Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

- General Thoughts: Global polymers struggle to pivot from trough to transition as trade fragmentation, regional cost asymmetry, and structural demand divergence reorder advantage, hurting laggards and benefiting integrated leaders.

- Polyethylene (PE): Global PE markets fracture along structural lines as advantaged producers gain market share, while trade friction, pockets of intense localized stress, and rationalization pressure reshape competitiveness.

- Polypropylene (PP): Global PP markets face mounting margin pressure amid weak demand, rising Chinese supply, and continued PP-to-PGP spread pressure, leaving integrated players best positioned to weather 2H25 volatility.

- Polyvinyl Chloride (PVC): Global PVC resin markets remain oversupplied and regionally fragmented, with those integrated into building products best poised to perform amid a continuation of weak conditions in 2H25.

- Other Sector Developments: We view crude oil price shifts, US hurricane disruptions, and trade policy movements as significant wild cards for 2H25; we see polymer prices mostly staying near or returning to 1H25 lows in 2H25.

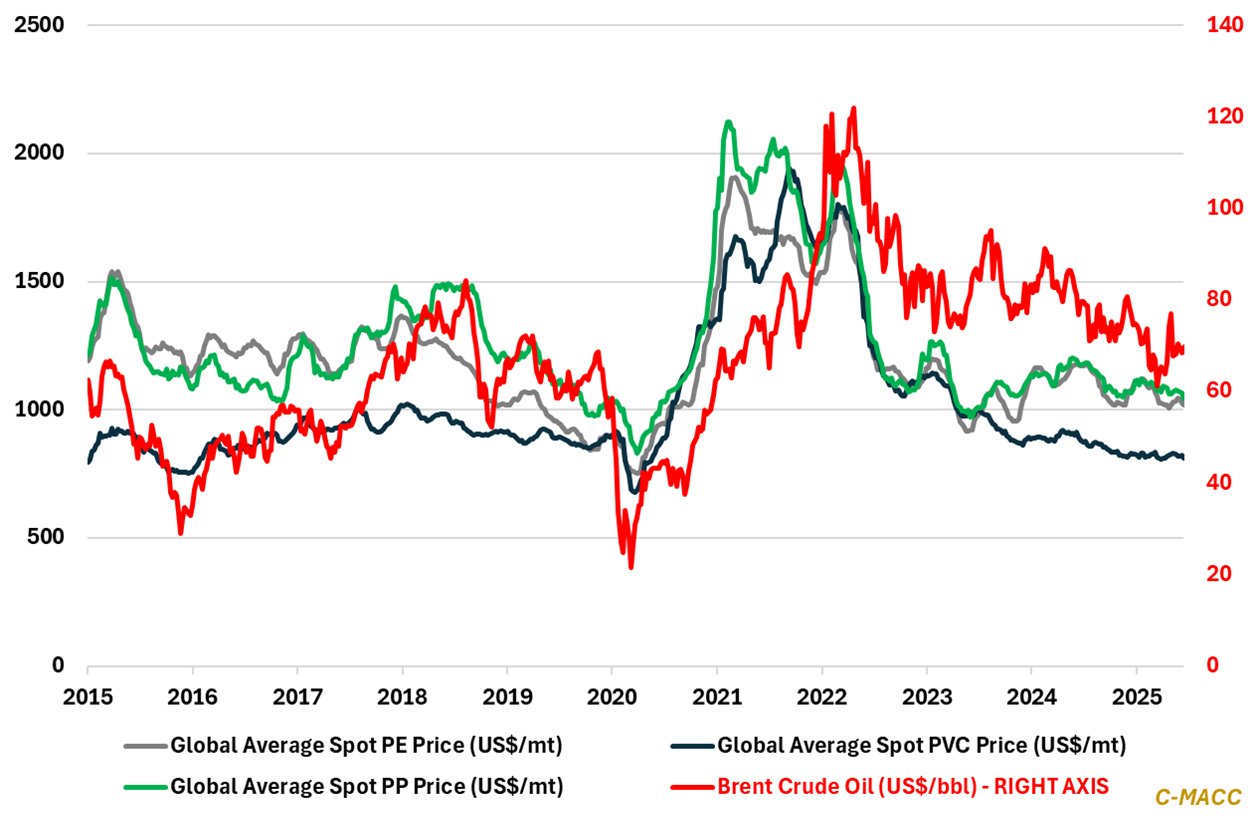

Exhibit 1 – Chart of the Day: Global average spot polymer prices remain near 2025 lows; unlikely to surge in 2H25.

Source: Bloomberg, Company Reports, C-MACC Analysis, August 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!