C-MACC Sunday Executive Summary

Holding Patterns: Chemical Producers Delay To Advance, Position For Clearer Skies Ahead

- Capital deployment in the current market setting favors the orchestration of precision over the pursuit of scale, sequenced only when sufficient risk-adjusted returns, timing leverage, and strategic irreversibility converge.

- Geographic participation must now be reverse-engineered from structural return defensibility, where policy insulation, logistics control, and localized value chains supersede the legacy logic of global throughput.

- Innovation is positioning to increasingly become margin infrastructure: deployed not to chase growth, but to embed pricing power, regulatory advantage, and volatility insulation deep into product portfolios.

- A significant theme from 2Q results involves execution sovereignty, the ability to pause, reallocate, and activate assets with surgical intent, as a defining currency of industrial dominance in a world where inertia equals decay.

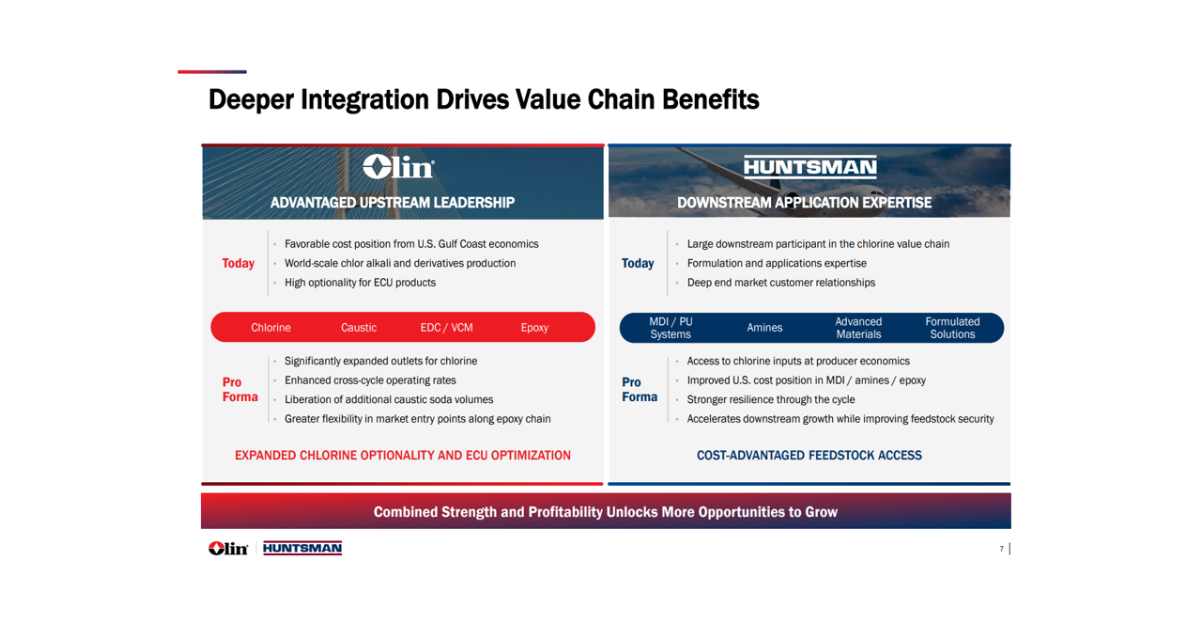

- Otherwise, from Olin’s chlor-vinyl discipline to Methanex’s cost curve leverage, LSB’s UAN advantage, and US midstream recalibration, execution now monetizes volatility, not legacy volume reflexes.

- Companies Mentioned: Dow, LyondellBasell, Eastman, BASF, OMV, Huntsman, Borouge, Olin, Kem One, Wacker, Celanese, Kuraray, Methanex, OCI, CF Industries, Nutrien, LSB Industries, Freeport, Anglo American, Albemarle, Rio Tinto, Enterprise, Phillips 66, Shell, Baker Hughes, Chart Industries, SABIC, Sekisui, Covestro, Arkema, Solvay, XPO, C.H. Robinson, Air Liquide, Air Products, Linde, Trina Green Hydrogen, Envision Energy, BP, Woodside, Fortescue, E.ON, Cleveland-Cliffs, GM, Redwood Materials, Oracle, LG Energy, Repsol

- Products Mentioned: Caustic Soda, Bleach, Ethylene Dichloride (EDC), PVC, Methanol, Ammonia, UAN (Urea Ammonium Nitrate), Natural Gas, LNG, LPG, Ethane, Copper, Lithium, Vanadium, Zinc, Rare Earths, Hydrogen, Polypropylene (PP), Polyethylene (PE), Polyurethanes, Butane, Ethylene, Propylene, Ammonia, Hydrogen, Biofuels, Critical Minerals, Batteries Fertilizers, NGL (Natural Gas Liquids)

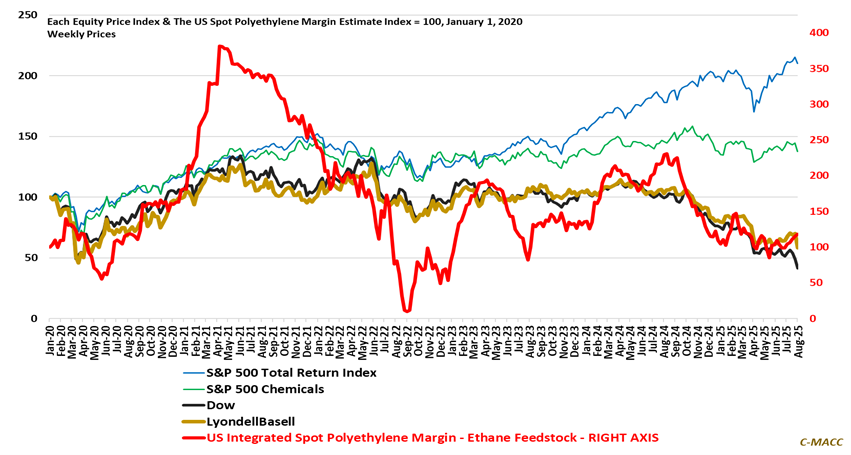

Exhibit 1: US commodity chemical equities have followed profits lower; corporate restructurings favor improvement.

Source: Bloomberg, C-MACC Analysis, August 2025

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!