Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

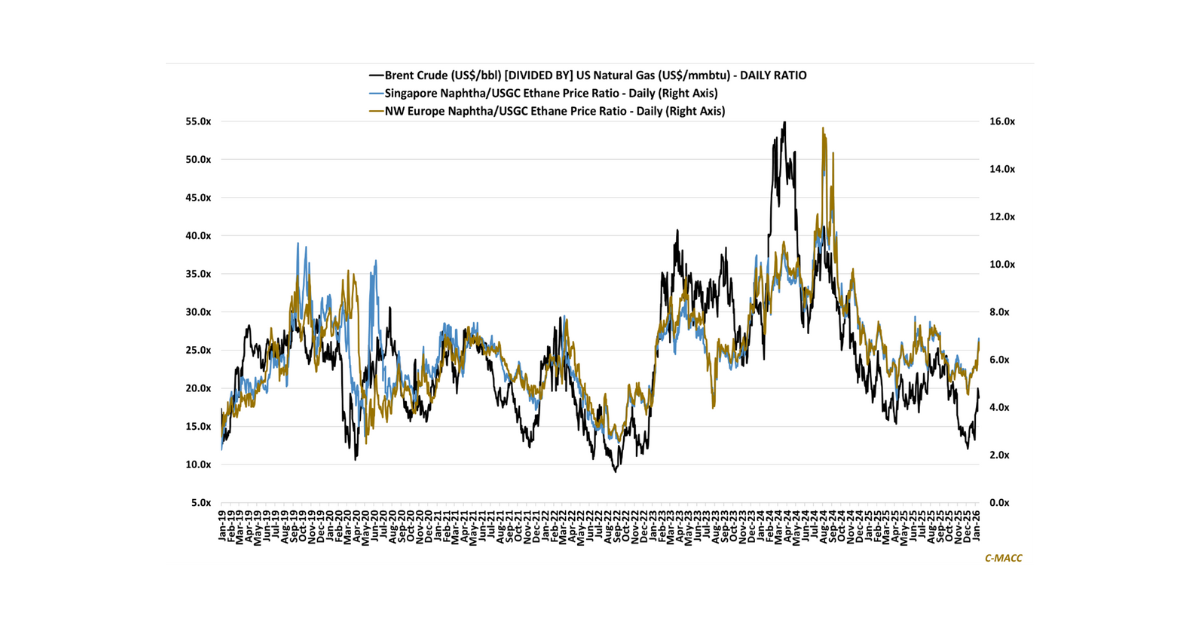

- General Thoughts: Global polymers are entering a structural reset period where energy asymmetry, policy defense, and oversupply, not demand cycles, are redefining cost advantage, rationalizations and long-term product competitiveness.

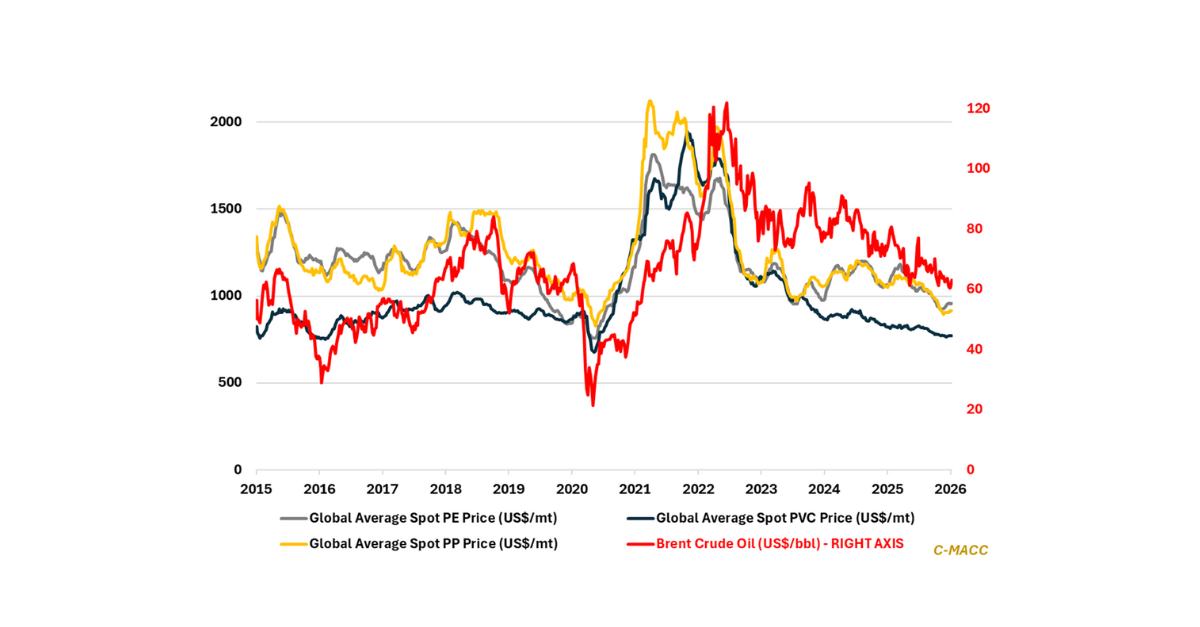

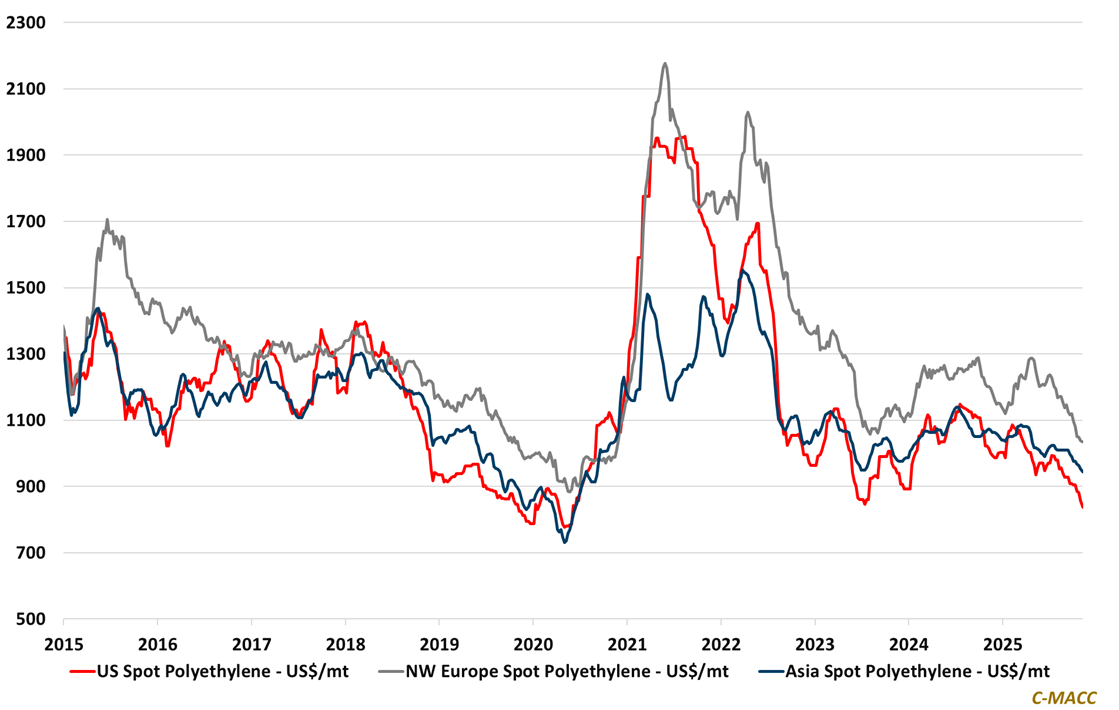

- Polyethylene (PE): The global PE production cost curve is flattening as range-bound naphtha values and USGC ethane price inflation signal a new equilibrium below historical margin norms as regional markets rebalance amid oversupply.

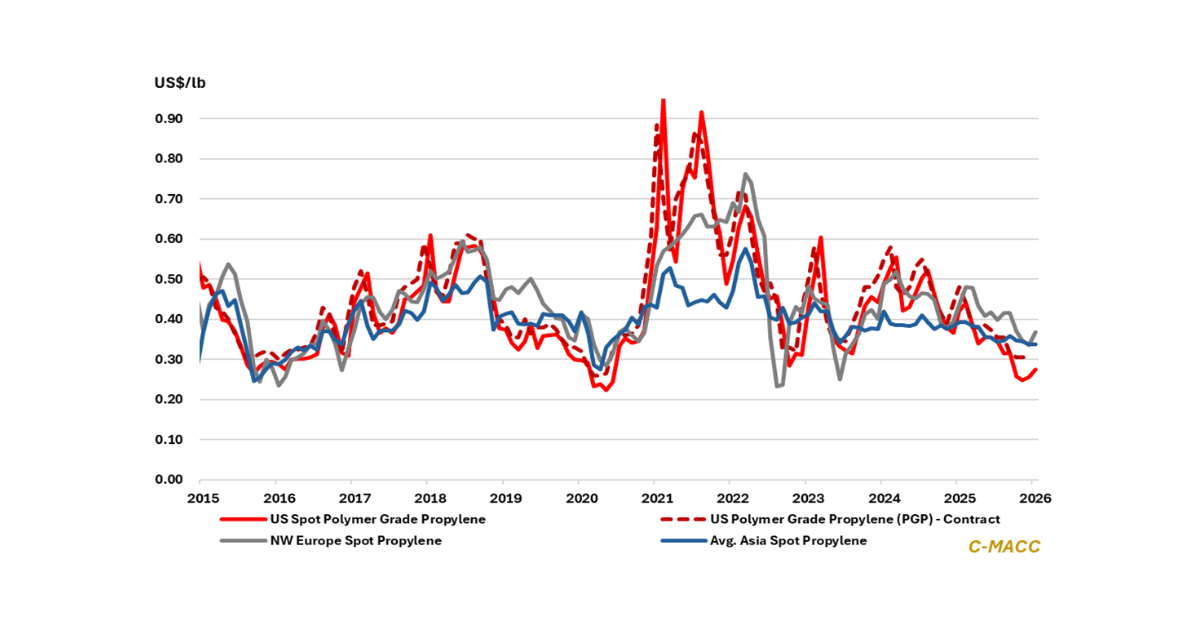

- Polypropylene (PP): Global PP markets stand at the epicenter of China’s industrial self-sufficiency drive, where relentless capacity additions and gradual rationalization are rewriting pricing power shifts as producers struggle to drive returns.

- Polyvinyl Chloride (PVC): The surface stability surrounding the global PVC market in mid-4Q25 masks deeper stress as tighter energy spreads, trade barriers, and shifting supply chains expose the industry’s fragile regional interdependence.

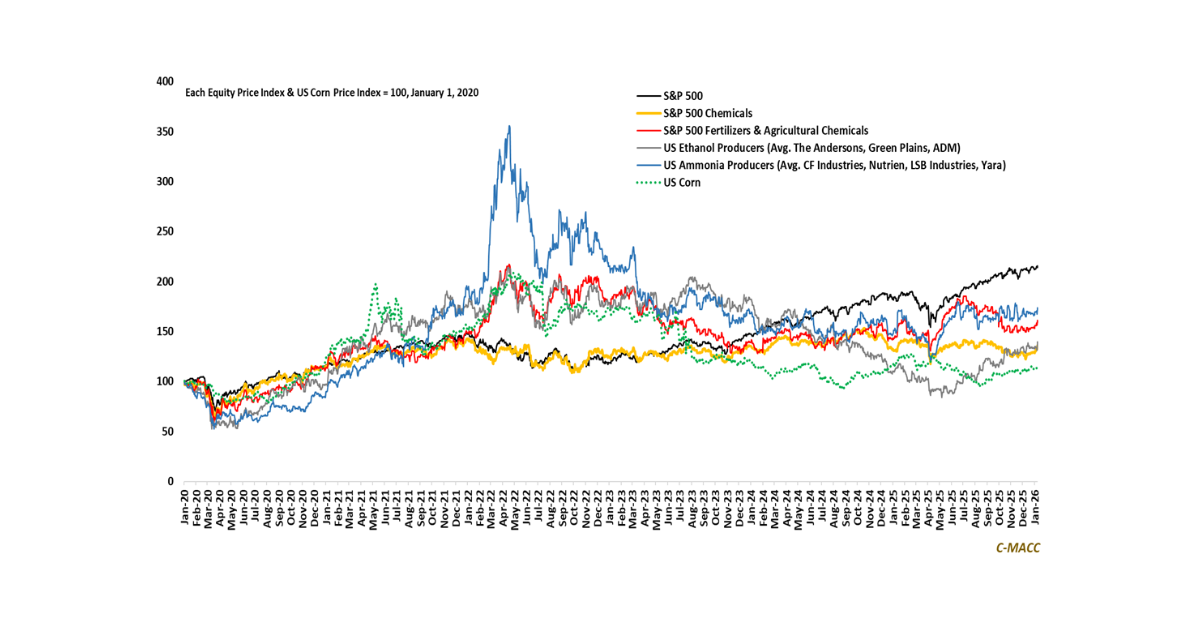

- Other Sector Developments: The surface stability surrounding the global PVC market in mid-4Q25 masks deeper stress as tighter energy spreads, trade barriers, and shifting supply chains expose the industry’s fragile regional interdependence.

Exhibit 1 – Chart of the Day: Regional avg. PE spot prices fall to multi-year lows; supply cuts needed for price rebound.

Source: Bloomberg, C-MACC Analysis, November 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!