Base Chemical Global Analysis

Global Weekly Catalyst No. 329

- General Thoughts: Global petrochemical value chains are being forced to adjust through constrained delivery rather than price signals, with inventory buffers delaying repricing and ultimately forcing demand to restore balance.

- Feedstocks & Energy: Feedstock fragmentation is redirecting capital toward gas-advantaged, flexible systems and delivery infrastructure, as naphtha exposure faces rising costs, weaker returns, and constrained reinvestment.

- Olefins: Global olefins markets have fractured across regions and chains, as sustained Asian pressure is exporting an imbalance toward Europe, concentrating pricing power in integrated, low-cost Western systems.

- Other Base Chemicals: Global base chemicals strength is being sustained by inventory depletion and delayed cost transmission, masking tightening supply as integration and logistics control concentrate value upstream.

- Agriculture: Global nitrogen markets are being driven by supply disruptions and policy allocation, with a delayed recovery shifting risk from availability to downstream affordability, especially in agriculture, and demand elasticity.

- Refining & Biofuels: Elevated global refining margins are sustained by supply shortfalls, with strong export demand and inventory draws delaying rebalancing until demand responds and restores equilibrium.

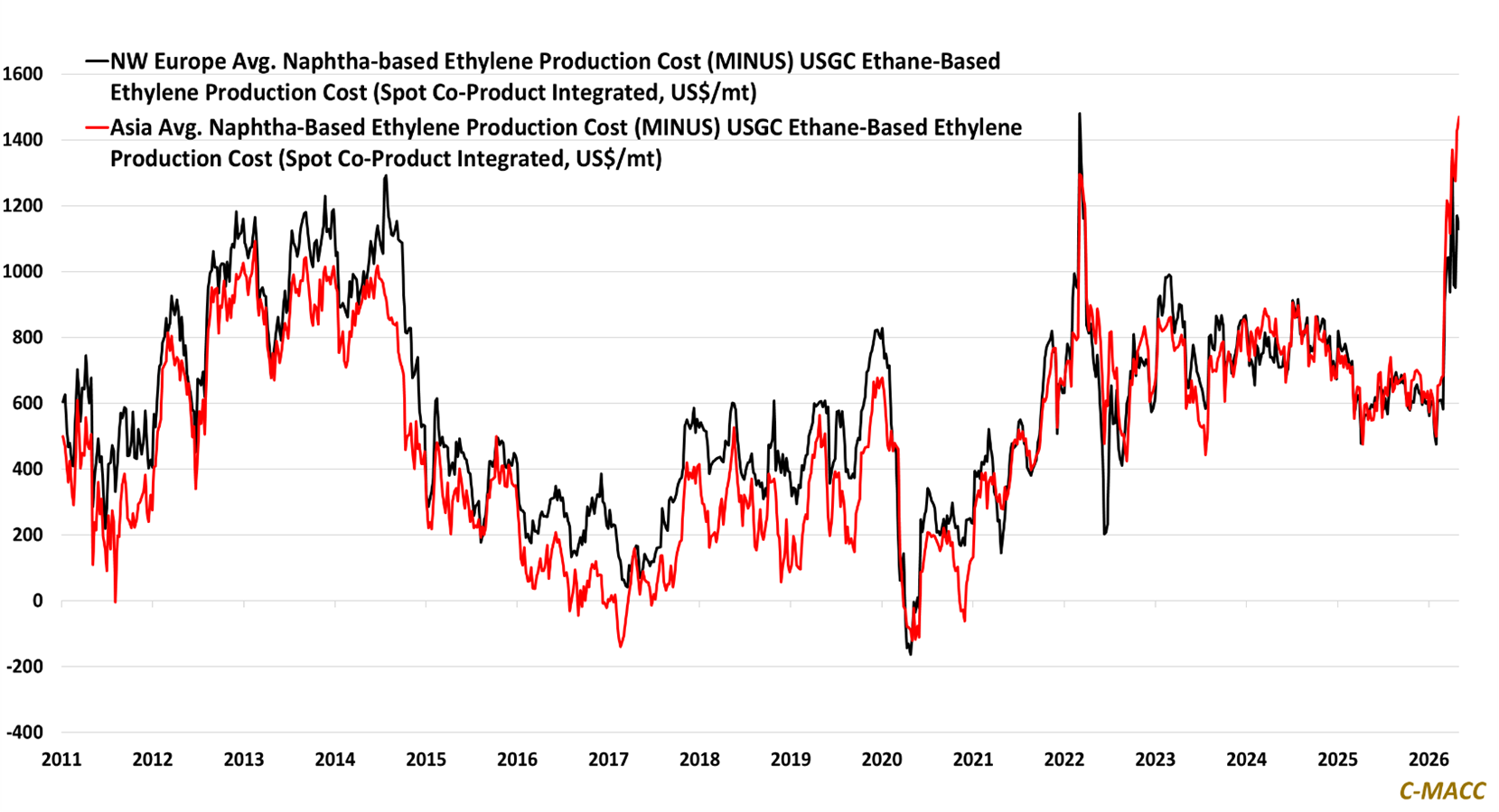

Exhibit 1 – Chart of the Day: Asia average naphtha-based ethylene production costs surge to more than a 15yr high.

Source: C-MACC Estimates, May 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!