Global Market Analysis

Waiting on the World to Change – The Unprotected Sit “Tariffied” As Oversupply Risks Rise; Early 1Q25 Trends Mostly Weak!

Key Findings

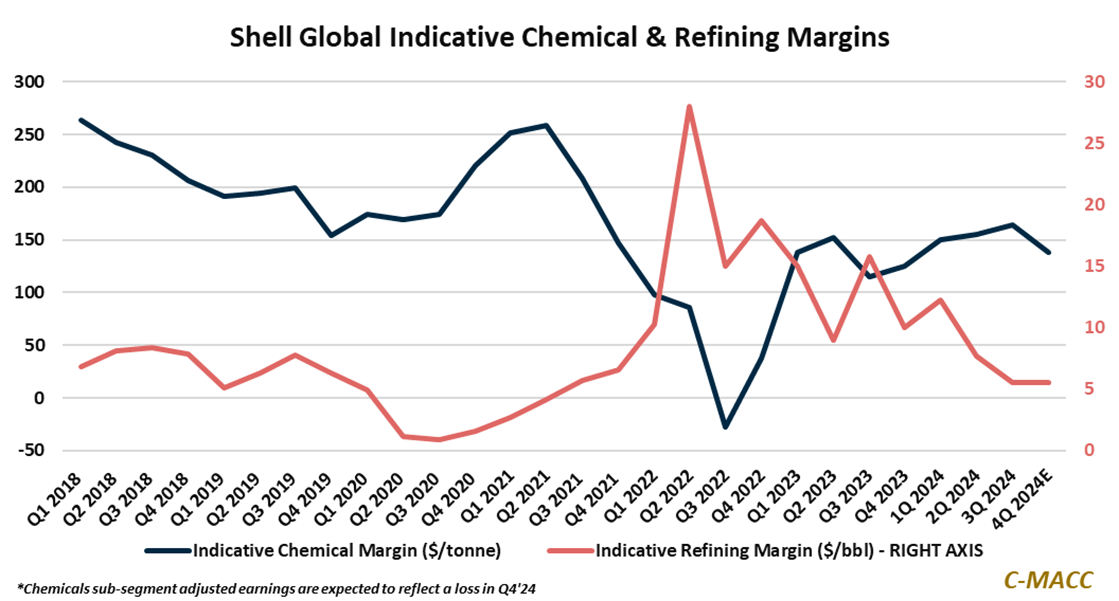

- General Thoughts: Global average chemical and refining margin moves in 4Q24 mostly resemble those shown in Shell’s business update – weaker-than-expected 1Q25 trends are the significant 4Q result reporting season risk.

- Supply Chain/Commodities: We discuss the announced development of another ethylene production unit in India based on imported ethane, which plays a role in India’s effort to build out its domestic petrochemical industry.

- Energy/Upstream: We highlight the Phillips 66 acquisition of EPIC NGL assets, including pipeline and fractionation assets, as part of a trend to lengthen product value chains and bring low-cost products to higher-cost markets.

- Sustainability/Energy Transition: We further discuss SAF use mandates going into effect in the UK and Europe, EU imports of SAF from Asia, what it says about European industry, and flag the airlines most likely impacted.

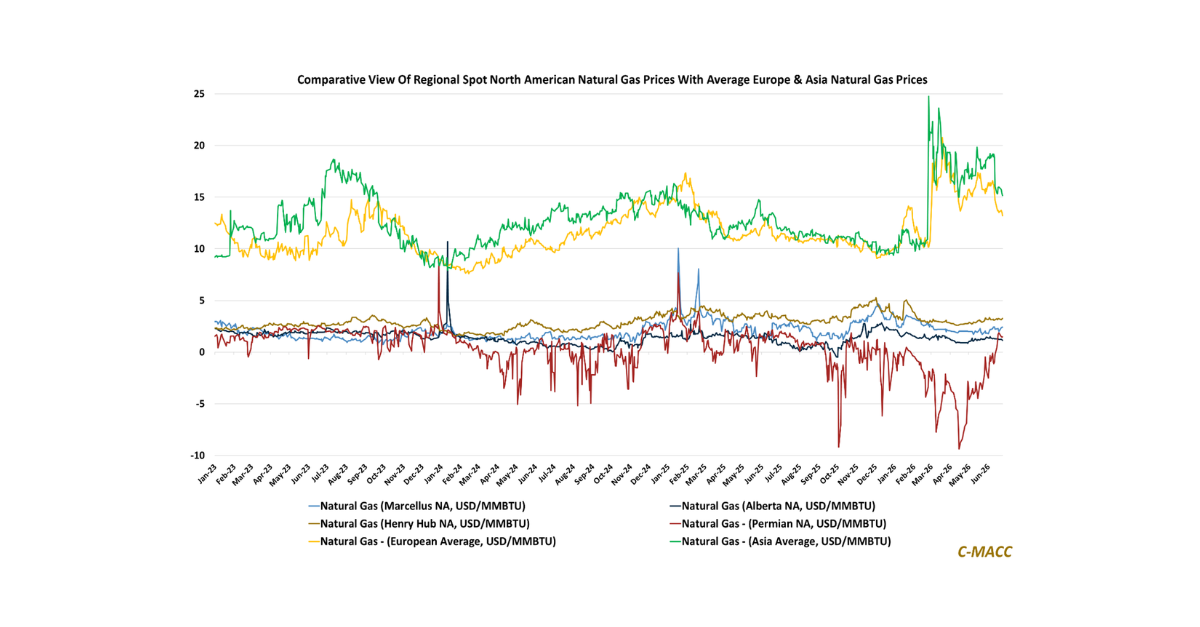

- Downstream/Other Chemicals: The recent strength in the US Dollar relative to the Chinese Yuan and other major foreign currencies is a headwind for US product competitiveness in global markets that has worsened in 1Q25.

Exhibit 1: Shell estimates its indicative chemical margins fell, while indicative refining margins were unchanged in 4Q.

Source: Shell – 4Q24 Business Update, C-MACC Analysis, January 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!