Global Market Analysis

Restructure, Punt, Or Invest: Supply Chain Darwinism Meets Capital Cannibalism

Key Findings

- General Thoughts: Global petrochemical markets are fragmenting into low-cost survivors and policy-backed strongholds, with capital fleeing high-cost regions and shifting to logistics, insulation, and strategic scale.

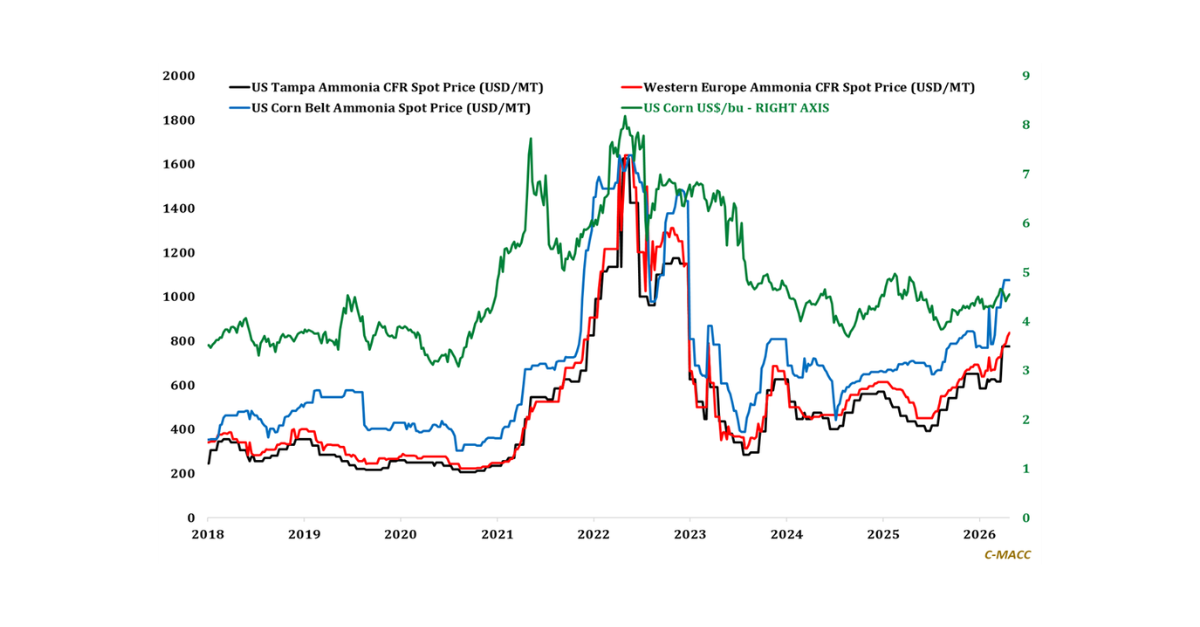

- Supply Chain/Commodities: Heading into 2026, ammonia margins will be defined less by new capacity, more by freight control, cost structure, and low-carbon optionality; those who control supply should outperform.

- Energy/Upstream: Global energy flows are realigning into politically fortified corridors, as Russia and China expand eastward infrastructure to secure pricing power, bypass sanctions, and reshape trade dynamics.

- Sustainability/Energy Transition: Sustainable plastics markets now favor players who control low-carbon feedstocks and meet global certifications; price no longer defines scale, margin, or market relevance.

- Downstream/Other Chemicals: Global freight softness and currency misalignment amplify China’s export edge, reshape trade baselines, and expose weaker exporters to margin compression and structural deflation risk.

Exhibit 1: Petrochemical asset restructuring and proposed asset sales are mounting across high-cost markets.

Source: Bloomberg, C-MACC Analysis, September 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!