Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

- General Thoughts: Misaligned cost curves, fractured trade routes, and demand asymmetry intensify global resin stress, exposing US material to pricing gravity as overseas markets drag benchmarks toward convergence.

- Polyethylene (PE): US PE strength belies global softness, as ethylene divergence, fading export pull, and muted overseas demand foreshadow price convergence by late 3Q absent fresh outages, higher oil or demand shocks.

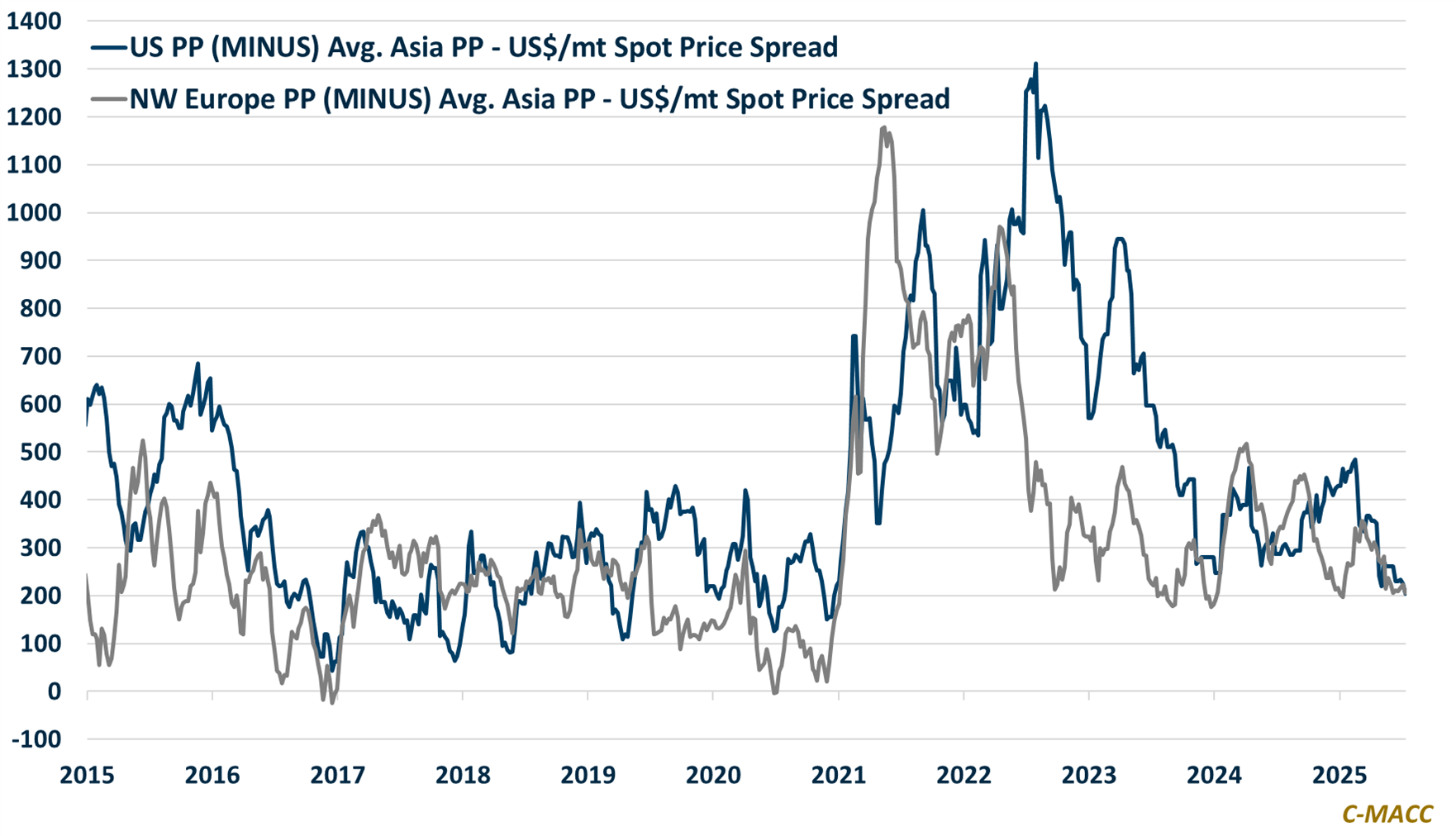

- Polypropylene (PP): Rising Asian exports, collapsing arbitrage, and fresh capacity waves intensify pressure on US PP spreads, as demand inertia and saturated trade lanes point to global convergence by late 3Q25 per our model.

- Polyvinyl Chloride (PVC): PVC faces a precarious reset as oversupply, weak global construction demand, and trade friction persist. Global market balance hinges on output cuts, policy clarity, and downstream recovery by 2026.

- Other Sector Developments: Europe and Asia spot ethylene and propylene prices have weakened relative to US levels, favoring continued stress on overseas resin prices that will ultimately challenge US markets, in our view.

Exhibit 1 – Chart of the Day: US and Europe PP prices will likely face continued downward pressure relative to Asia.

Source: Bloomberg, Company Reports, C-MACC Analysis, July 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!