Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

- General Thoughts: Global polymer price weakness belies a deeper truth: cost-advantaged, customer-focused players with supply chain agility and strategic clarity are set to lead—not just survive—amid rising market noise.

- Polyethylene (PE): Weak demand, lower feedstocks, and trade uncertainty have reshaped PE market dynamics in 1H25, working to keep supply long despite recent cost curve shifts modestly favoring North American producers.

- Polypropylene (PP): Global PP markets face sustained pressure as weak demand, shifting trade, and regional feedstock imbalances weigh on pricing – oversupply will likely persist in 2Q25, and Western premiums shrink.

- Polyvinyl Chloride (PVC): Global PVC markets remain under pressure as weak construction activity, oversupply, and persistent economic and trade uncertainty will likely limit pricing power and weigh on margins in 2Q25.

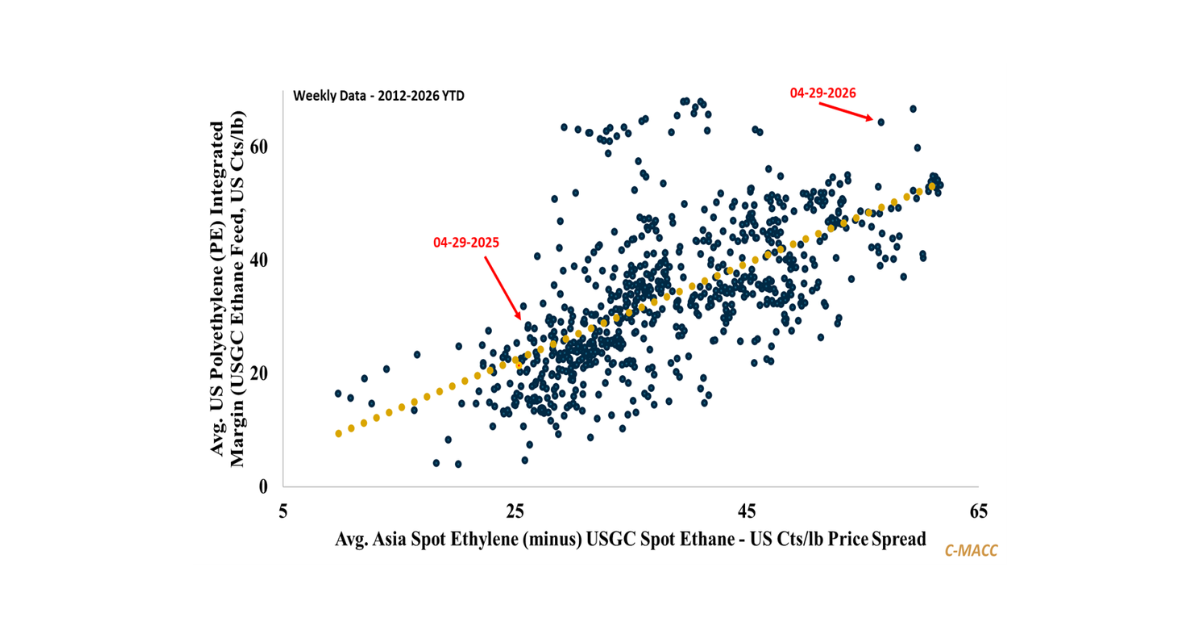

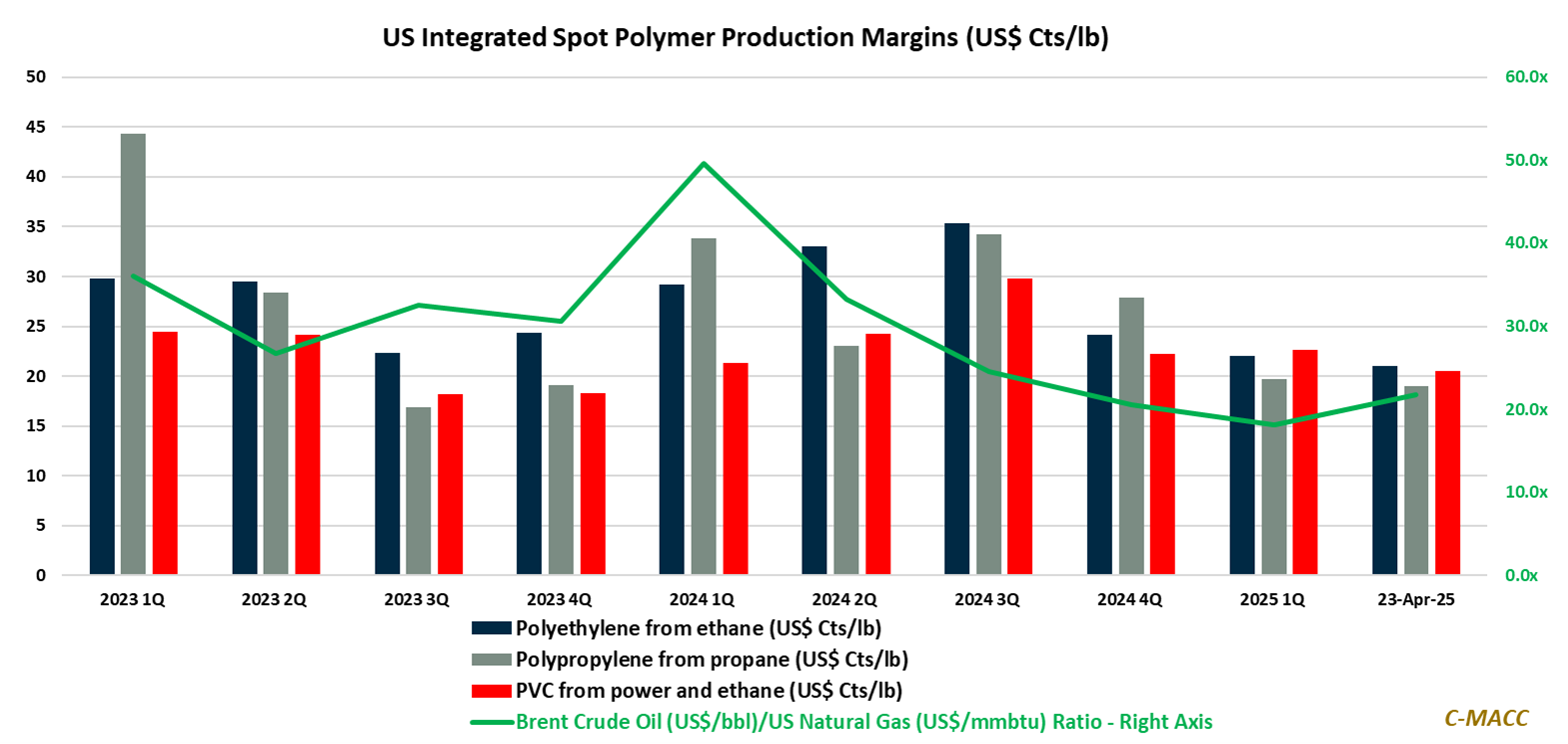

- Other Sector Developments: Recent US ethane price weakness relative to rising propane and stable ex-US naphtha is helping support US PE and PVC integrated margins. Tighter US propane/propylene is hurting some PP producers.

Exhibit 1 – Chart of the Day: US integrated spot polymer margins are slightly below their 1Q25 average.

Source: Bloomberg, Company Reports, C-MACC Analysis, April 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!