Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

- General Thoughts: Europe’s PE price movements across grades YTD underscore how evolving grade-level dynamics now rival cost position in shaping price formation, notably as regional restructuring sharpens strategic focus.

- Polyethylene (PE): Global PE market divergence and grade-level volatility expose a more profound truth: margin resilience now hinges more on strategic adaptability than price hikes or historical cost advantages alone in 2H25.

- Polypropylene (PP): Global PP markets reveal a fragile pricing ecosystem hindered by oversupply, rising capacity, and falling trade competitiveness, leaving PP-to-PGP spreads structurally compressed through a muted 2H25.

- Polyvinyl Chloride (PVC): Global PVC markets remain trapped between weak housing conditions and uneven policy traction, with restructuring hopes and futures-led rallies unable to offset fading demand visibility through 3Q25.

- Other Sector Developments: Despite a mixed monomer and feedstock setting WoW, most upstream price trends and end-market demand developments suggest downward pressure on polymer prices will remain firm in 2H25.

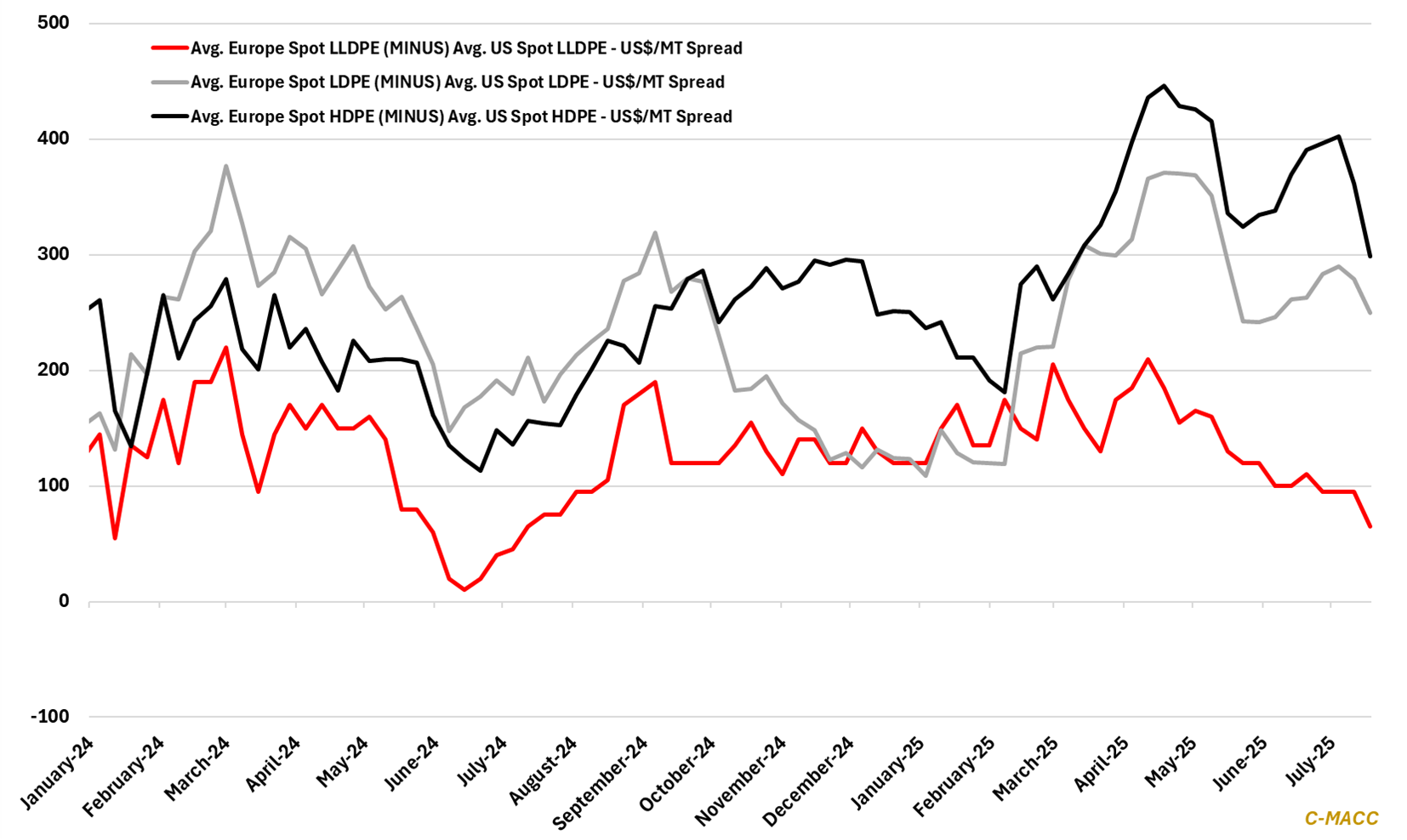

Exhibit 1 – Chart of the Day: European spot HDPE and LDPE prices have risen YTD relative to the US; LLDPE has fallen.

Source: Bloomberg, Company Reports, C-MACC Analysis, July 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!