Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

- General Thoughts: Global polymers face persistent oversupply and cost gaps; India’s protectionism and South Korea’s restructuring show diverging policies shaping markets, demanding margin defense and portfolio discipline.

- Polyethylene (PE): Global PE markets remain oversupplied, with weak demand and soft feedstocks reinforcing structural price pressure and profitability headwinds likely persisting across most markets into late 2025.

- Polypropylene (PP): Global PP markets remain under considerable strain, as Chinese exports and new production capacity overwhelm demand, ensuring profitability challenges for non-integrated players persist across regions.

- Polyvinyl Chloride (PVC): Global PVC markets remain imbalanced, where oversupply, weak housing demand, and volatile feedstocks sustain downward pressure, with profitability headwinds likely enduring for most in 3Q25.

- Other Sector Developments: Recent weakness in petrochemical feedstocks and weak demand remain headwinds to global polymer prices. Government policy and global restructuring actions are rising, likely further intensifying in 2H25.

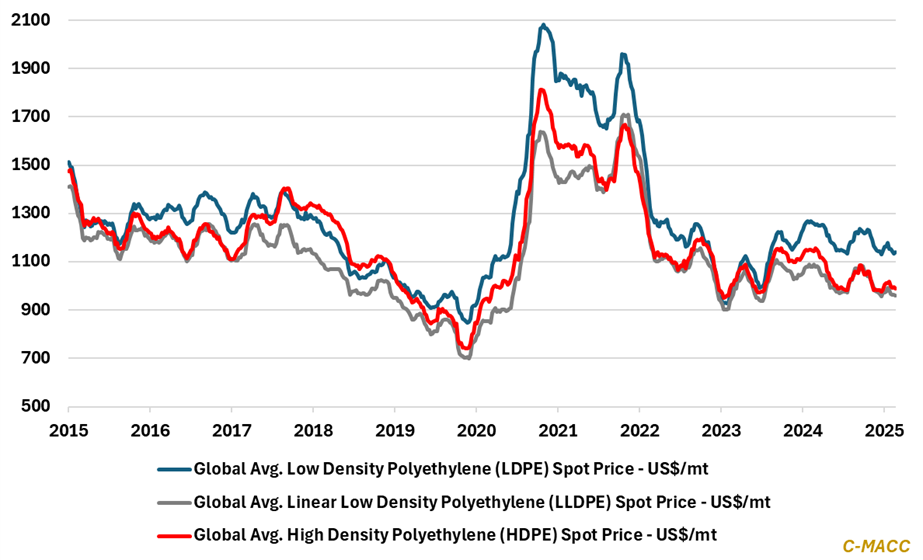

Exhibit 1 – Chart of the Day: Global spot LDPE continues to command an outsized premium relative to HD and LLDPE.

Source: Bloomberg, Company Reports, C-MACC Analysis, August 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!