C-MACC Hydrogen Economy Weekly No.24

The US 45V Tax Code Will Change The Competitive Landscape

- Weekly Theme: The US Tax Code – Efficiency Will Matter

- News Update

- Projects Update

- Ammonia/Methanol Update

- Power Update

- Next Week: E-Fuels

Key Points

- The adherence to additionality, temporal, and geographic standards, suggested in the recent IRS 45V tax code leak, means higher-priced green hydrogen based on higher-cost power and a slow rollout.

- While the tax code aligns with IRA objectives in a broader sense, it will increase focus on electrolyzer efficiency and push solid oxide technology (Bloom), especially where projects have waste heat.

- Less efficient technologies, Alkaline and PEM, should see demand fall because of higher operating costs, increasing financial problems for its primary equipment producers, and possible bankruptcy.

- Lower cost high capacity-factor power will be critical to get full credits, and the run of river power idea pursued by Issaquena Green Power (IGP) could drive substantial green hydrogen investment along fast-flowing rivers. (Note that C-MACC’s Graham Copley and Cooley May are partial owners of IGP.)

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!

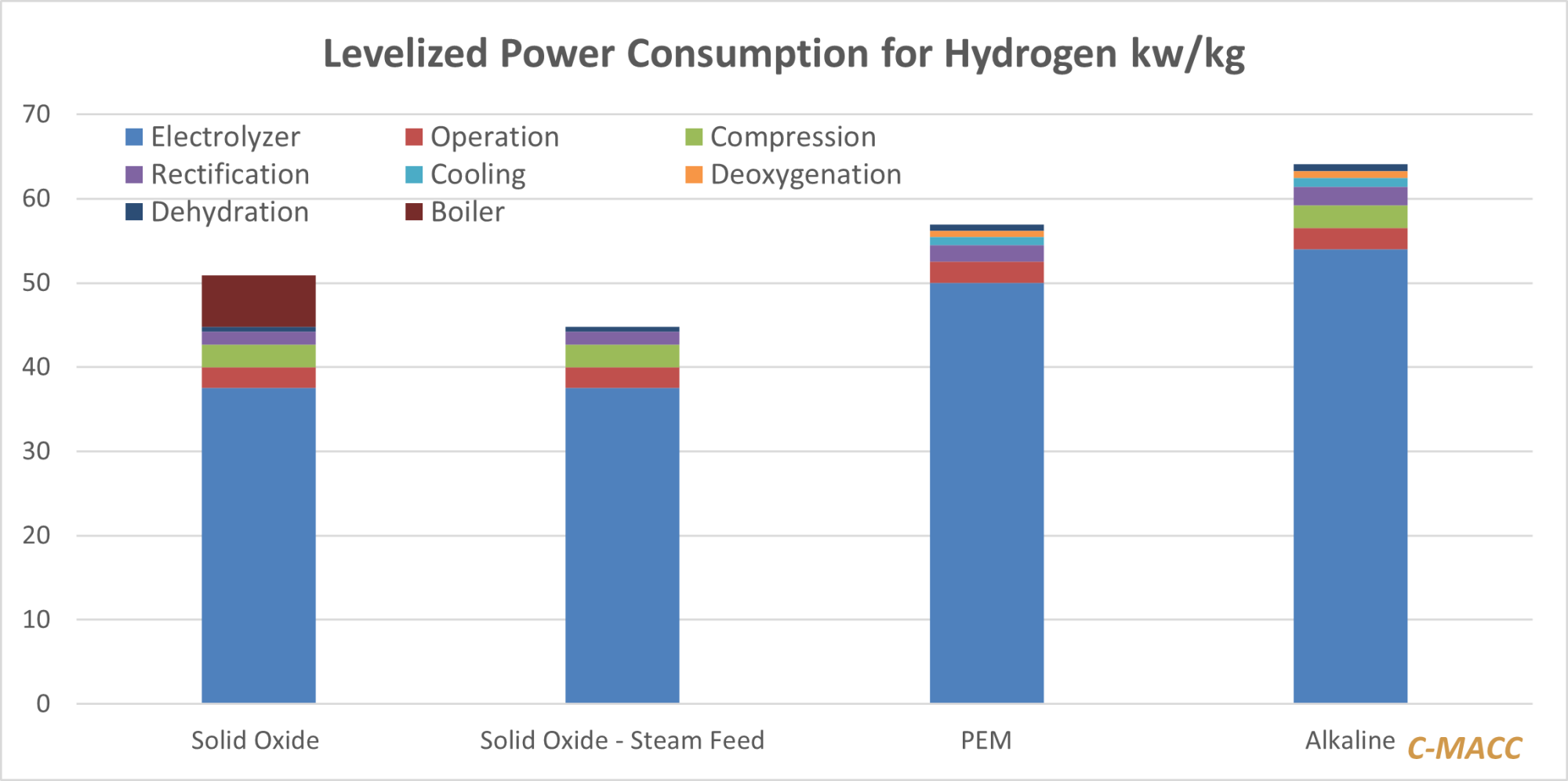

Exhibit 1: These differences are insignificant if power is free – very different if it is not.

Source: Company Reports, Client Discussions, and C-MACC Analysis

Weekly Theme – And The Winners Are… Solid Oxide Electrolyzers and Issaquena Green Power!

Earlier this month, there was a leak of the proposed Treasury Department guidance for claiming hydrogen production tax credits under the Inflation Reduction Act (IRA) (45V) – while the renewable power challenges are significant – on a relative basis, it looks quite good for the most efficient electrolyzers. Requirements to get the full $3 per kg credit are strict. Until there is such an abundance of low-cost renewable power that intermittency is no longer an issue, projects will struggle to get off the ground because the net cost of power will simply be too high. To be clear, all our analysis suggests that full credit is needed to give green hydrogen any chance of being competitive – a partial solution will not get you there. The three proposed conditions – additionality (of power) – temporal correlation (only an issue with intermittent power) – and geographic correlation, essentially mean that you cannot use existing sources of renewable power (which kills nuclear), you need to account accurately for the renewable power you get – i.e., no subsidy when the sun does not shine, and you need local power. We have always said in our work that the development of power hubs is needed, not hydrogen hubs, and this ruling, should it go through, will not only prove that thesis correct but could throw a wrench in some of the hydrogen hub plans already selected for funding.

Not surprisingly, the leaked draft has raised concern amongst green hydrogen project developers everywhere, although the rumor mill had been active for a while. While the impact of the proposed legislation will vary from project to project, and from geography to geography, one outcome, intended or not, is clear. Applying a more restrictive set of criteria (additionality, matching, proximity) to the renewable power supply to secure the relatively lucrative Production Tax Credits, will inevitably result in higher cost power, and therefore at first blush, more expensive green hydrogen. As the chart below shows, you need very cheap power to make this work unless customers are willing to accept higher hydrogen prices. Faced with this challenge, but more severe, in Europe, we are already hearing calls for demand-based subsidies to allow consumers to pay more. So, subsidies on production and on consumption to make the investments acceptable.

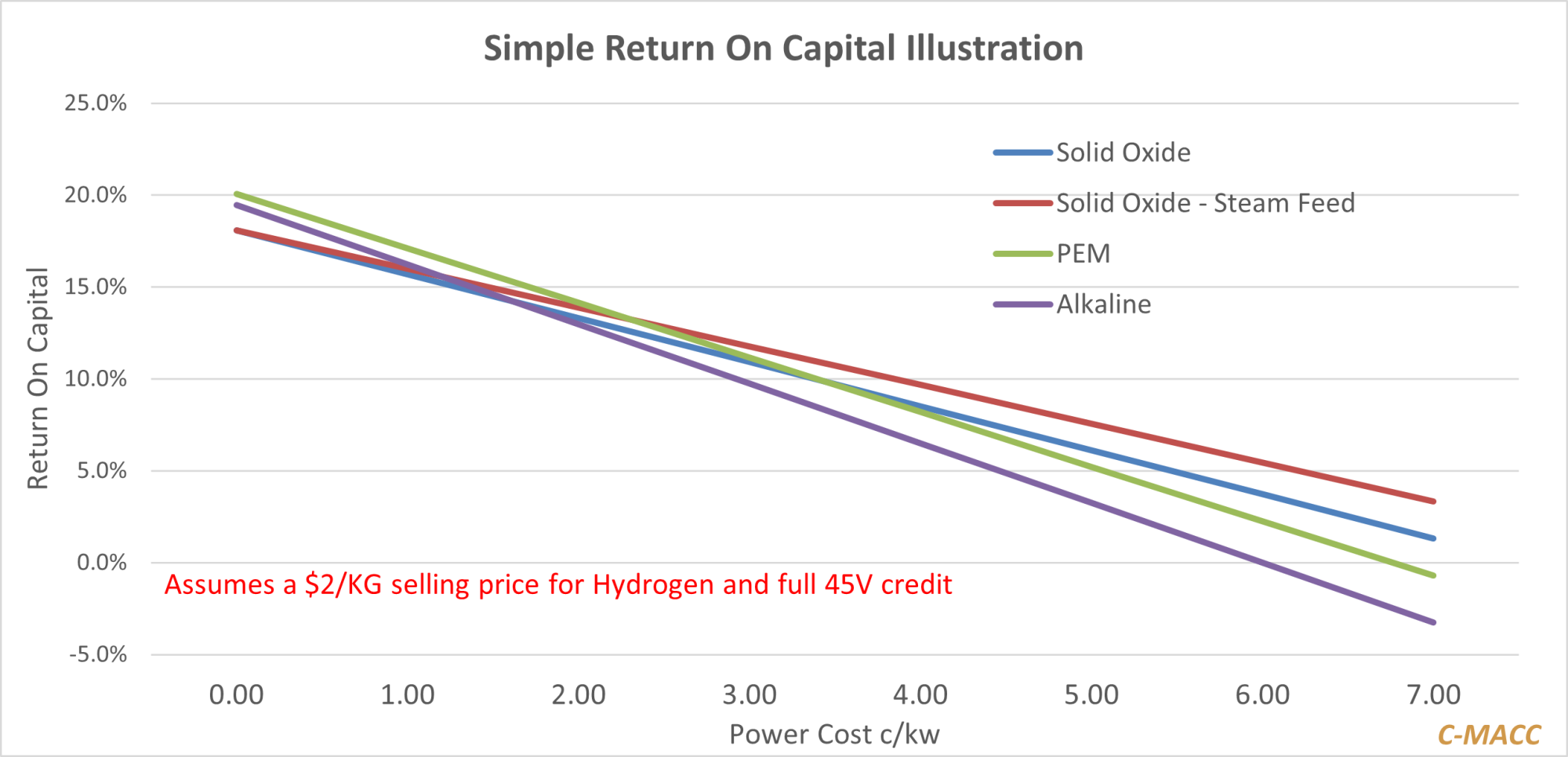

Exhibit 2: Given the higher labor and manufacturing costs in the US, capital costs will only come down with significant scale – there is unlikely to be demand enough to drive that. The more you pay for power, the more attractive solid oxide technology becomes – equivalent to PEM at 1.5 cents per kw of power.

Source: Company Reports, Client Discussions, and C-MACC Analysis

Looking at this through another lens, however, it is likely that this position from the IRS was not an unintended outcome. Such criteria will produce clean hydrogen that does not have the unintended consequence of generating more fossil-fuel-derived power (with incremental carbon footprint), elsewhere in the United States to offset the possibly more lucrative (with PTCs) production of green hydrogen. It is possible to view this approach, especially given the magnitude of potential subsidy by the Treasury Department, as prudent to both the US taxpayer and lower net carbon emissions, which is the intended result of the IRA. It does not help many of the projects on the books, including some of the hydrogen hubs, but it stays true to the bill’s goals.

A separate consideration is that properly costing the dedicated renewables required under the ‘leaked’ language, results in the renewable power most likely being at a higher cost to each clean hydrogen project. This brings us back to the work in our initial hydrogen report and Exhibit 1, which is that electrolyzer efficiency will be much more important, and probably more so than capital cost. Existing projects could go back to the drawing board as the impact of higher efficiency (lower operating cost) alternatives versus capital costs in the LCOH (Levelized Cost of Hydrogen) calculation becomes much more important, and the focus should shift to the hydrogen technology with the lowest lifetime cost of production. This is applicable for projects fed with complimentary stacked (e.g., wind and solar) renewables as well as alternatives considering energy storage in the form of batteries – higher cost input electricity, which is the prime driver of the LCOH economics, will always favor the most efficient conversion technology of electrons into molecules in the electrolyzer. Exhibit 1 shows the cost of getting dry, pressurized hydrogen in each case, which is more than just the power needed to split the water atom. The solid oxide with waste heat is as much as 20 kw/kg “cheaper” than alkaline and almost 12 kw/kg “cheaper” than PEM. With power at 6 cents per kw – the best-case solid oxide hydrogen cost is $1.20 per kg lower than alkali and $0.80 per kg cheaper than PEM. See Exhibit 3.

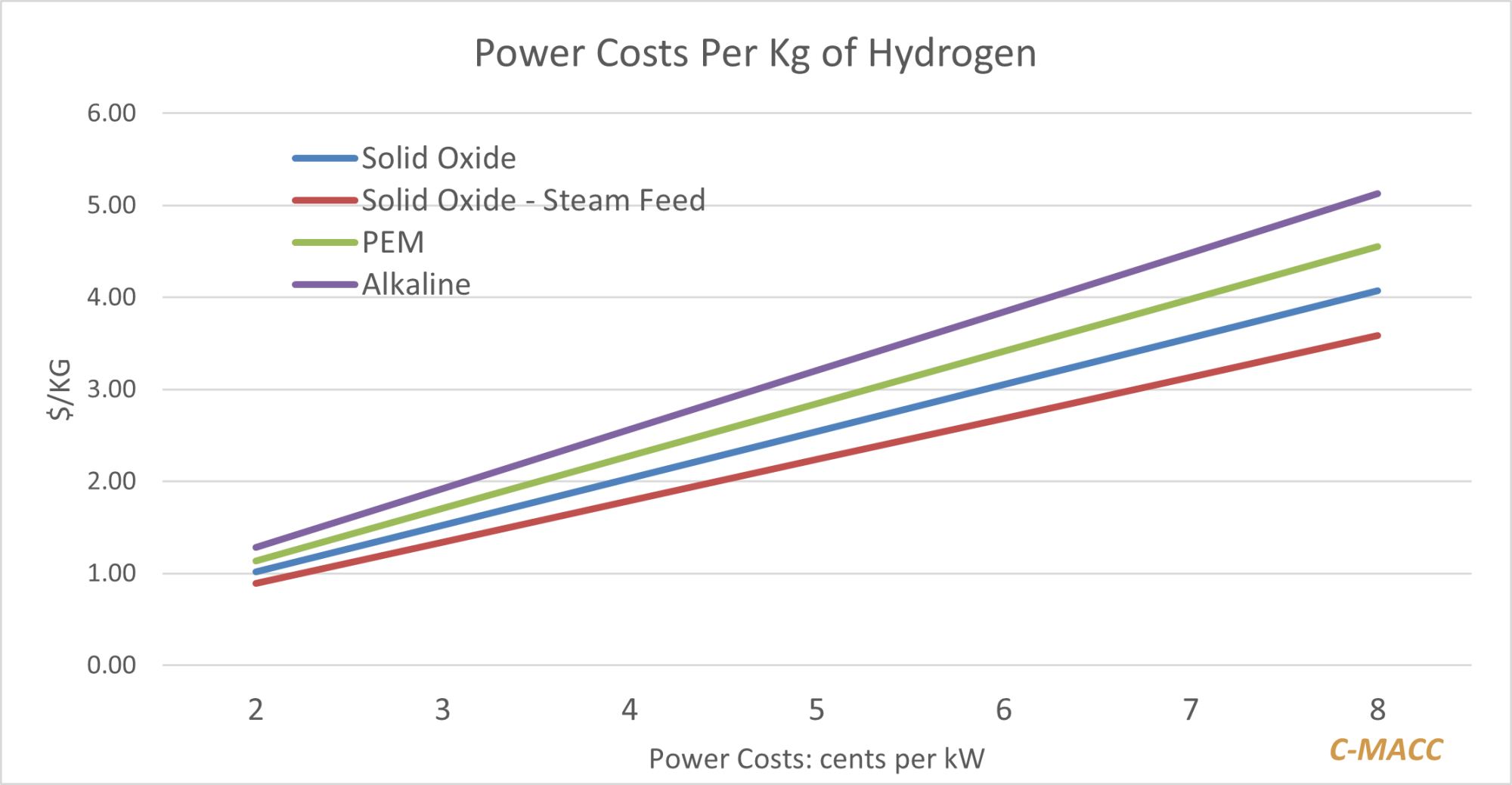

Exhibit 3: Best case solid oxide is breakeven with 45V below 7 cents per kw. For Alkaline it is 4.5 cents.

Source: Company Reports, Client Discussions, and C-MACC Analysis

With the capital cost assumptions we introduced in the summer, you can see that the return on capital of the solid oxide electrolyzers only looks less attractive when you get close to free power – Exhibit 2. Those trying to get demand-based subsidies are likely to bump up a lot of opposition, and even if they are successful, what would be the incentive to offer a subsidy that does not reflect the lowest-cost technology?

Additionally, we have expressed significant concerns regarding China potentially dominating electrolyzer production in the future, as they have taken leading positions in wind and solar power generation. It is possible that what the Departments of Treasury and Energy are proposing, with these more restrictive rules, is that in fairly evaluating renewable power, the endgame could also be to discourage the application of relatively inefficient but lower capital technologies – although we see China on a path to lower costs so significantly that this may not be enough. The economic bias would shift in favor of leading-edge technologies developed and manufactured in the United States to ensure that United States manufacturing, jobs, and technologies are advantaged in the future as projects look to benefit from the subsidies – as the cost of power rises, getting access to some of the locally manufactured production credits may drive more capital efficiency for US projects.

We doubt that the IRS view was leaked unintentionally – with the goal being to get the analysis that we have presented here into the market. Some conclusions:

- The tax code drives even harder some of the conclusions that we have been pushing for years – green hydrogen will be more expensive than people expect.

- The more limited investment that the tax code would create will not allow for economies of scale to develop such that capital costs can come down quickly – the $1 per kg target that the DOE has is out of the window.

- The hydrogen hubs put the cart before the horse as power is the challenge – some of the hubs make less sense and will waste any grant money provided.

- Some equipment makers will not see enough demand and demand growth to keep the debt collectors from their doors – we will see bankruptcies. See – Un-Plugged: The Worst of The Drunken Sailors – Making Life Harder

- Issaquena Green Power, with its run-of-river hydropower concept, is slowly moving to the front of the starting blocks – see below.

Issaquena Green Power is in pre-development, but the design is simple, and the idea of high capacity-factor renewable power is very appealing for any industrial consumer adjacent to a large and fast-flowing river – the Mississippi, for example. We came to this project backwards, trying to identify where/how you could get enough cheap and high capacity-factor power to help large industrial operations and new projects. We are finding from conversations with C-MACC clients that there are many locations today where access to any renewable power is challenging, and many of these locations sit on the Mississippi River. New hydropower solves the additionality challenge, the temporal correlation, and the geographic correlation for green hydrogen simultaneously. While many of the companies we are talking to are trying to resolve other power need issues and will likely be the first customers for Issaquena Green Power, large-scale green hydrogen and its derivatives are a perfect fit with what we are developing, and there are plenty of unoccupied stretches of the Mississippi and other rivers in the US where it would make sense to produce hydrogen and derivatives – watch this space.

Separately, and as noted in other research, any change in Administration in the US may signal the end for green hydrogen. We suspect that the odds are high that 45V would be targeted by a Trump administration or even by a congress with Republican majorities. The Republicans are likely to support initiatives that support fossil fuels – CCS and low carbon fuel incentives – and dismiss anything that is direct competition – which green hydrogen would be.

News Update

Incentives/Policy

- TÜD SÜD unveils new standard for blue hydrogen and its derivatives

- COP28: Future hydrogen importers, exporters sign certification recognition statement

- Japan eyes launch of H2, NH3 subsidy scheme next summer

- COP28 hydrogen initiatives

Technology

Opinion

- Green Hydrogen Systems and GeoPura identify hydrogen challenges and opportunities

- Saudi Arabia’s $8bn Neom green mega-plant is no vanity exercise, says project chief

- EU Energy Outlook to 2060: power prices and revenues predicted for wind, solar, gas, hydrogen + more – Energy Post

Projects – Not included below.

- Lhyfe unveils 800MW green hydrogen project plans for Germany

- Samsung C&T to build South Korea’s first green hydrogen plant

- ACWA to develop largest green hydrogen facility in Indonesia

- Cepsa and C2X set up joint project to develop the largest green methanol plant in Europe

- GPCA 2023: Linde CEO flags FID early in 2024 for ASU, reformer at Dow net-zero Alberta complex

- COP28: Masdar, Verbund Green Hydrogen to explore development of green hydrogen plant in Spain

- Nearly 2,000 Hydrogen projects worldwide: IEA’s interactive tools give snapshot on progress, costs

- Sharjah NOC explores green hydrogen production in net-zero push

- CWP partners with Djibouti government to speed up 5-10 MW green hydrogen project

- JCB Unveils Rs 700 Crore Hydrogen Project in Grand Indian Debut

Transport

- Azane Fuel Solutions and Amogy Ink Deal for Ammonia Bunker Vessel (chemanalyst.com)

- Maersk Tankers Secures Order for Up to 10 Ammonia Carriers in South Korea

- North Sea Container Line (NCL) and Yara plan ammonia-fueled containership

Other

- Poppe + Potthoff names hydrogen supply systems TOPAQ

- COP28: Global hydrogen trade initiatives launched

- Adnoc, Mitsubishi to Partner on Hydrogen, Ammonia Projects

- NWTN Announces Strategic Partnership with China State Construction Engineering Corporation (Middle East)

Detailed Projects Update

Each week we will take projects that have hit our radar in the last 7 days and show the success factors that would be needed to make each successful. This week we have fewer projects and as some of the power challenges are recognized around the world, we may see the project list identified by the IEA list highlighted above shrink rather than grow from here – we will see new projects added but others will likely fall off the list, assuming that the IEA focuses on projects that are active.

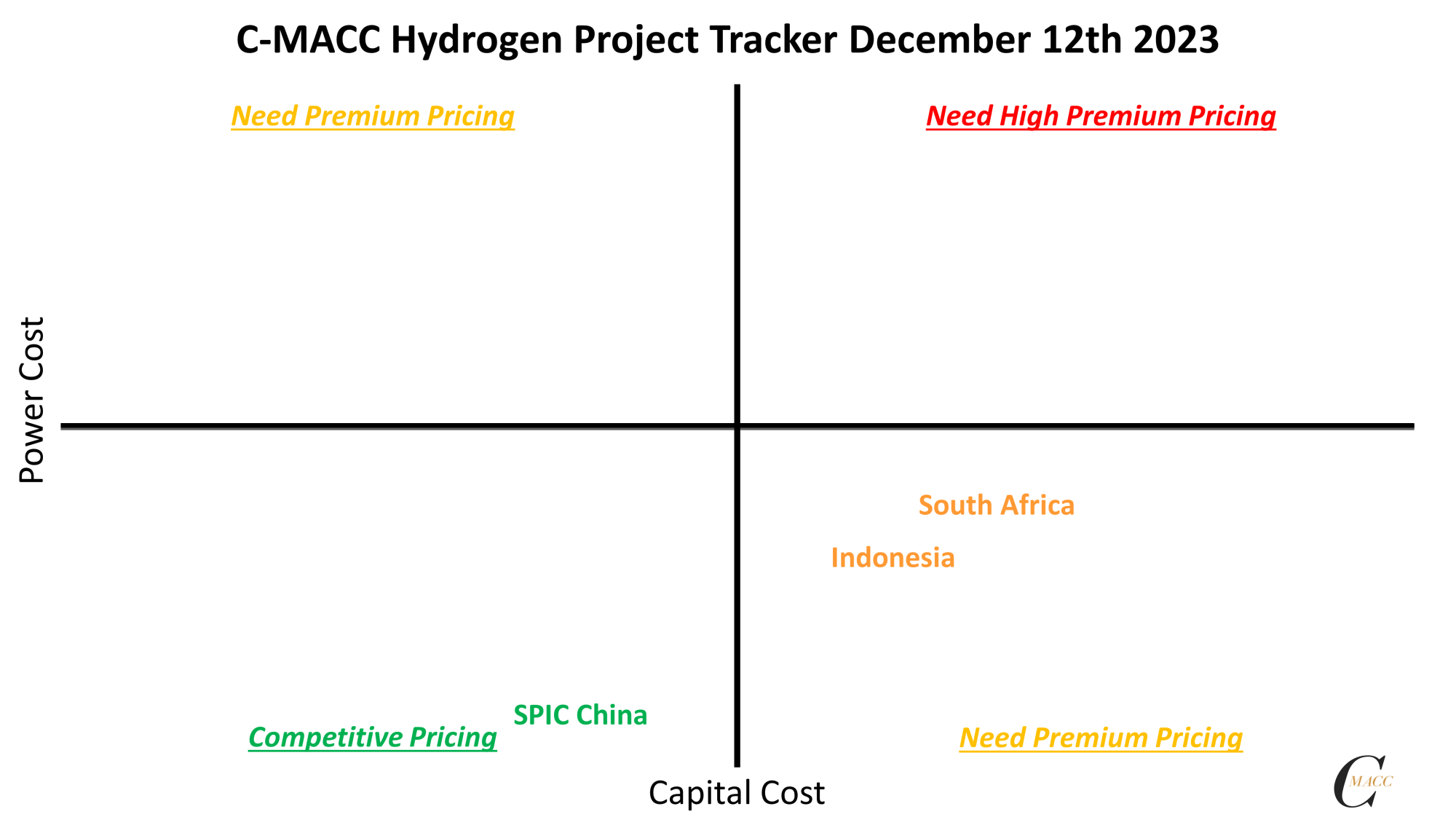

Acwa Power signs deal to develop the largest Green Hydrogen Project in Indonesia

- Saudi-listed ACWA Power is set to develop the largest green hydrogen facility in Indonesia with PT Perusahaan Listrik Negara (PLN) with Indonesia’s state-owned electricity provider and PT Pupuk Indonesia, a state-owned fertilizer and chemical producer.

- Garuda Hidrogen Hijau (GH2) Project is expected to start commercial operations in 2026.

- It will run on 600MW of solar and wind power, and will produce 150,000 tonnes of green ammonia per year.

- The project’s cost is estimated to be upwards of $1 billion.

The math is wrong with this announcement, as 600MW of power will only get you to around 60% of the production suggested, and that is assuming a 100% capacity factor. To get 150,000 tons of hydrogen, the most efficient solid oxide system above would need 750MW of 100% capacity factor power or 1.1MW of power for alkaline technology. Given the wind and solar mix, you need 3x minimum of the power capacity plus storage. This setting suggests that the power measure is off by as much as 75% – should be closer to 2.5MW –or the production will be lower. Still, Indonesia should be a relatively low-cost power. In the report we published last week, we identified Indonesia as a possible location for cheap blue hydrogen – which could be much more cost-effective than the project here.

Exhibit 4: The Project Tracker Grid

Source: Corporate Reports and Announcements and C-MACC Estimates and Analysis

China’s SPIC plans $5.9 billion investment turning green hydrogen into fuel

- China’s State Power Investment Corp announced a 42-billion-yuan ($5.85 billion) investment plan in northeast China (Qiqihaer city, Heilongjiang province).

- It will produce fuel from hydrogen produced from wind power – the first of its kind in China.

- Include a 3.5-gigawatt wind power plant, a 164,000 metric ton per year hydrogen-making facility, and 400,000 tpy each of sustainable aviation fuel (SAF) and methanol.

- SPIC will first build a 10,000-tpy pilot plant making SAF from wind power-based hydrogen applying technology from Tsing Energy Development Co.

- The SAF plant is slated for its first fuel in late 2025, according to experts.

The renewable power surplus in Northeast China is growing, and it is creating some curtailed power, which, if used in this project, could result in near-zero prices for the power. The announcement’s ratio of wind power to hydrogen is appropriately conservative and suggests the use of power at off-peak times. This will be a very low cost with the challenge of getting the fuels to distant markets in China, assuming there is insufficient local consumption. This area is one of the very few locations in the world where we expect to see the production of very low-cost green hydrogen.

Itochu and Hive to collaborate on green ammonia project in South Africa

- ITOCHU and Hive will cooperate on the green ammonia production project in Coega, Nelson Mandela Bay, the Eastern Cape province in the Republic of South Africa.

- Scheduled to be commissioned in 2028, the plant will supply Japan, Korea, and Europe with over 900,000 tons annually in the first of four phases.

- Hive is confident that its green ammonia pricing for pre-2030 supply will be one of the lowest in the world.

This should be a relatively attractive project if the capital costs can be kept under control, but it may fall foul of one of the issues we discussed last week, which is the dedicated use of renewable power at low prices for industrial projects, when the power may be of more value to residential customers or industrial users in more labor-intensive industries – so good for jobs.

Ammonia/Methanol Update

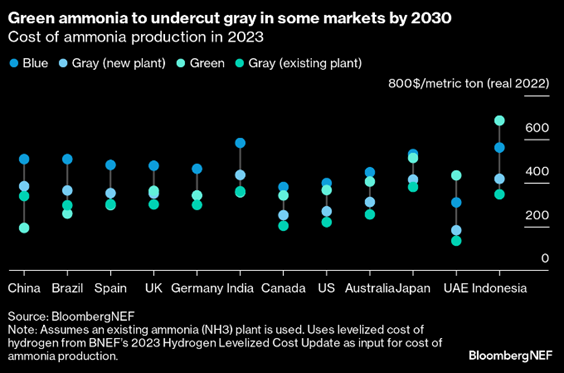

Based on the analysis above for the US and our views of higher power costs outside the US – except in China, we see no way in which the chart below can be correct. See our research, The Cost Of Developing Hydrogen Vectors Without Blue Is Too High, highlighting that wherever carbon capture and storage are possible, blue hydrogen (and ammonia) will likely be cheaper than green. It is also the only near-term option to develop scale for CO2-free product generation alongside their likely increased consumer acceptance. Though we see examples of infrastructure sharing and repurposing to reduce the time and cost associated with new construction, such as locating hydrogen electrolyzers near existing gray ammonia plants and converting gray ammonia facilities to blue and the eventual retiring of some gray production for green, we see blue production growing volume faster than green near term.

Exhibit 5: Bloomberg estimates green ammonia cost parity by 2030, assuming demand scales – see full paper in LINK.

Source: BloombergNEF, December 2023

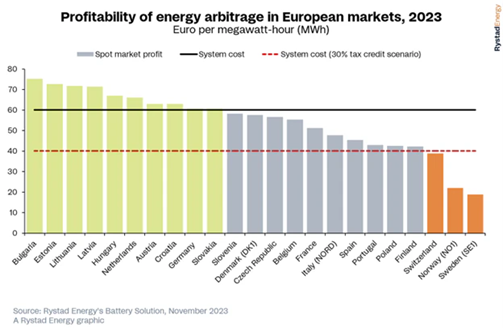

Power Update

Given the context of the report today, we show another example of something that is not economic and is sucking up government subsidies and taxpayers’ money. Several European countries have spot power prices that do not cover the cost of power generation and, in some cases, do not even cover a subsidized cost. If this power is then used to make expensive hydrogen, where either production or demand (or both) need subsidies, you end up with government-funded expenses that drive higher taxes and likely cause greater political friction, especially if one European country is seen to be subsidizing more than another, to the benefit of other countries. Power is a scarce resource globally, and it will be for many years. Using that power most effectively today means not subsidizing expensive green hydrogen, in our view, especially where you have a blue alternative.

Source: Rystad Energy, December 2023

See PDF for More Analysis in the Appendix

Loading…

Loading…