Excerpt from Sunday Recap 186 & Sustainability Report 146

Feedback from Pack Expo and CMA’s WCF: So Many Moving Parts – Some Moving The Wrong Way and Some Not Moving Fast Enough

It was a busy week for C-MACC, culminating in a very successful client/friend of the firm dinner on Thursday of last week. We wanted more time to reflect on what we observed and what we also took away from many meetings at two very good conferences.

First, we share a couple of pictures from the Hydrogen Panel we presented at the World Chemical Forum:

In plenty of prior research, we have focused on the coincident challenges that the chemical industry faces with an expensive need to decarbonize at the same time that cash flows are collapsing, and the message was rammed home clearly at the CMA conference, while the feedback from Pack Expo was that all are interested in a more sustainable solution, but not at any cost. Many of the sustainability sessions talked about “something” needing to change to speed up the pace of change, but few were explicit with the only solution, which is that someone has to pay a lot more if we want to see progress quickly, and even then “loads of money” cannot fix some of the physical development constraints. Any polyolefin producer outside of the US, and many within the US will be left thinking that they may have no means to pay for anything.

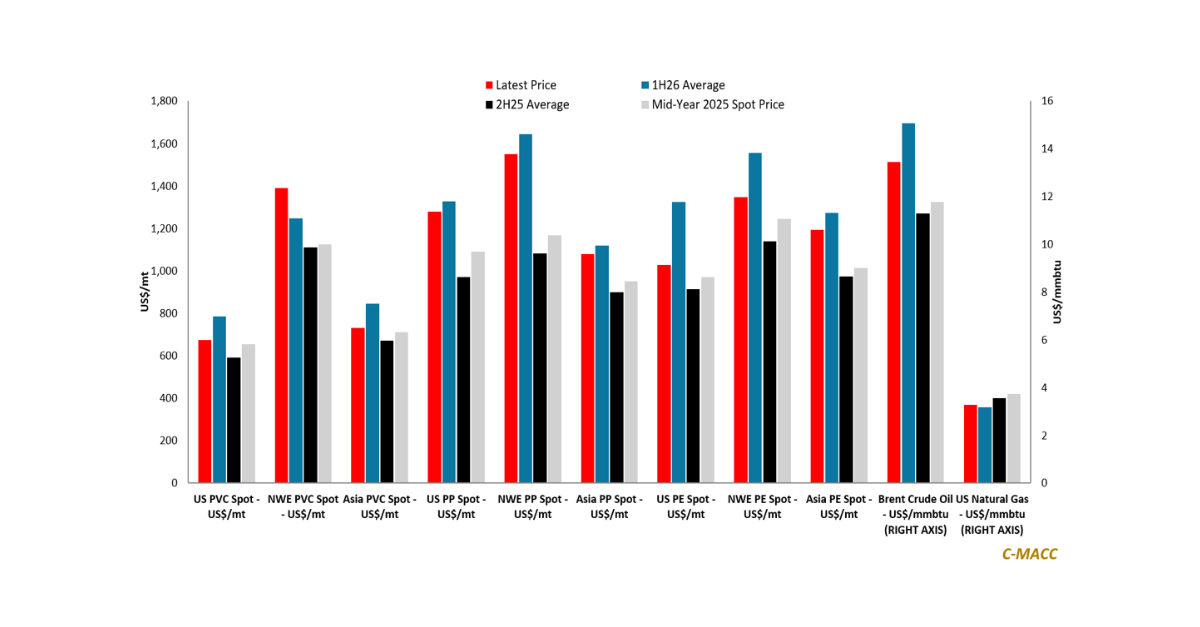

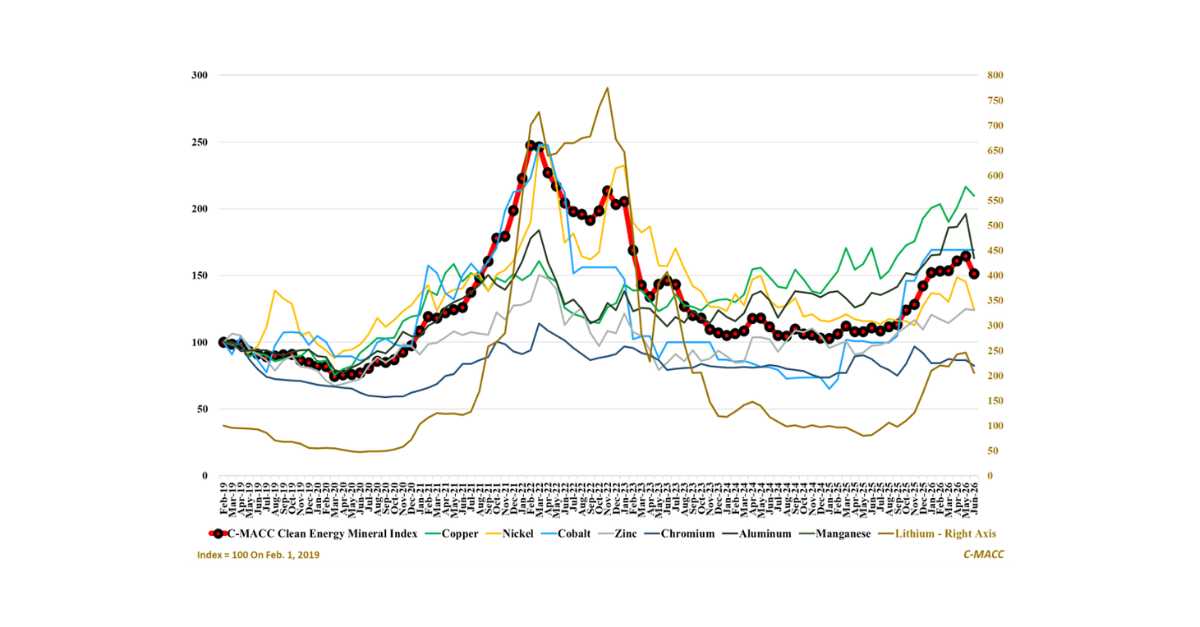

Exhibit 1: The very negative trend since mid-2021 is clear – the US is all about cost

Source: Bloomberg, C-MACC Analysis, September 2023

In the immediate term, those who would prefer to be short-sighted are looking at signs of hope, like some rising prices (all driven by higher oil costs), and one better data point from China. If those were the key messages you took home last week, it is probably time to look for another job. There is no escaping the seismic change that is taking place in China, and the trends will remain negative, even if we get some volatility in the data. Those who listened to the olefins and polyolefins presentations on Thursday at the CMA conference likely left the session depressed and needing a drink. We were grateful that we were able to help with that for a group of our clients on Thursday night, although the glasses of wine did not seem to change the conclusions – only the mood. We are in a period of unprecedented oversupply for polyolefins globally, and we concur with CMA that there is no quick fix. CMA has lowered its polymer demand elasticity ratio with GDP growth for China, which drives only some of the oversupply math. We think this is the right move, but we believe the base GDP forecast behind that calculation may still be too high, especially given the demographic changes in the country. While we may get a couple of years of 3-5% growth in China, it is hard to make a longer-term case. To make the markets better again, we need either a lot of time without new additions (not guaranteed) or an unprecedented number of plant closures – as much as 16 million tons of ethylene and polyethylene capacity in CMA’s view – more if our more bearish view of China’s GDP is correct. Some energy transition opportunities hold hope for China – more on that later in the report.

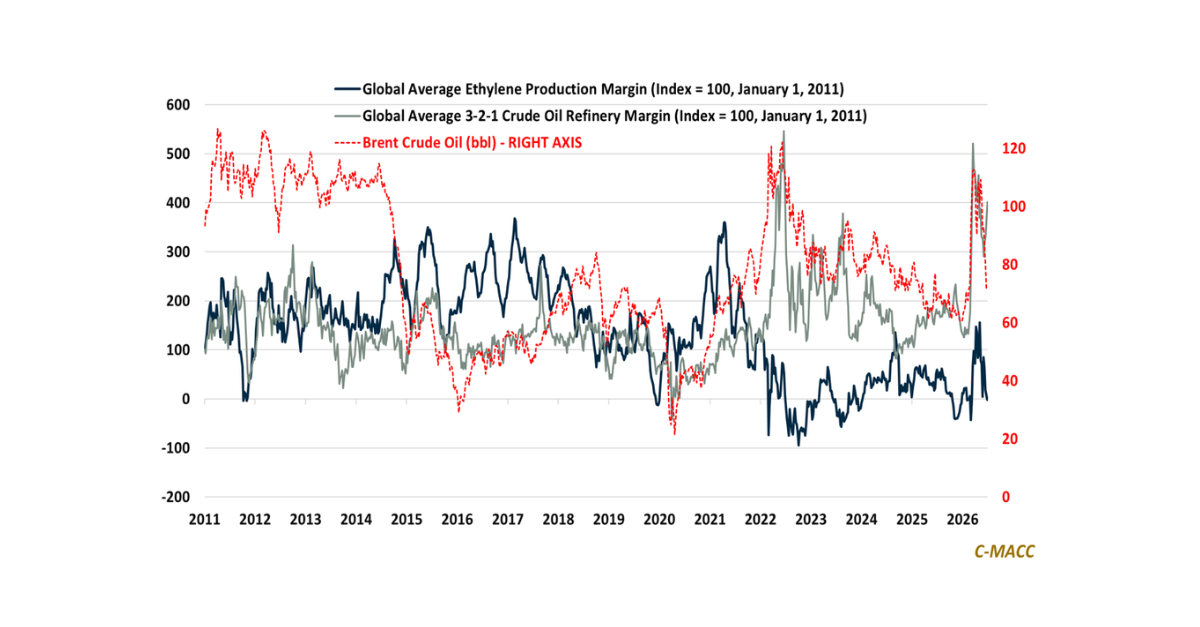

Below we have borrowed a couple of charts from CMA. And the third chart is our own ethylene model – which has more history. The most interesting takeaway from the first two charts is that we know from bitter experience that it is not good for business if you are a consultant and you are negative – you discourage clients from doing anything – including buying your work. Yet here we are – the data is so hard to avoid that you have no choice. The more significant concern we have – if you look at the third chart – is that we could be looking at a 5-7-year period of global operating rates that are as bad as anything we have seen in history. This will have serious knock-on effects, and we should expect consolidation, rationalization, and bankruptcies – as we saw in the past. Those with a cost advantage may look at these charts and think that they are OK, especially in the US, but if lower export pricing and some structural resistance to US imports emerge in places like Europe, the US, and Canadian producers could decide to fight amongst themselves and collapse local profitability as well. No one is safe, except perhaps the heavily upstream integrated producers in the Middle East.

Exhibit 2: The CMA view of polyethylene – not pretty!

Source: CMA World Chemical Forum 2023

Exhibit 3: The estimate in the presentation was that more than 35 polypropylene closures the size of the LyondellBasell Brindisi unit would need to close to bring the market back into balance.

Source: CMA World Chemical Forum 2023

Exhibit 4: Complacency would be a mistake regardless of where you think you sit on the cost curve

So, the glass-half-full view here would be one of consolidation and substantial closures. The challenges around consolidation and possible capacity rationalization are many and include the time it will take for companies to realize that they are in trouble for the long term – you would be surprised how much pushback we see to this scenario – when we talk to some clients – suspension of disbelief. After accepting the conclusions, the next move will be to look for a transactional solution – “can I buy or partner with someone to make my position better”. Only after that will we see some of the closures needed, which will be biased to regions at the top end of the cost curve. We tend to agree with the CMA view that we should not expect much in terms of rationalization in China, despite the high costs and the nominal losses. These investments create and maintain jobs in China and high unemployment is already a problem. Separately, there is a self-sufficiency goal in China, and while China may be there on PVC, HDPE, and polypropylene, it is not yet on LLDPE and ethylene. The conference threw up some diversity of views also based on the agenda of specific presenters. Still, for the most part, CMA itself was skirting the near-term issue a little by focusing on 2027 and beyond in some of its presentations. There are a lot of quarterly earnings reports between now and 2027! In the M&A and banking presentations, the point was made that valuations are currently misaligned. We covered this last Sunday, as chemical companies are not trading, for the most part, as if the wheels are coming off. Bottom-of-the-cycle buyers – including private equity – do not see valuations that suggest opportunity. Those public stocks that are in trouble are in sectors where the longer-term viability is questioned.

Separately, but equally important, the traditional cost curve is not the answer this time and the value in the chart below is quite limited. When we first created this analysis in the mid-90s we thought we had invented the best tool in the industry, and while the analysis is helpful, it is only a little helpful in situations like we see today. While the analysis is inherently flawed because there are a lot of assumptions and because we have more reliable data for some regions and facilities versus others – which is always the case – the bigger issue today is that ethylene costs alone will not drive shutdown and rationalization decisions – they never did – except in a handful of cases in the early cycles. The key chart is almost impossible to draw, as for every ethylene facility you need to consider the site downstream integration and other offsite integration and you also need to consider upstream feedstock integration – arguably much more important this time around. An ethylene unit that sits towards the right hand of this chart today, may be consuming captive hydrocarbons and may be integral to a refining operation. Those ethane-based units consuming captive ethane are more secure than the ones that buy on the open market. In a past downturn, one high-cost ethylene facility kept operating because one of the on-site propylene derivatives was making enough money to keep the whole facility afloat. The chart below does not tell you this.

Exhibit 5: Rough current global cost curve for ethylene – this does not mean that all the capacity to the right of the demand line (red) will close.

Source: Decades of C-MACC founder’s experience and modeling

So that is problem number 1. Clearly establishing who will have to make the hard choices over the coming years is not a straightforward exercise and we will see a period where everyone assumes it will be someone else – they cannot all be right. During that period, profitability will be low and will likely get worse. However, faced with this environment, how do you then prioritize the stakeholder requests and demands about decarbonization (Problem Number 2) – no solutions to which are inexpensive? This becomes another factor in the complex decision process around consolidation and capacity rationalization.

Sustainability and the need to decarbonize was the other major theme that ran through the CMA conference, and the desire for sustainably sourced polymers (or low carbon polymers) also ran through the Pack Expo conference. But what was also clear from both venues is that no one is yet willing to pay for it. The last statement is deliberately provocative, and we concede that there are some willing to pay, but there are not enough by a very wide margin. This subject came up in several different forums, but some couched the problems in statements like “risk sharing” and “appropriate incentives”. The real issue is who pays because nothing that is being asked of any company is free and many stakeholders that companies work with are interested in committing capital to something that has no return – so either the government pays and consumers pay the government back in taxes or the consumer pays directly because prices rise. Voluntary schemes like the US tax incentives look interesting but they are very uneven and not mandatory – note how the activity in hydrogen appears to have declined almost coincident with the IRA announcement! It is also important to note that the slowdown also coincides with the acceptance that inflation was not transitory. Also, note in the second chart that the plans for CCS far outweigh what exists and more importantly what is under construction. Here the 45Q incentive is likely enough encouragement in the US and the carbon price in Europe should also be adequate for select projects, but permitting is slowing things down everywhere and while we wait, inflation is chipping away at any expected investment return.

We encourage you to read our full Sunday report for more views from last week. Request a trial of our services below to receive our research reports directly via email free of charge for a month!