Global Market Analysis

Get Up Offa That Thing: Cheap Inputs Don’t Cash Themselves

Key Findings

- General Thoughts: Benchmark advantages become cash only when companies control the conversion point, as delivery, qualification, and customer commitment decide who keeps margin across energy and chemicals.

- Supply Chain/Commodities: Falling input costs do not guarantee relief for adhesive prices, as specialty inputs and supply coverage enable stronger formulators to protect margins despite uneven global demand.

- Energy/Upstream: Customers will pull small modular reactors forward where firm power, siting flexibility, and steam create value beyond low-cost power for sites facing uptime, emissions, and grid constraints.

- Sustainability/Energy Transition: Hydrogen players are extending models to close commercial gaps and lift returns, with select companies moving into power markets where customers pay for complete solutions.

- Downstream/Other Chemicals: Soybeans’ premium pressures switchable corn acres as forward fertilizer buying and financing costs make lower-nitrogen 2027 plans attractive before fall ammonia commitments.

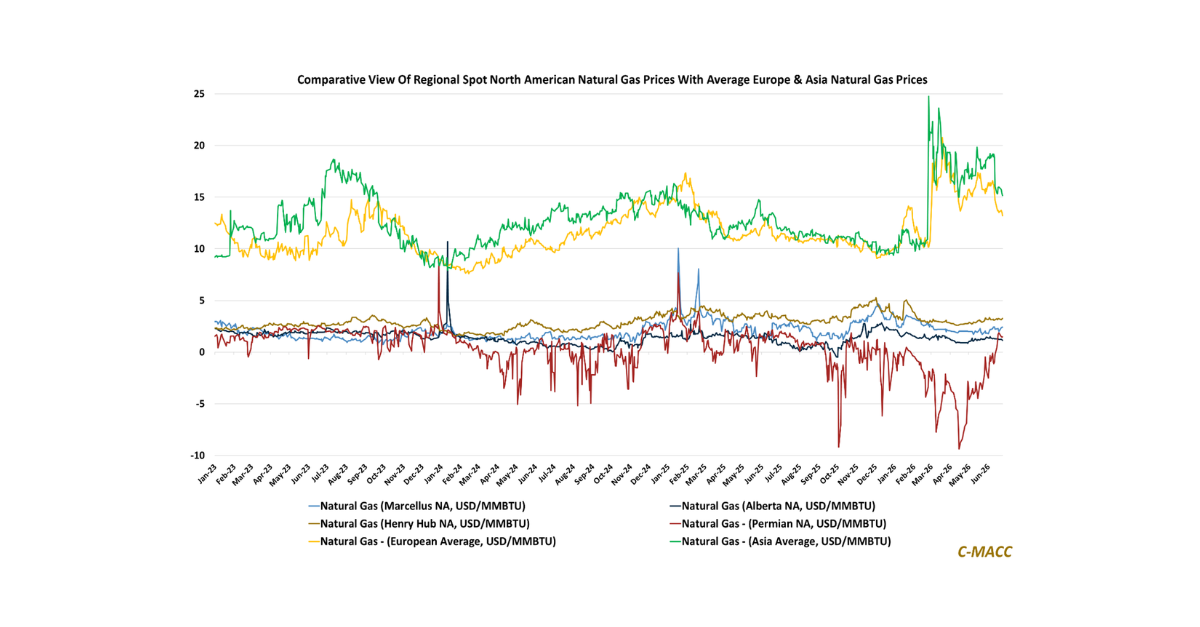

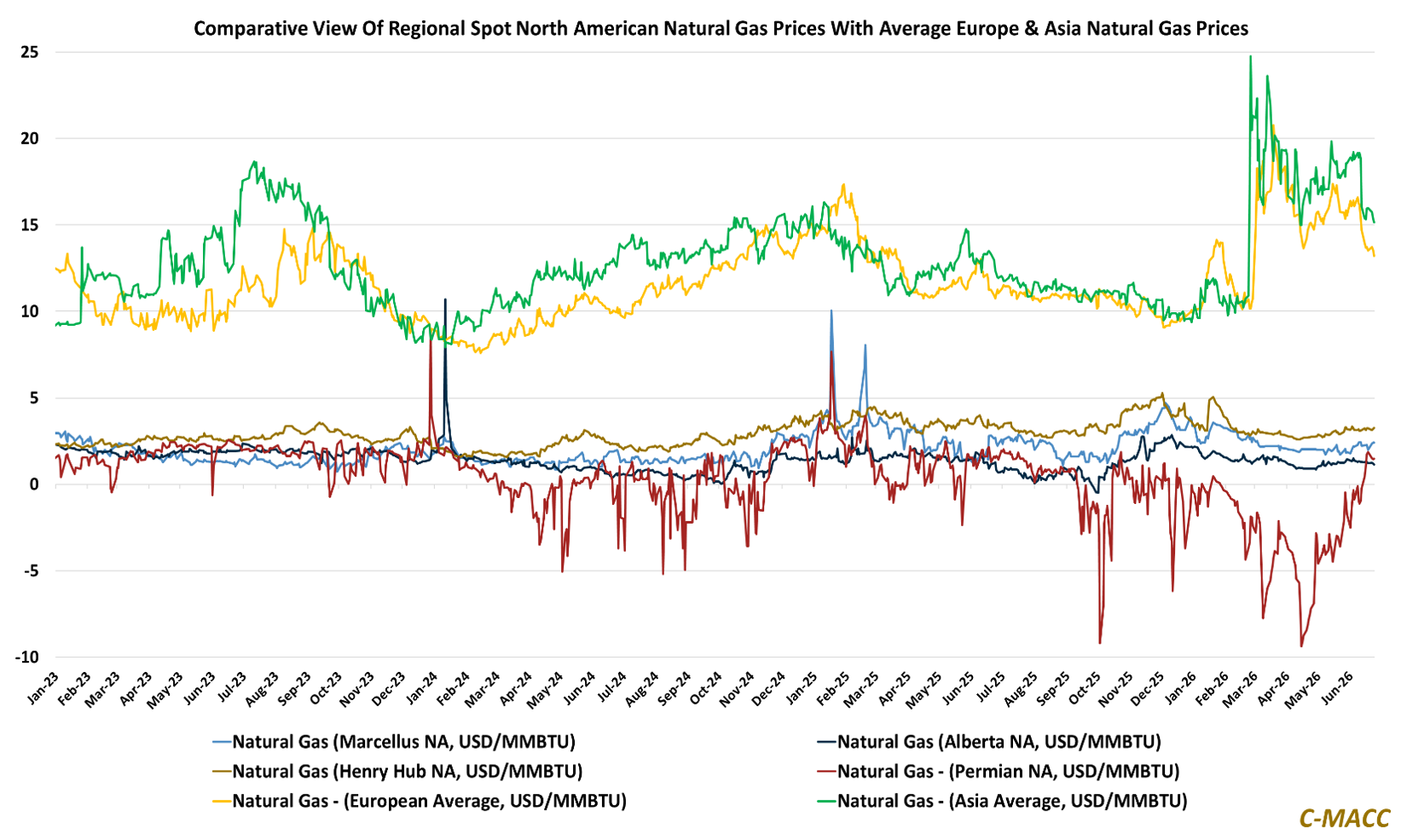

Exhibit 1: Natural Gas Spreads Reveal Who Converts Cheap Supply into Realized Cost Advantage.

Source: Bloomberg, C-MACC Analysis, June 2026

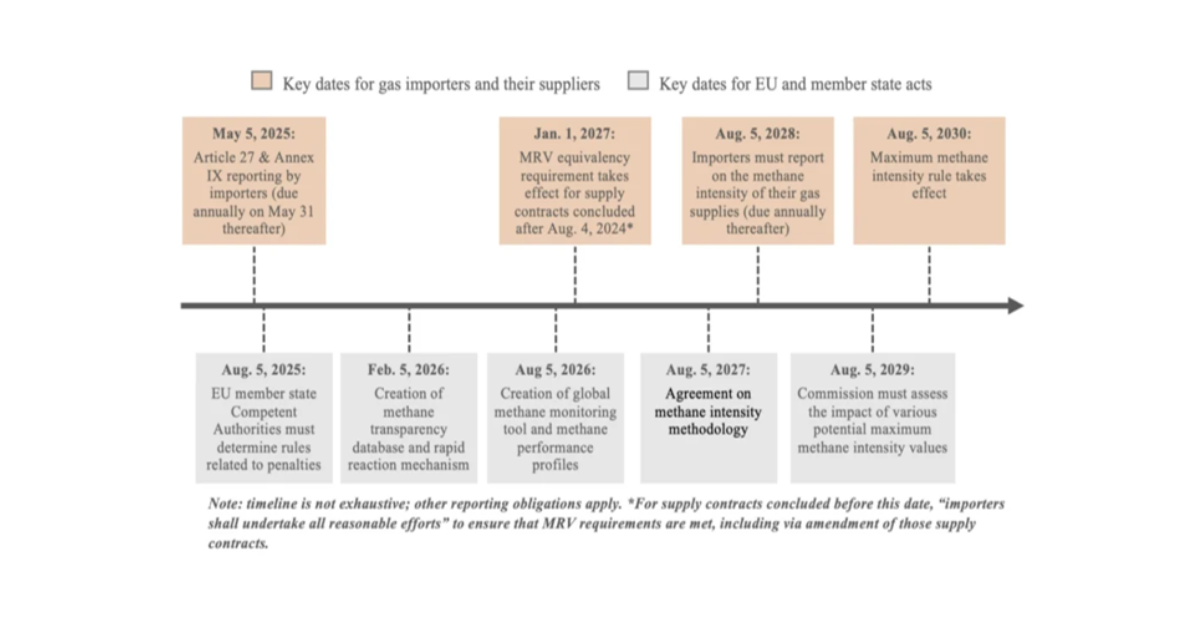

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!