C-MACC Sunday Executive Summary

Poly-‘Ticks’: Politics, Tariffs, and Squeezed Resin Margins

- Trade fractures are posing challenges to US and Canadian PE cost positions, as Brazil’s ADDs, India’s tariffs, and Turkey’s discounts force its producers into compressed netbacks and volatile, policy-driven trade flows.

- Latin America embraces import substitution, with Pemex’s planned revival, Braskem’s struggles, and Dow’s Argentina hedge reshaping flows and undermining North American reliance on historic regional outlets.

- Ownership clarity eclipses feedstock advantage, as Shell’s Monaca shows that even cost-advantaged assets can become stranded when portfolio fit, geography, and policy exposure diverge from corporate strategy.

- Global market leaders will master agility, embedding tariff shocks, diversifying footprints, and integrating into niches downstream, while laggards clinging to feedstock cost curves risk structural marginalization by 2027.

- Otherwise, capital discipline, stalled FIDs, and fragile policy agendas ensure blue ammonia, methanol, and energy transition markets favor incumbents with secured offtake, integration, and resilience.

- Companies Mentioned: Pemex, Braskem-Idesa, Dow, Shell, BASF, Yara, CF Industries, Woodside, LSB Industries, Enterprise, Energy Transfer, Oneok, Enbridge, Phillips 66, Valero, Methanex, OCI, Corteva, Nutrien

- Products Mentioned: Polyethylene (PE), HDPE, Ethylene, Ethane, Ammonia, Methanol, Formaldehyde, Natural Gas, LNG, Crude Oil, Gasoline, Coal, Fertilizer, Corn, Soybeans, Biofuels, Ethanol, UAN, Marine Fuels, SAF (Sustainable Aviation Fuel), Biodiesel

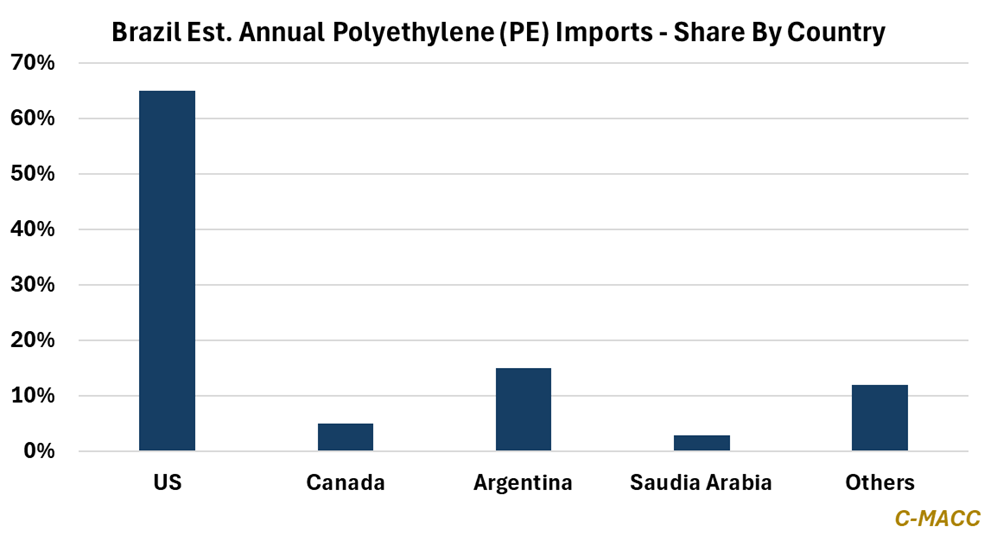

Exhibit 1: US and Canadian PE resin comprises ~70% of Brazil imports, accounting for ~40% of its total PE demand.

Source: C-MACC Estimates, August 2025

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!