Global Market Analysis

More Than a Feeling: Ammonia’s Next Moves Aren’t Consensus-Friendly

Key Findings

- General Thoughts: The consensus view calls for ammonia markets to stay supportive, but execution speed, carbon traceability, and certification readiness, not consensus, will dictate who best captures the margin through 2030.

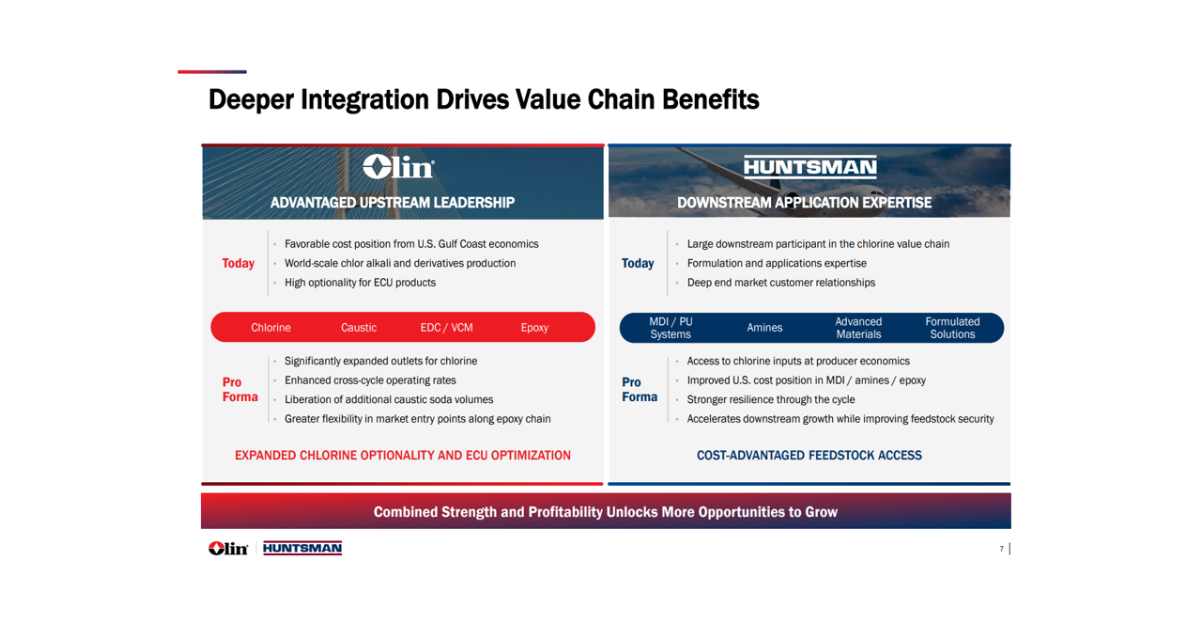

- Supply Chain/Commodities: Yara’s 2Q25 earnings call underscores a pivotal industry shift: capital discipline is no longer optional, and peers will soon echo its prioritization of certified, premium-linked ammonia investments.

- Energy/Upstream: BASF’s Equinor gas deal signals a European energy pivot where carbon intensity defines contract value, a core principle mirrored in 45Q’s reshaping of US oil economics around margin, not output.

- Sustainability/Energy Transition: Rising US ethanol margins in July contrast with pressure in Brazil, revealing a growing imbalance that may reshape trade flows and cost competitiveness in global low-carbon fuel markets.

- Downstream/Other Chemicals: Elevated mortgage rates and weak single-family starts confirm housing’s drag on chemicals, where tepid demand, volatile costs and pricing headwinds keep margin pressure stiff for most in 2H25.

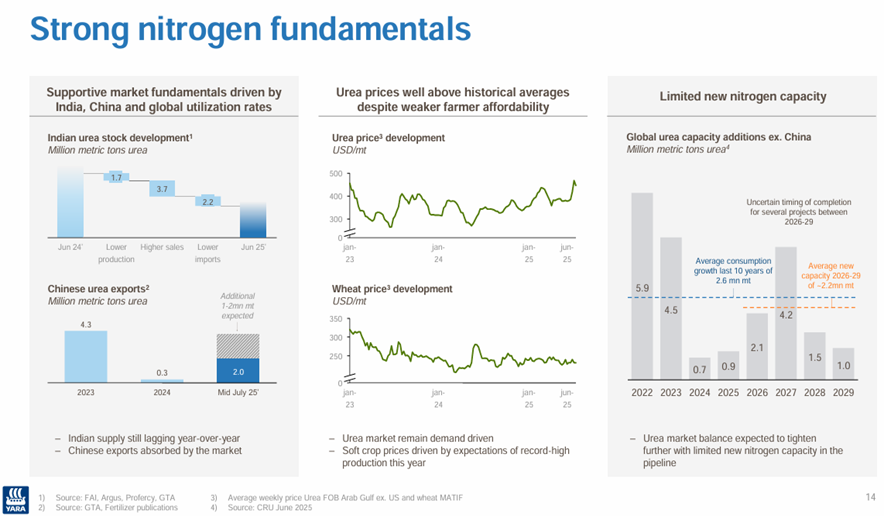

Exhibit 1: A consensus outlook anticipating constructive nitrogen markets favors one thing: greater investment!

Source: Yara – 2Q25 Earnings Presentation, July 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!