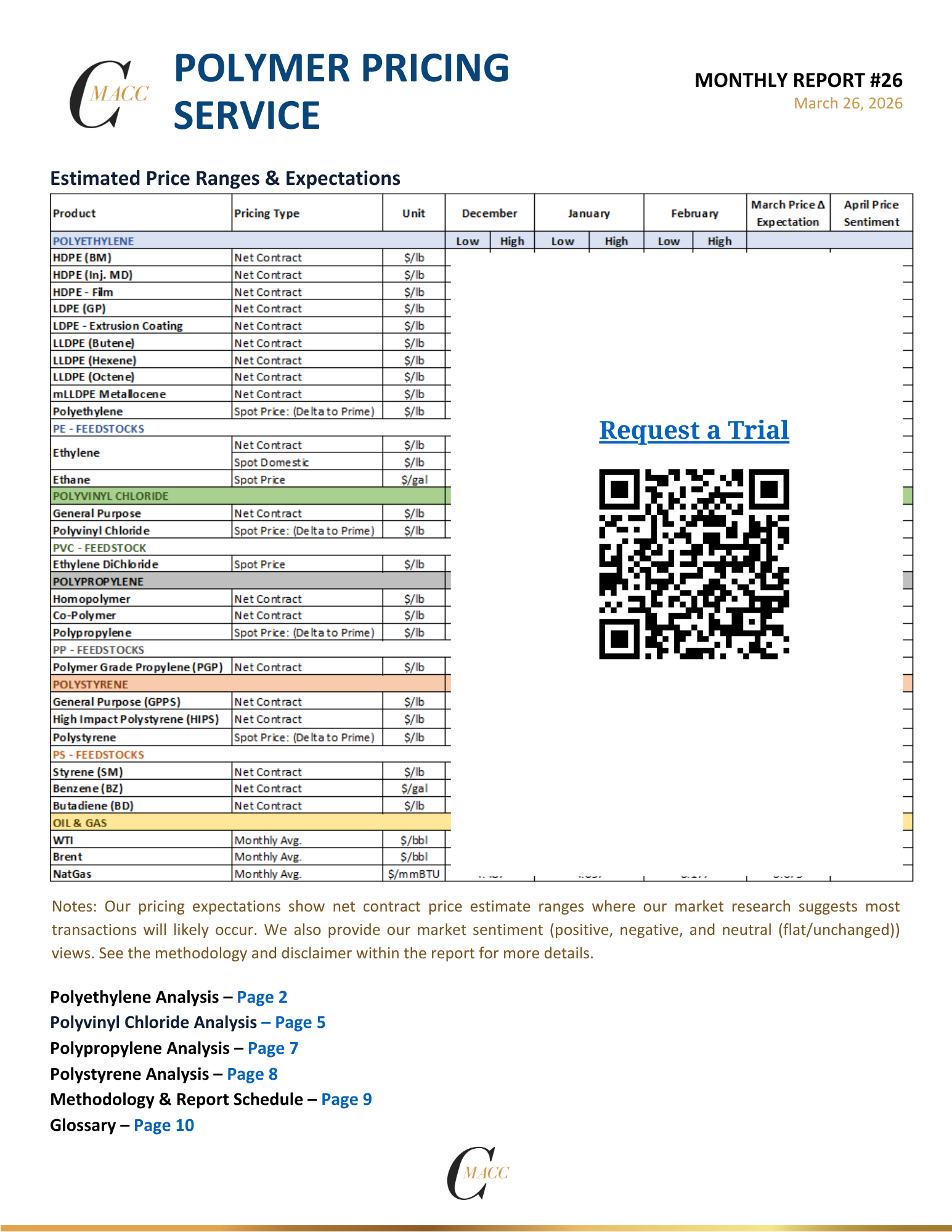

Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

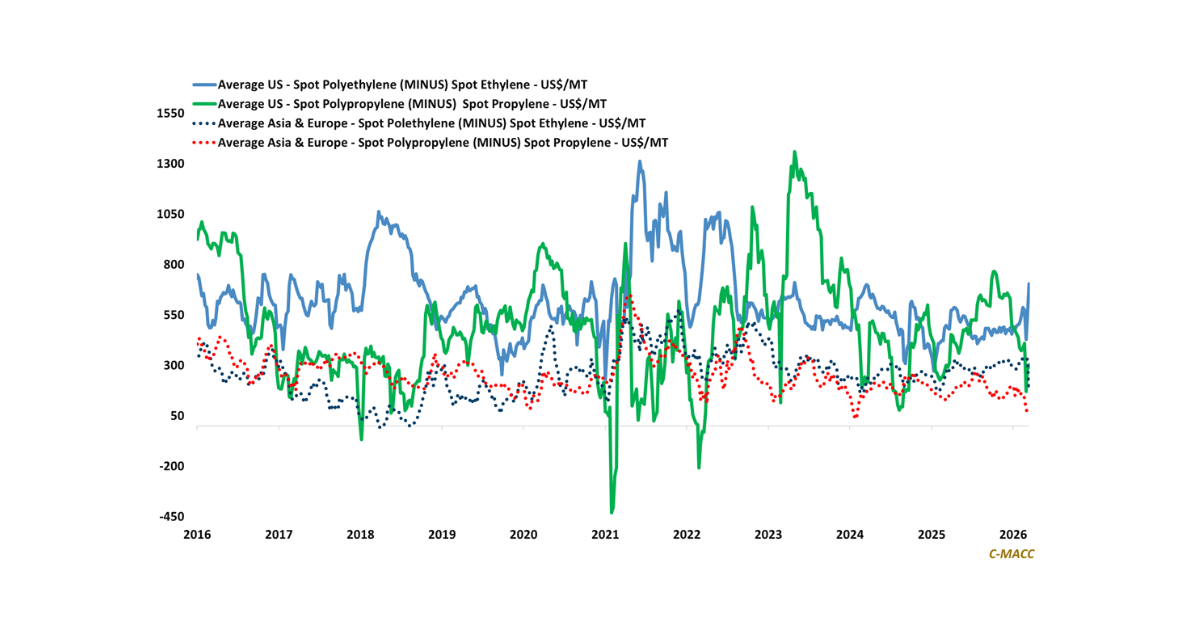

- General Thoughts: Integrated polymer producers retain a durable margin advantage through cost position, system capture, and reliability, as converters and non-integrated producers face tighter spreads and diminishing pricing power.

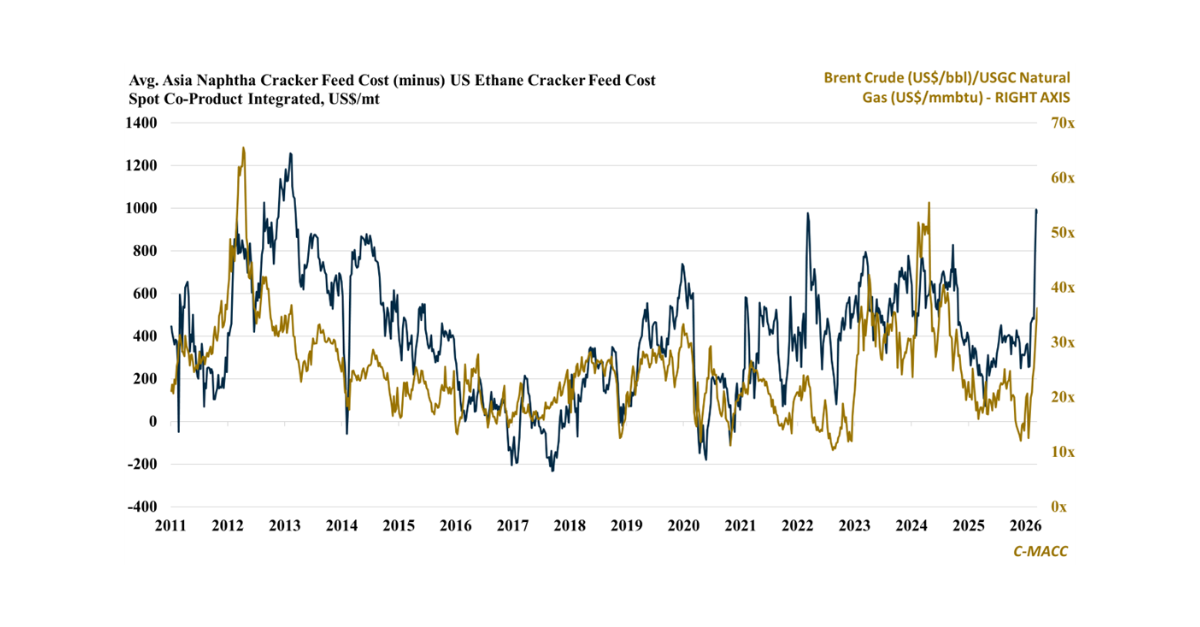

- Polyethylene (PE): Export arbitrage dictates global PE pricing as constrained supply and weak demand shift marginal price discovery offshore, lifting US netbacks, tightening domestic availability, and entrenching export-driven pricing.

- Polypropylene (PP): Propylene tightness keeps PP-to-PGP spreads compressed globally as outages and upstream cuts constrain supply, favoring integrated margins and pushing high-cost capacity toward rationalization.

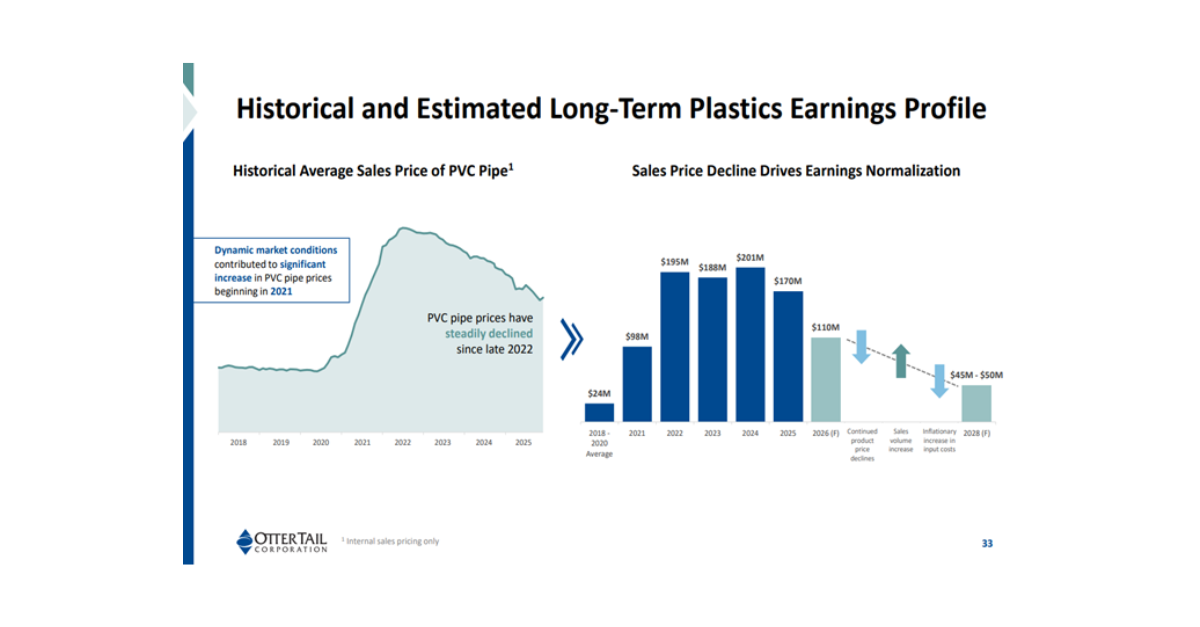

- Polyvinyl Chloride (PVC): Turnarounds and outages tighten global PVC supply as rising costs abroad steepen cost curves, shifting marginal supply toward North America and lifting PVC and EDC export economics.

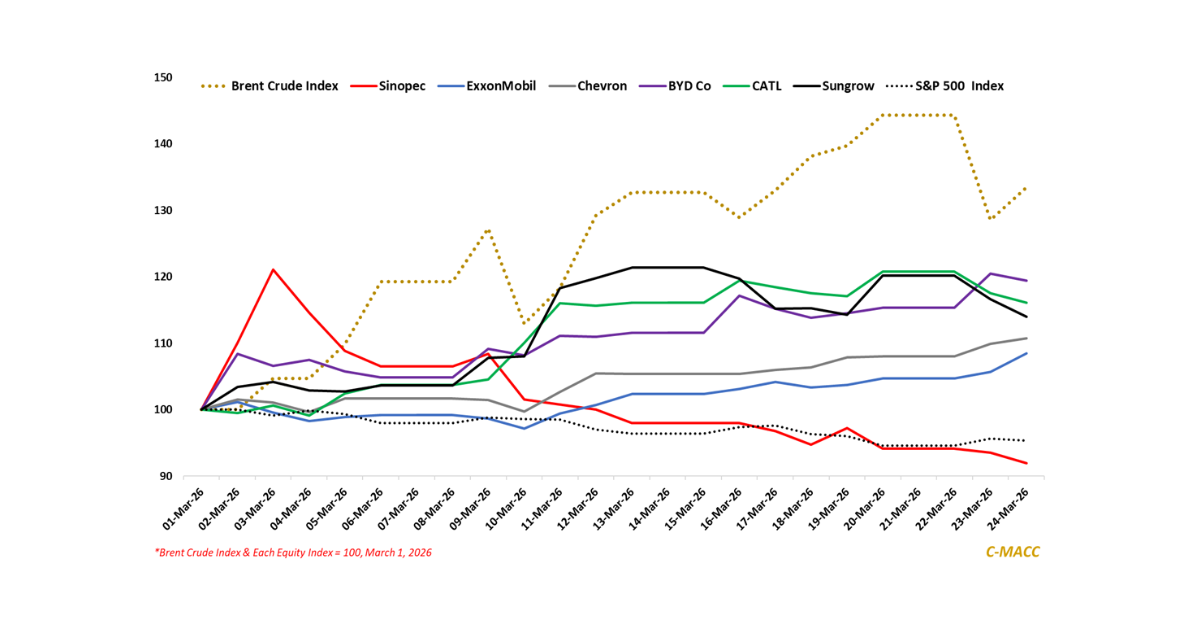

- Other Sector Developments: Oil-linked feedstock inflation is pressuring ex-US petrochemical margins, supporting rate cuts, outages, and delayed restarts across higher-cost regions, most notably Europe and significant parts of Asia.

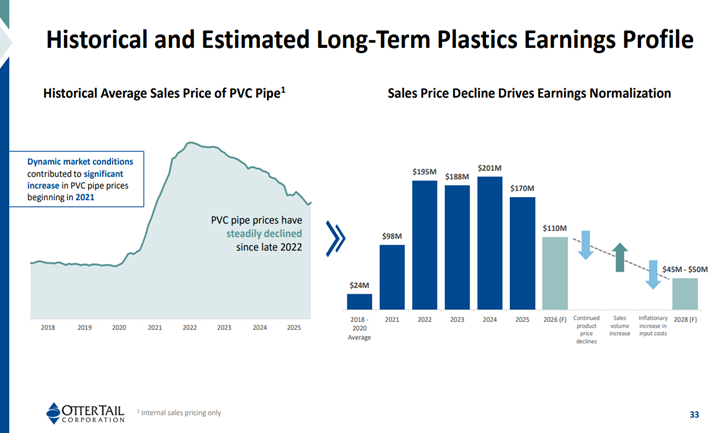

Exhibit 1 – Chart of the Day: Integrated PVC chains gain advantage as resin inflation pressures converter margins.

Source: Otter Tail Corporation – 1Q26 Investor Presentation, March 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!