Base Chemical Global Analysis

Global Weekly Catalyst No. 337

- General Thoughts: Market indicators near early-year levels do not mean risks have reset; lower ex-US production costs and working capital positions test routes, timing, and customer urgency as supply returns against weak demand.

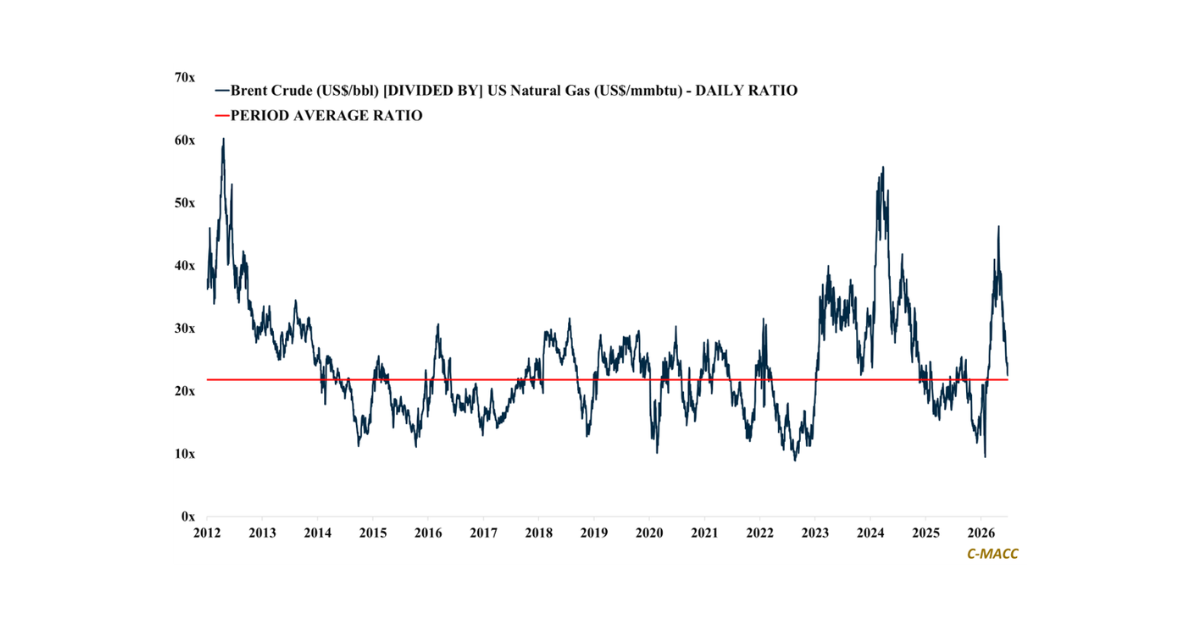

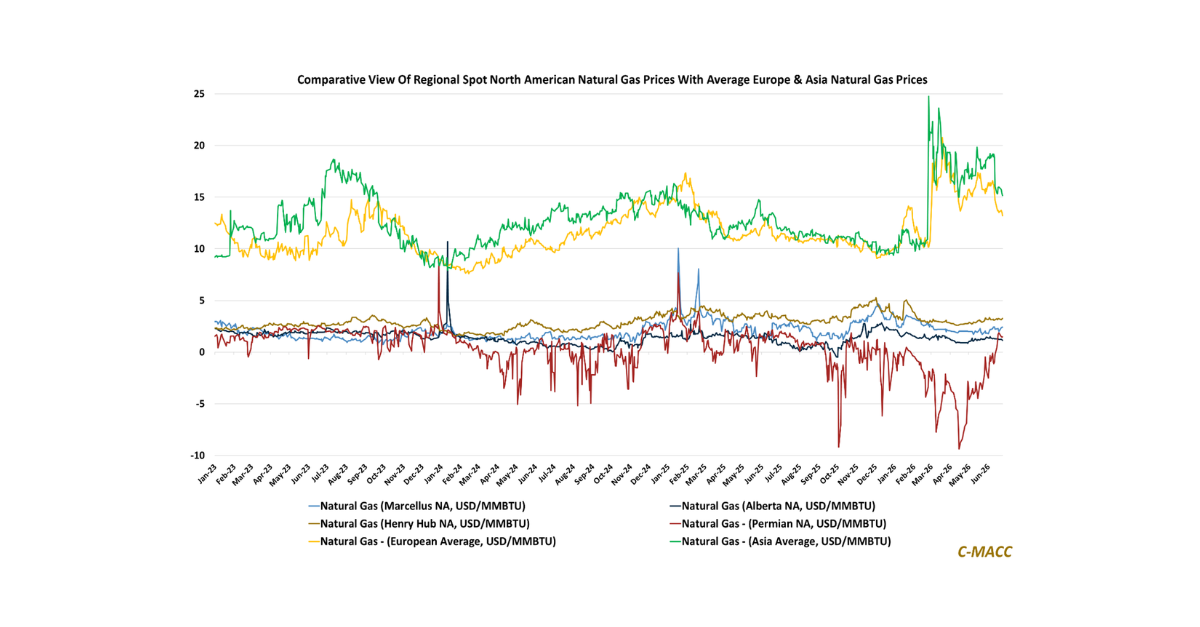

- Feedstocks & Energy: Oil-linked feedstock relief and ex-US natural gas declines have flattened global chemical cost curves, shrunk the US cost advantage, and shifted leverage to buyers as producers consider higher runs.

- Olefins: Lower cracker costs may spur output restarts, but China and US supply should keep olefin derivative chains oversupplied, especially in Asia ex-China, leaving high-cost producers under margin pressure in 2H26.

- Other Base Chemicals: Benzene and methanol are losing risk premium faster than global demand is returning, while chlor-alkali looks better protected only where contracts, freight access, and customer urgency support terms.

- Agriculture: Urea and inland US ammonia prices are easing, but lower overseas natural gas prices and shifts in planted acreage could pressure demand, import prices, and high-cost producers globally through next season.

- Refining & Biofuels: Crude cost relief lifted refinery margins last week as product prices held firm, but high runs and China exports limit upside; ethanol margins rely on cheaper corn, with E15 adding policy optionality.

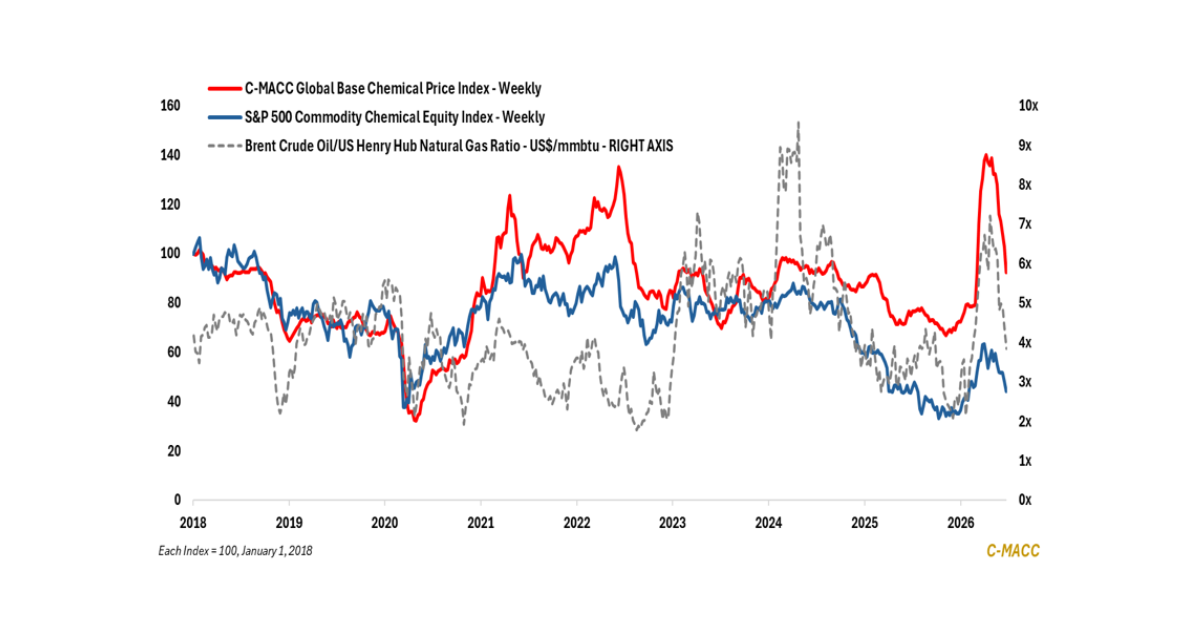

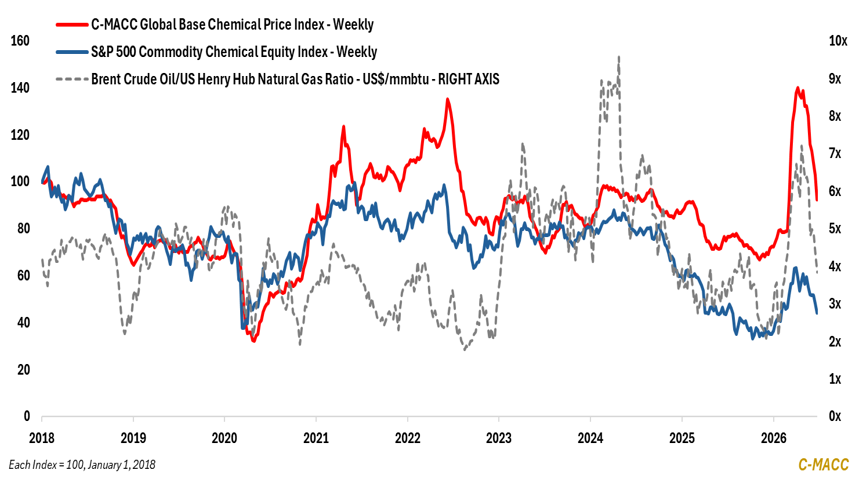

Exhibit 1 – Chart of the Day: Prices, Equities, and Oil-to-Gas Ratios Retreat, but Market Risk Still Lingers.

Source: C-MACC Estimates, June 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!