Global Market Analysis

Sitting Still Should Not Be an Option – Global Feedstock Competition to Intensify, Chemical Cost Curves to Adjust

Key Findings

- General Thoughts: Global ethylene market oversupply is resulting in the restructuring and closing of some high-cost capacity, but strategic activities to source cheap feedstock and many capacity additions remain in motion.

- Supply Chain/Commodities: We discuss the SABIC 4Q24 results, its planned petrochemical complex targeted to begin production in China in 2026, and the February US polymer-grade propylene contract settlement.

- Energy/Upstream: We discuss Shell’s 2025 LNG outlook, which is more optimistic about long-term LNG demand than its 2024 outlook, and we highlight movements in European and Asia natural gas prices relative to USGC levels.

- Sustainability/Energy Transition: Chinese solar power additions are poised to slow YoY in 2025, partly due to grid constraints, but will still dwarf additions elsewhere, and we frame the oversupplied setting in solar equipment.

- Downstream/Other Chemicals: We highlight recent movements in the Chinese Yuan relative to the US Dollar, as it is near relative multi-year lows that we view, along with falling freight rates, as positive for Chinese exports.

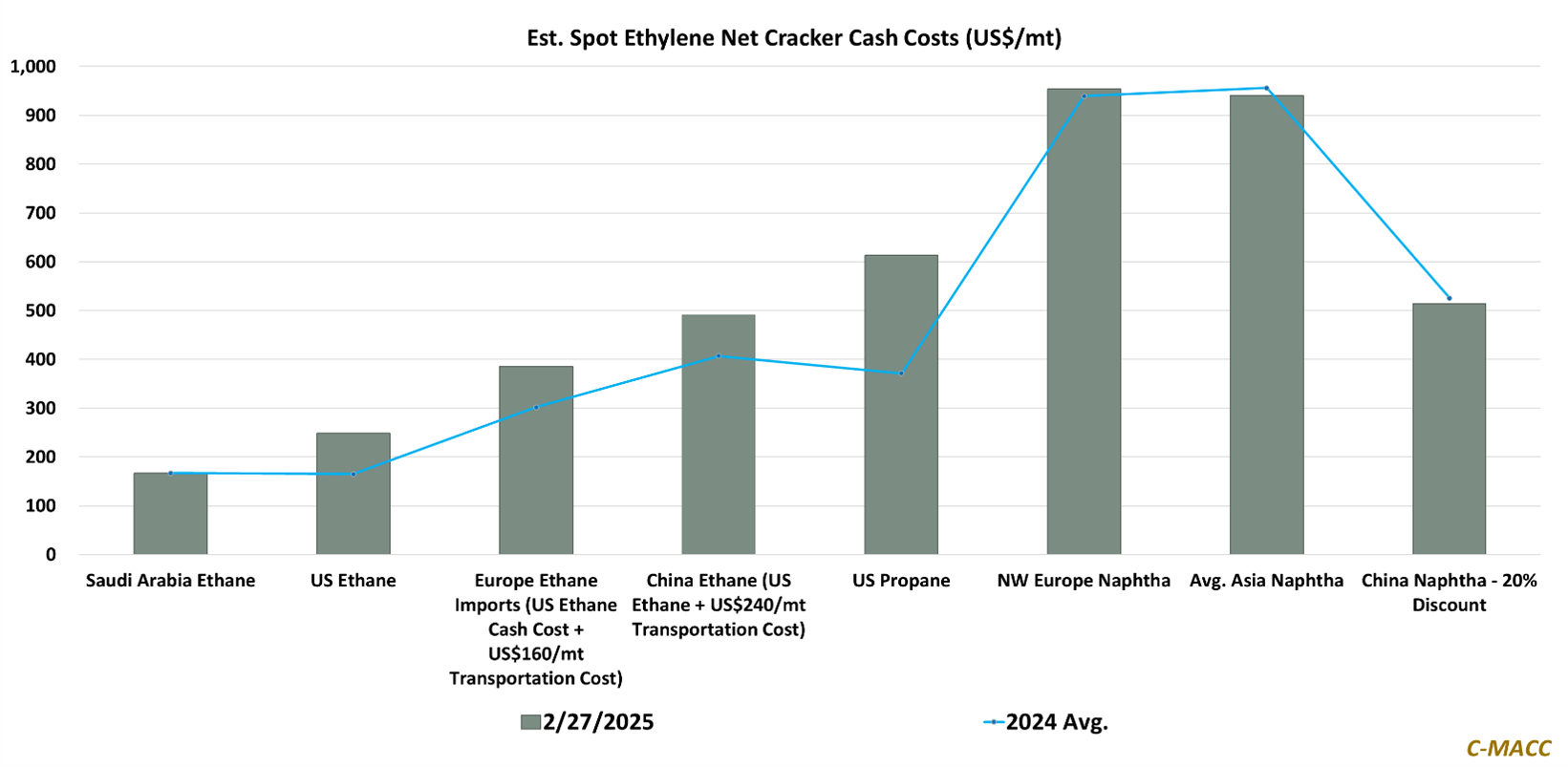

Exhibit 1: Global ethylene markets reflect oversupply, stressing the importance and reviews of existing cost positions.

Source: Bloomberg, C-MACC Analysis, February 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!