early 2H24 lows, and flag US refinery capacity additions through 2024, noting recent crude oil price movements and our views.

- Sustainability/Energy Transition: We discuss wind turbine price developments on a per MW basis, flagging the prospect of an uptick into 2025, and the price of carbon allowances in the California cap-and-trade program.

- Downstream/Other Chemicals: We highlight DuPont end-market views from its 2Q24 earnings presentation and discuss the drop in the China PMI index in July. However, signs of China’s exporting excess products remainhigh.

Farm Income Faces Downward Pressure – Input Supplier Profit Impacts Mixed; Crop Consumers Rejoice, For Now!

- General Thoughts: US corn and soybean prices fell to fresh YTD lows this week amid expectations for strong US (and global) production, supporting our weak agriculture economy views for 2H24 ahead of a better 2025/26.

- Supply Chain/Commodities: We discuss chemical sector 2Q reports, including Albemarle, and the different return settings currently facing seed and crop protection player Corteva relative to US fertilizer producer LSB Industries.

- Energy/Upstream: We discuss highlights from a few energy sector results and updates, ranging from Chevron to Shell, and Exelon efforts to boost power delivery with a low-risk plan that we think will likely assure a tight market.

- Sustainability/Energy Transition: We discuss low-carbon hydrogen/ammonia developments at LSB Industries and Air Products, following their 2Q24 earnings calls, and how clean energy subsidies could be assuring trouble ahead.

- Downstream/Other Chemicals: Elevated global freight rates are benefiting shippers, as shown with the Maersk profit guidance increase for 2024, but it is posing an elevated cost for US agriculture exports into some markets.

Cheap & Cheery In The States, Pensive Pounds In Europe – Western Restructurings Underway Amid Global Oversupply

- General Thoughts: USGC ethane prices declined to a fresh YTD low and fell relative to Ex-US naphtha values this week, further lifting the North American ethylene production cost advantage favoring many Ex-US asset reviews.

- Supply Chain/Commodities: We discuss LyondellBasell 2Q results and the strategic review of its European assets, the causes of the Celanese 2024 profit guidance cut, and highlight several other chemical sector business updates.

- Energy/Upstream: We update our petrochemical feedstock data sheet to examine developments in the US, Asia, and Europe to frame cost curve determinants and flag relevant news items, including Exxon and Chevron results.

- Sustainability/Energy Transition: European PPAs, amid a push toward electrification and low-carbon production, remain underway; however, they do not lack challenges, and we discuss several items worth consideration.

- Downstream/Other Chemicals: We highlight YTD volume trends in North American rail traffic, as chemicals are the second strongest AAR category. We also flag more agriculture sector news amid crop price weakness.

Weekly Climate, Recycling, Renewables Energy Transition and ESG Report (CRETER) No 191

Recycling Pull-Backs – There Is No Logical Owner Of An Optimal Recycle/Reuse Plan

- 1st Topic of the Week: We likely need to rethink recycling and instead focus on waste management and driving the optimal value or minimal cost from a waste supply – there is a need to focus on the front end of recycling rather than a business plan that is driven by wanting a small share of the output.

- 2nd Topic of the Week: It’s not just recycling hitting a reset button.

- Otherwise: We look at carbon values that are too low and power costs that are too high.

Weekly Hydrogen Economy Update No 57

It’s a Big Boys Game – But Many of the Big Boys Don’t Want It or Can’t Afford It!

- The economic challenges of hydrogen require critically important economies of scale in any business model that stands a chance of working; this is the arena of well-financed companies, not start-ups.

- At our very well-attended dinner last week, there was broad consensus that buyers willing to pay a lot more for products with a clean hydrogen component are elusive, but cost-competitive products will take share.

- Companies bringing unique technology to the hydrogen party, whether on the production or consumption side, should look for deep-pocketed partners or simply license what they have – less risk and more chance of success.

- We continue to see a wave of green European projects passing FID, as companies look to capitalize on grants and government incentives geared to see which country can subsidize the most – blue is so much cheaper.

- With crop prices weaker, grey ammonia pricing is not strong (although far from a cyclical low), and this market is influencing price discovery for other colors. We see a grey price rebound, possibly in 2025.

C-MACC/PXI Polymer Price Expectations Service

July Monthly – Polymer Price Expectations Report #6

Loading…

Loading…

{/restrict]