Global Market Analysis

Easy Come, Uneasy Go: Cost Relief, Rewards Split

Key Findings

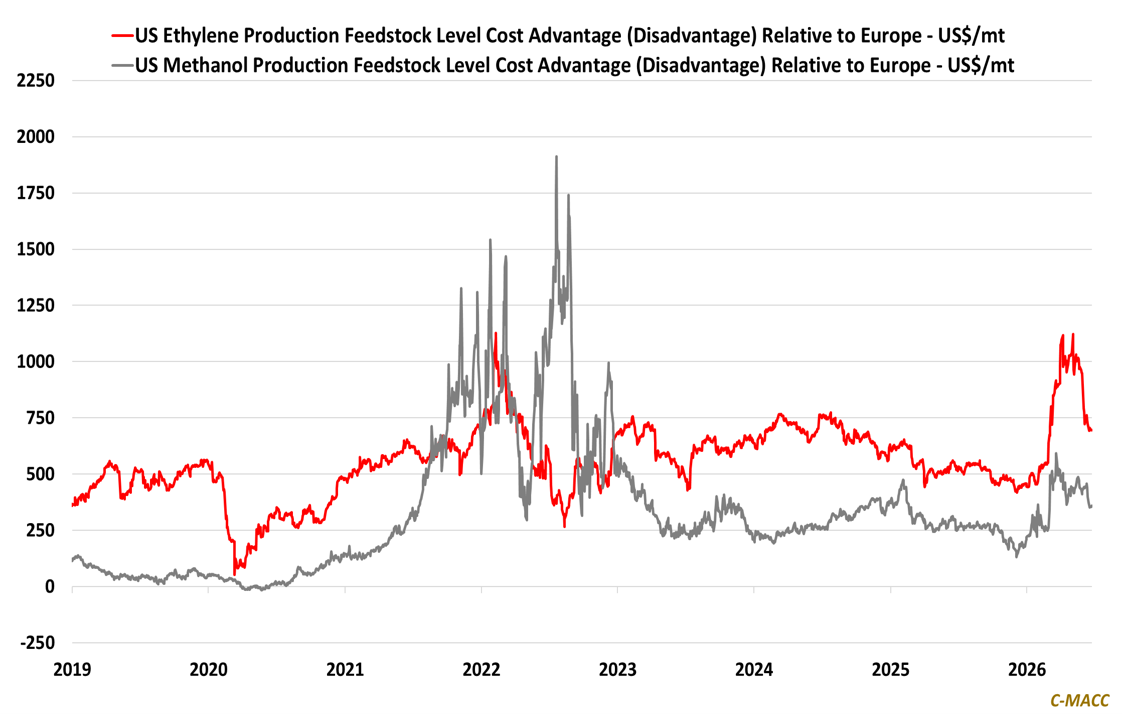

- General Thoughts: The US feedstock advantage has eased from shock peaks, but Europe and Asia ex-China remain exposed, with naphtha and gas costs still limiting derivative recovery and trade flexibility.

- Supply Chain/Commodities: Methanol tightness is sustaining premium value for North American supply in Western markets, as buyers need non-Middle East coverage before new Western plants can justify their cost.

- Energy/Upstream: China is using coal, clean power, and power-market reform to reduce import risk, with ethylene and methanol showing that its domestic efforts will increasingly pressure global chemical margins.

- Sustainability/Energy Transition: Ethanol economics are moving beyond plant margins, favoring operators that pair blending access with RIN capture and credible carbon proof before fuel spreads fade.

- Downstream/Other Chemicals: Freight rebounds and dollar strength are widening delivered-cost gaps in dollar-linked and US-exposed trade, pushing buyers to value route reliability over headline discounts.

Exhibit 1: US Chemical Cost Advantage Eases but Europe (And Asia Ex-China) Remain Relatively High Cost.

Source: Bloomberg, C-MACC Analysis, June 2026

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!