Base Chemical Global Analysis

Global Weekly Catalyst No. 333

- General Thoughts: Recent global chemical price relief should not be mistaken for normalization; bargaining power is shifting toward bottleneck-controlling assets before weaker buyers regain credible substitutes and pricing leverage.

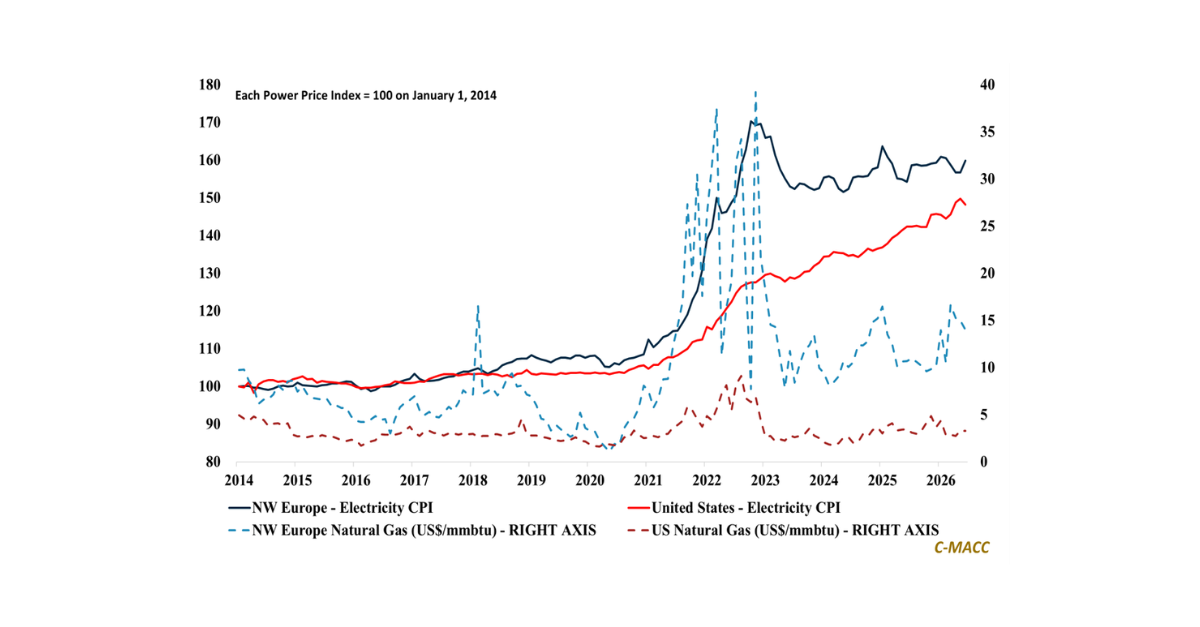

- Feedstocks & Energy: Naphtha spreads are exposing optionality gaps, as Asia pays for supply security and Europe’s relative relief still favors LPG cracking and flexible feedstock systems.

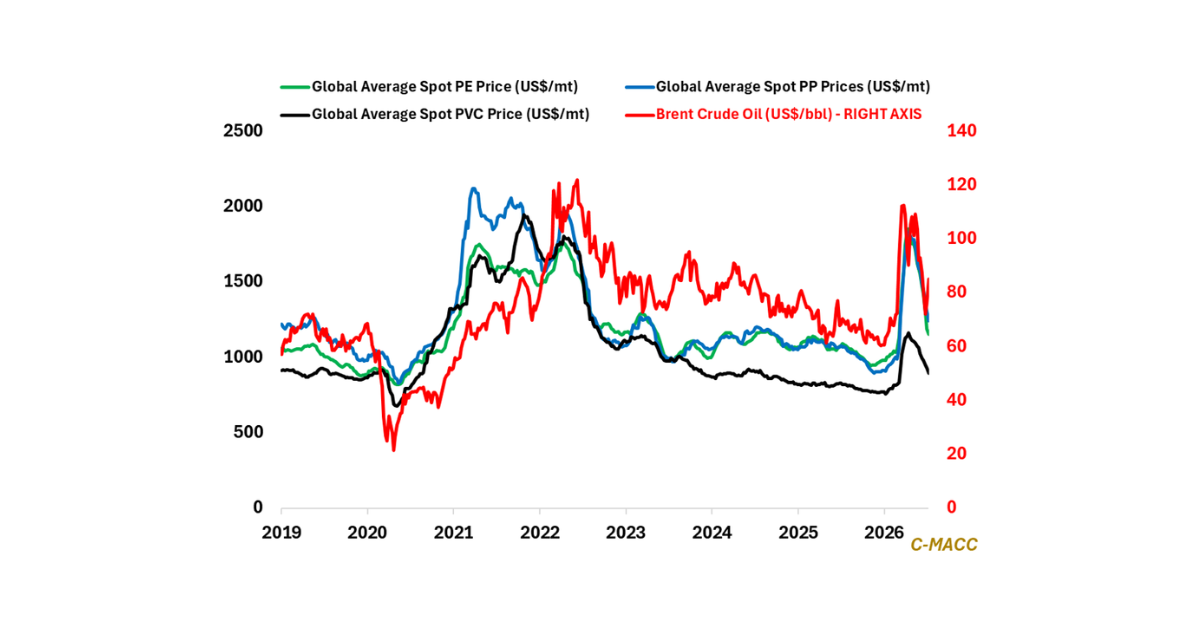

- Olefins: Global olefin spreads reward NGL routing depth over volume signals, favoring US producers as high-cost Asian naphtha systems restructure and Europe’s propylene premium faces fragile demand.

- Other Base Chemicals: Global base chemical corrections are testing pricing durability, as logistics reliability, feedstock linkage, and balance sheet quality outweigh spot relief for merchant buyers in contract negotiations.

- Agriculture: Global nitrogen markets are shifting from shortage stress toward affordability scrutiny, favoring low-cost producers as import-dependent buyers delay, reduce, or reprice demand through 2026 contract planning.

- Refining & Biofuels: Global refining and biofuel margins remain above early-2026 levels, with export reach, distillate strength, and policy-backed demand favoring flexible operators over constrained regional capacity.

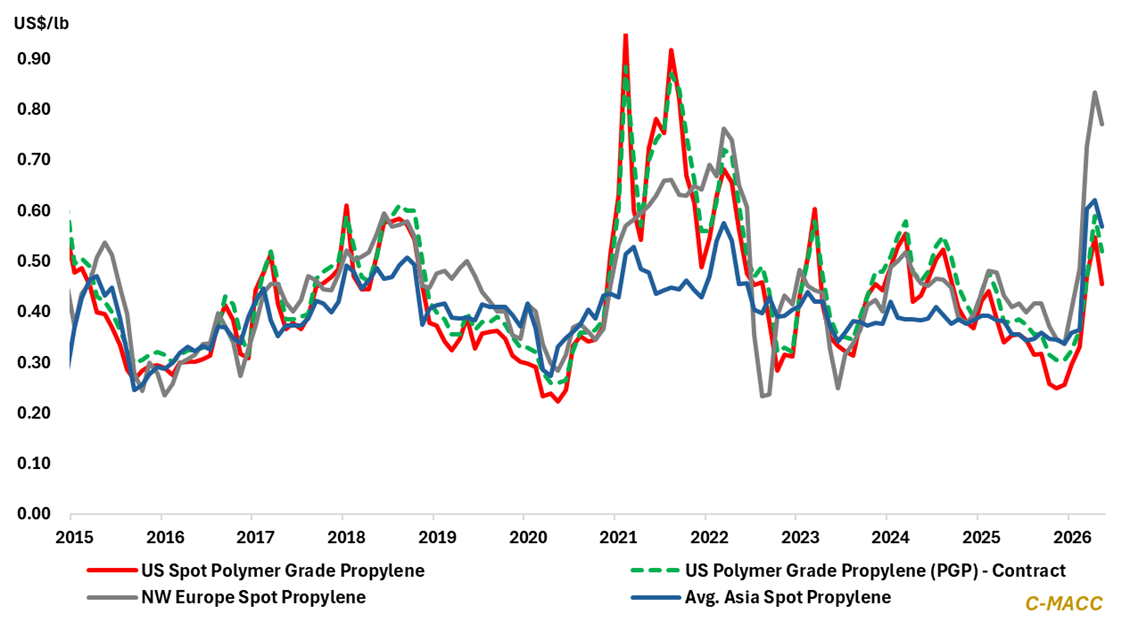

Exhibit 1 – Chart of the Day: Global propylene prices retreat from 2Q26 highs as buyers challenge regional premiums.

Source: C-MACC Estimates, June 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!