Base Chemical Global Analysis

Global Weekly Catalyst No. 290

- General Thoughts: Integrated producers with export flexibility and advantaged feedstocks are best positioned to outperform as the global ethylene cost curve flattens and policy-driven volatility reshapes trade flows.

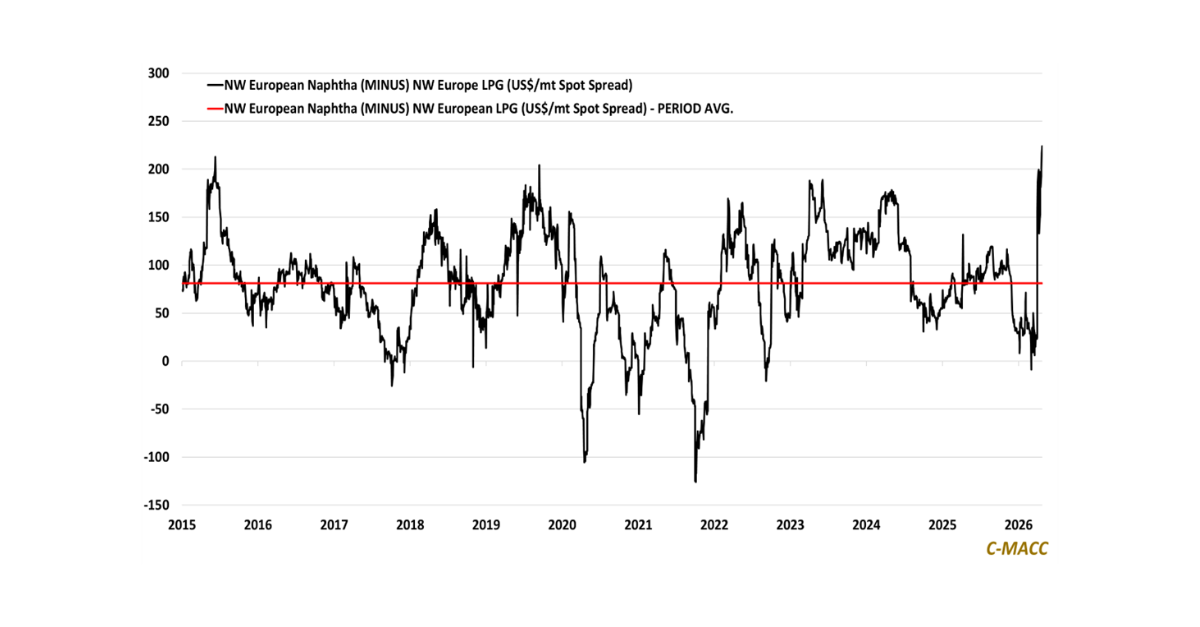

- Feedstocks & Energy: USGC ethane prices moved lower last week relative to Ex-US naphtha values, and US natural gas prices declined relative to Asia and European levels. Most chemical feedstock prices declined WoW.

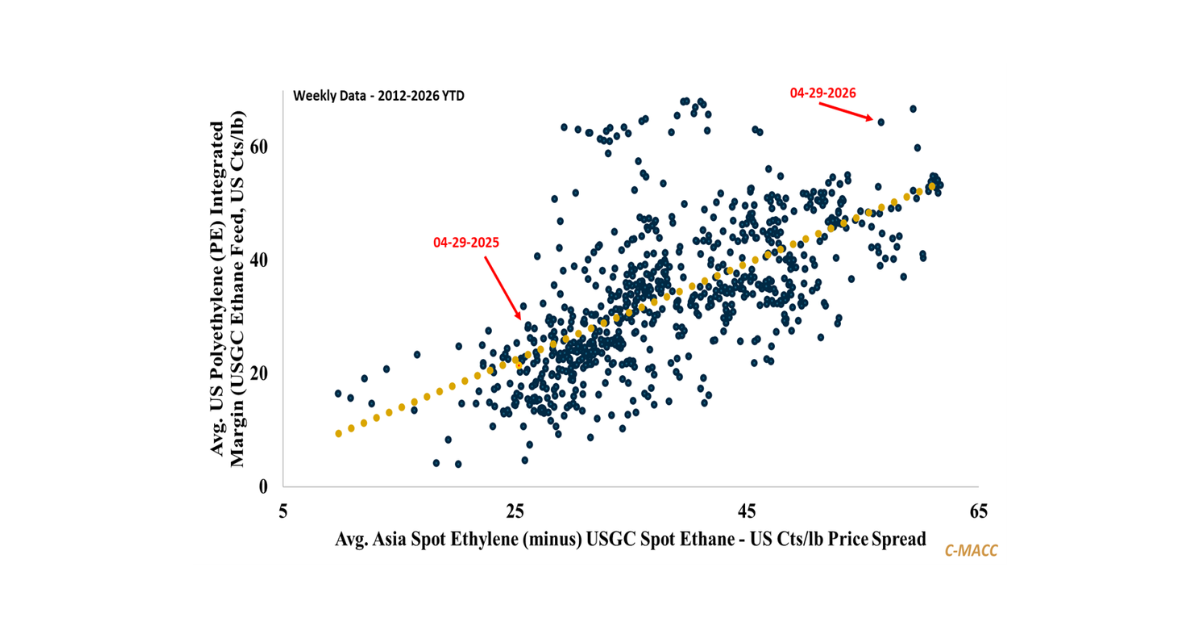

- Olefins: Global olefins markets remain oversupplied, but regional prices were mixed last week. US and Europe spot ethylene values saw strength relative to Asia, while European spot propylene saw the largest WoW decline.

- Other Base Chemicals: US and Asia spot methanol prices improved last week relative to Asia, benefiting North American production margins. Caustic soda price support in China is positive for Western Chlor-alkali producers.

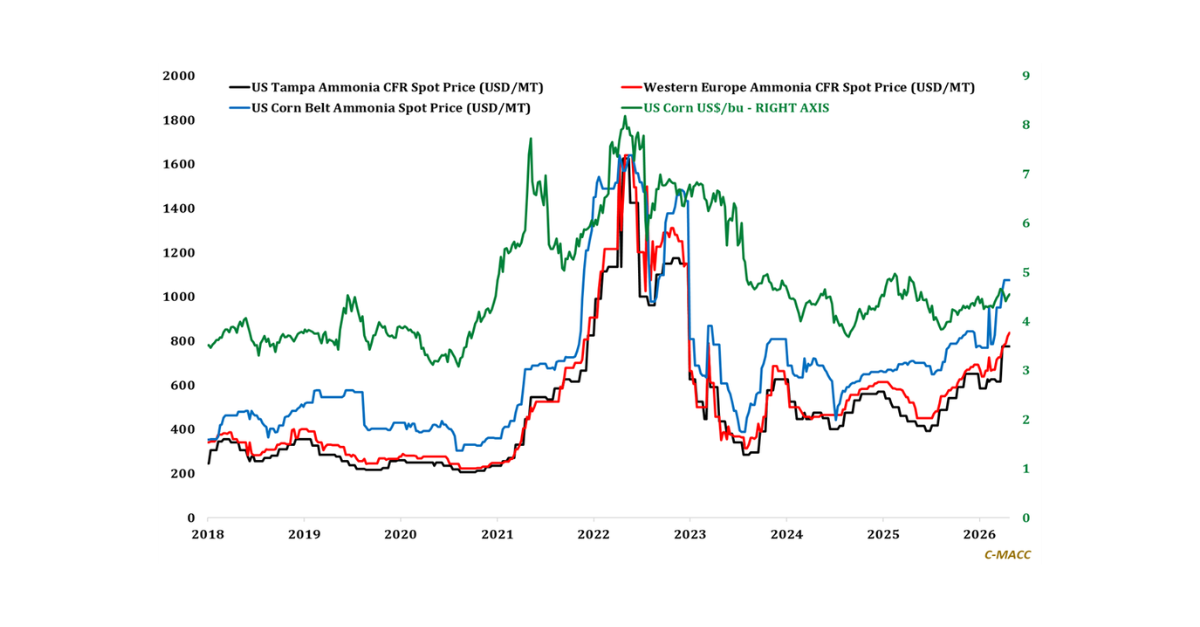

- Agriculture: Global ammonia prices broadly increased last week, with weakness in natural gas prices boosting production margins. With corn prices at a YTD low, we continue to take a cautious near-term demand view.

- Refining & Biofuels: US ethanol production margins increased to a YTD high last week, benefiting from supportive prices and falling corn costs. US refinery margins moved in the opposite direction despite weaker crude oil prices.

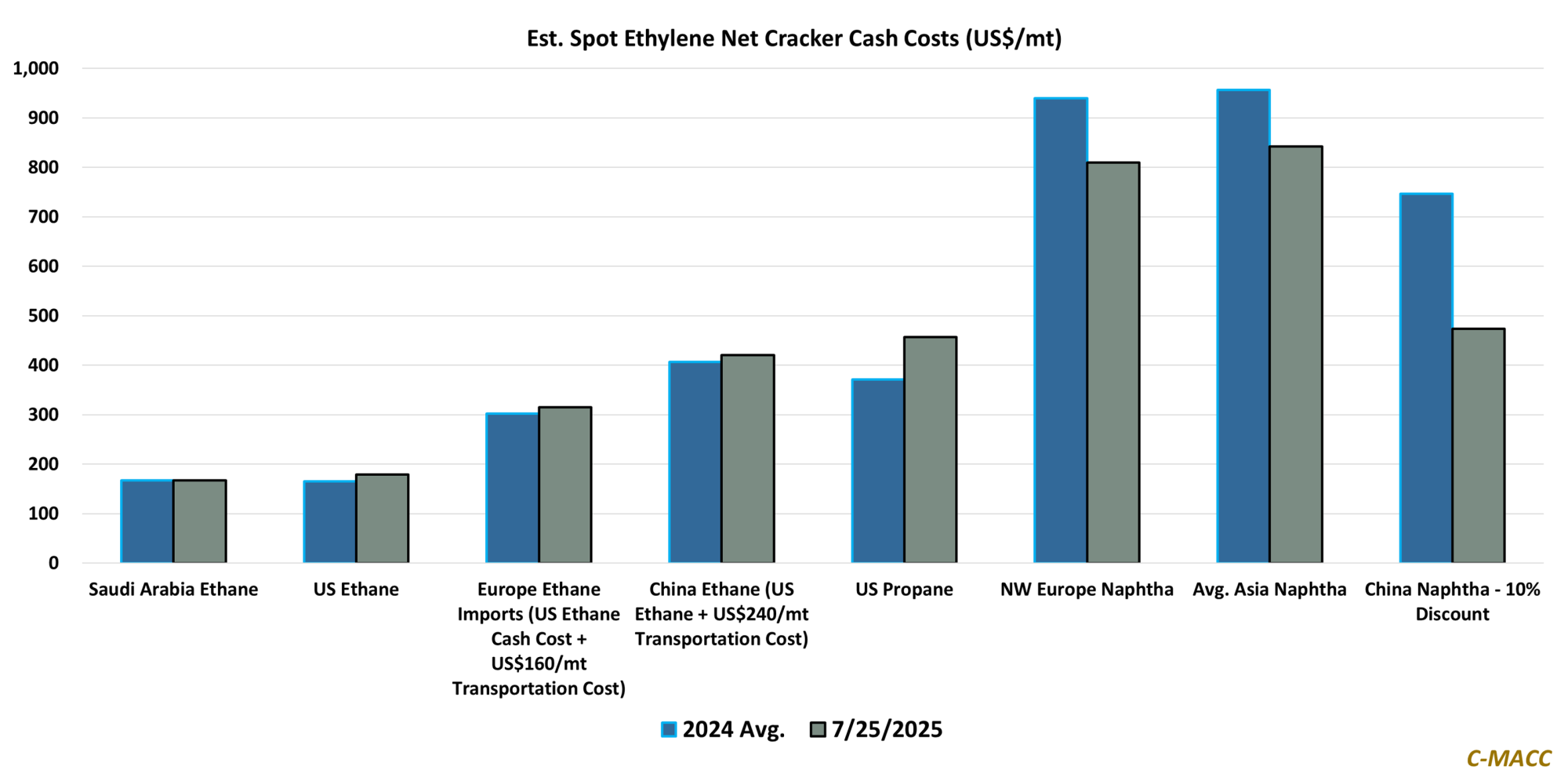

Exhibit 1 – Chart of the Day: Global ethylene production cost curve flatter YoY; likely to remain compressed into 2026.

Source: Bloomberg, C-MACC Analysis, July 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!