C-MACC Sunday Executive Summary

Afterglow: Prices Burned Hot, Cash Takes the Heat

- 1H26 saw margins shift twice: conflict pricing rewarded reliable low-cost sellers in 1Q26, while falling oil-linked inputs gave buyers stronger leverage in 2Q value-chain negotiations globally against old surcharges.

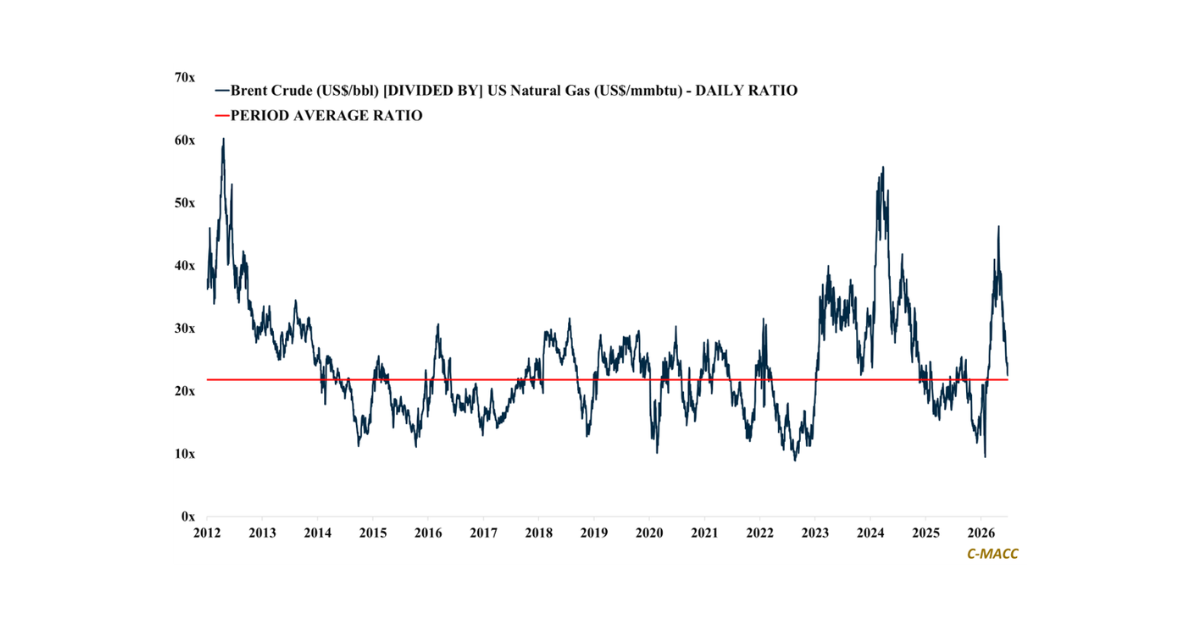

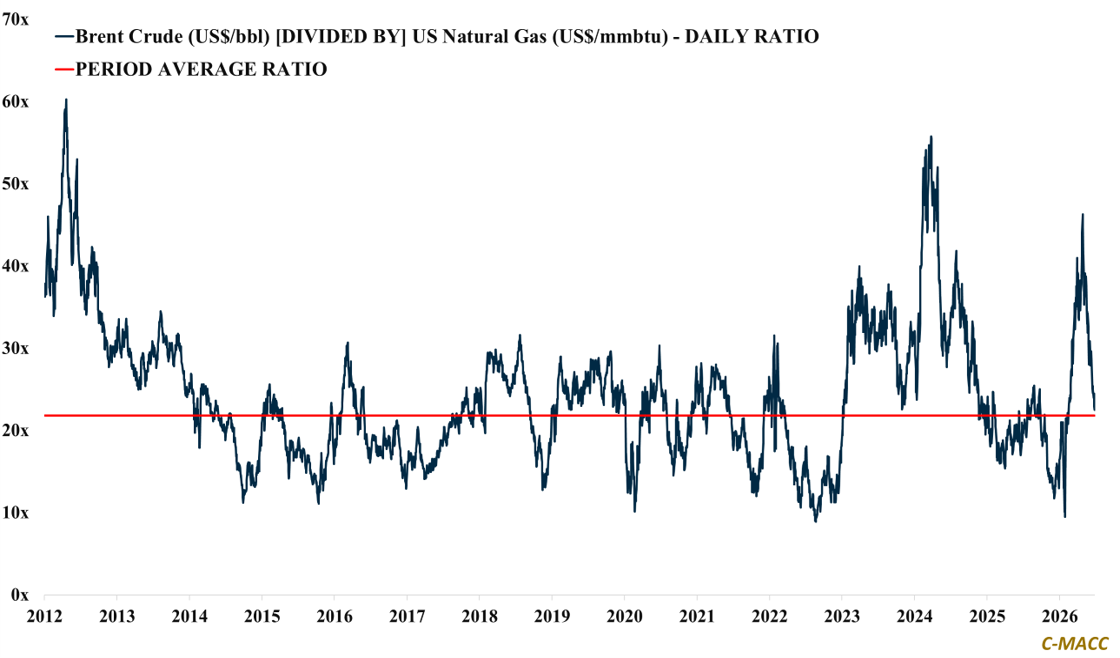

- The recent oil-to-gas ratio collapse redirects global feedstock relief toward non-integrated buyers, but US natural gas/NGL-based producers still retain a cost edge as overseas inputs fall from shock levels into 2H26.

- Evonik, Brenntag, and H.B. Fuller have given stronger-than-expected 2Q updates that reflect supply cover, pre-buying, and price action before repeat demand proves durable through normal reorder patterns.

- 2H26 should test cash discipline, as customers will challenge legacy surcharges while producers manage inventory bought under different cost assumptions amid weaker global forward pricing signals.

- Additionally, we discuss methanol premiums, China’s fuel-cost strategy, methane-proof LNG, delivered-cost gaps, and soybean-led ammonia risk as tests of pricing power after the 1H26 margin handoff.

- Companies Mentioned: Evonik Industries, Brenntag, H.B. Fuller, Celanese, Methanex, Energy Transfer, Dow, X-Energy, NuScale Power, Corteva

- Products Mentioned: Natural Gas, Ethylene, Propylene, Benzene, Polypropylene (PP), Phenol, Nylon, Polyethylene (PE), Monoethylene Glycol (MEG), Methanol, Polyvinyl Chloride (PVC), Naphtha, LPG, Crude Oil, Coal, Ammonia, Soybeans, Corn, Nitrogen, Ethanol

Exhibit 1: Oil-to-Gas Ratio Collapse Shifts Global Feedstock Relief Toward Non-Integrated Buyers After Shock.

Source: C-MACC Analysis, June 2026

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!