Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

- General Thoughts: Recent global polymer production cost curve steepening amid still weak demand and Chinese oversupply will hurt high-cost players, potentially forcing rationalization and positioning markets for a better 2026.

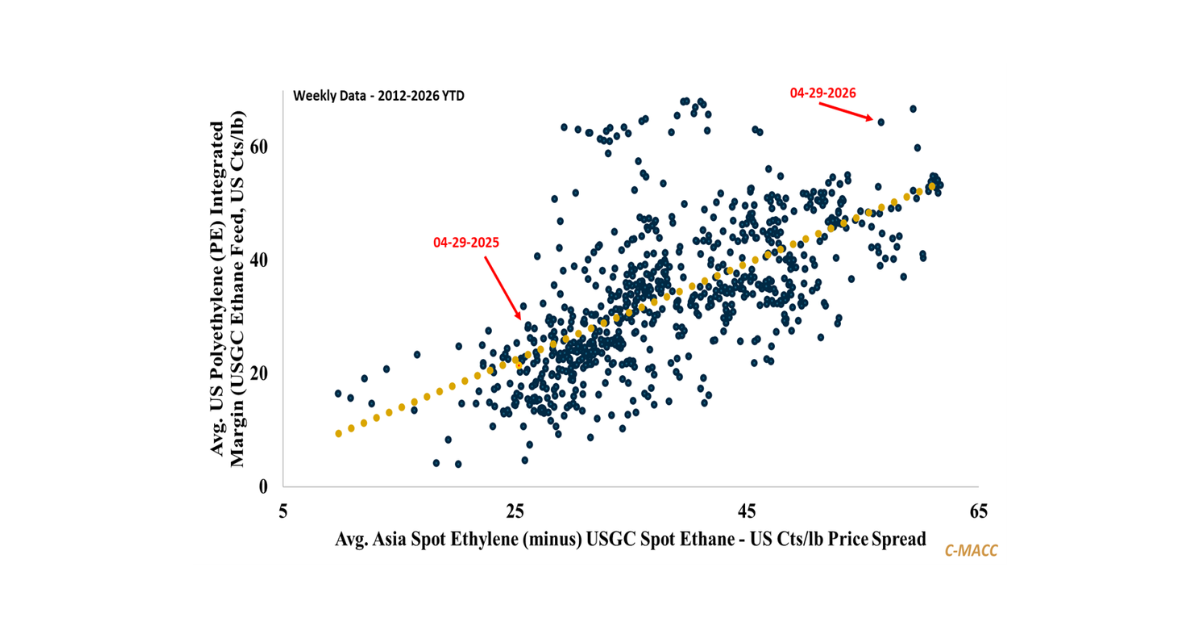

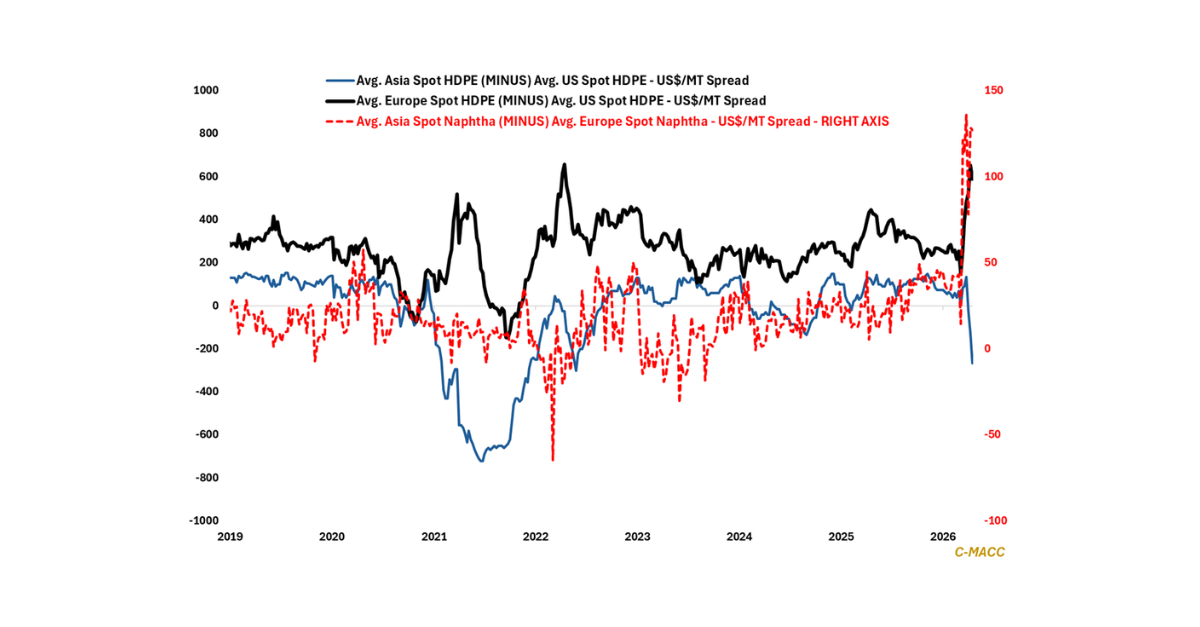

- Polyethylene (PE): Global PE markets face intensifying margin compression as US volume pressures Latin American arbitrage, Asia drifts despite pre-tariff buying, and Middle Eastern supply increasingly targets a saturated Europe.

- Polypropylene (PP): Global PP markets face mounting margin pressure as swelling Chinese supply, weak demand, and discounted cargoes pressure PP-to-PGP spreads, leaving integrated players best positioned for 2H25 volatility.

- Polyvinyl Chloride (PVC): Global PVC markets remain oversupplied and regionally fragmented. Chinese policy optimism lifts prices, US demand underwhelms, and trade frictions threaten supply chains absent better demand.

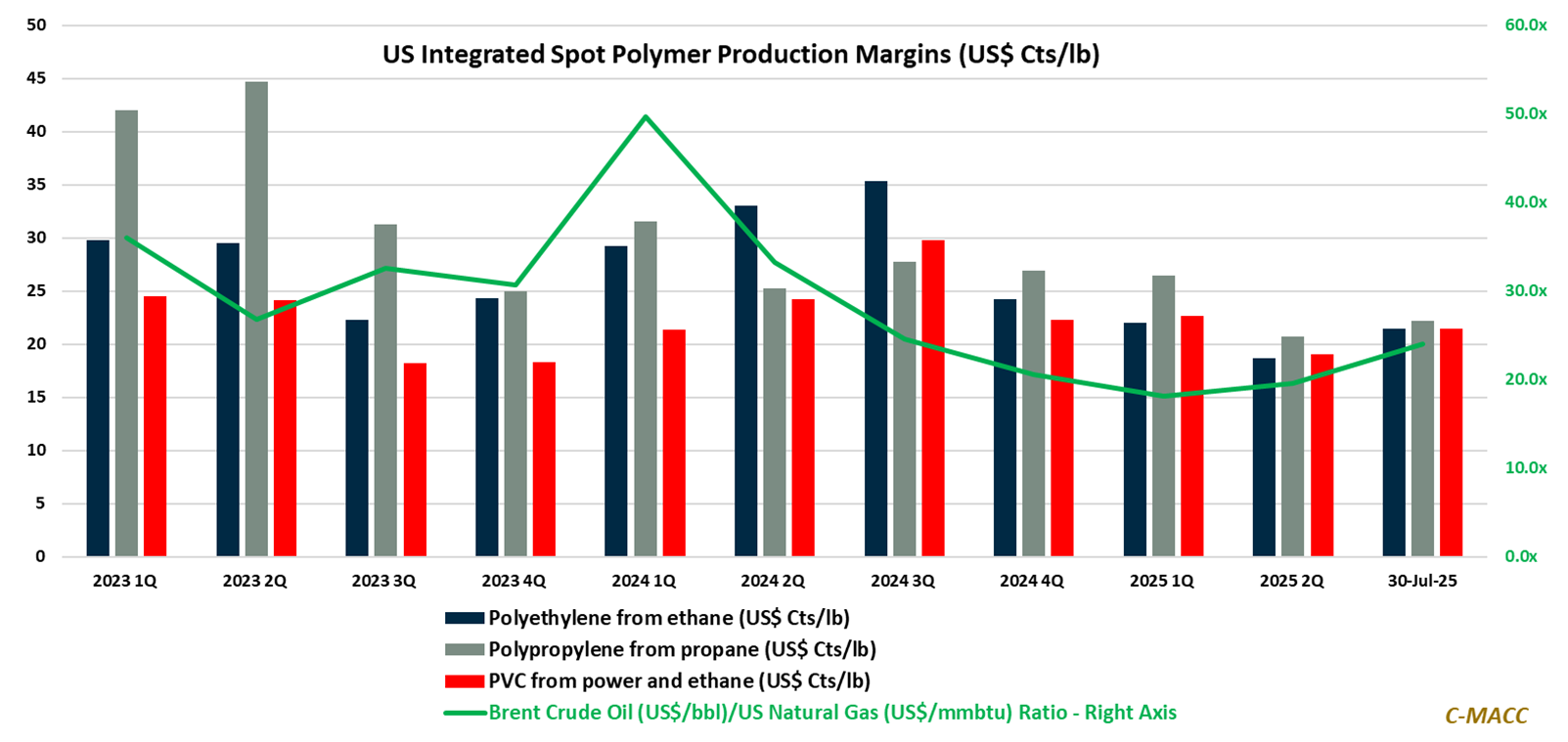

- Other Sector Developments: The strength in crude oil prices relative to natural gas relative to 2Q25 average levels has helped improve profits for US and Middle Eastern producers and lifted hopes for price improvement in 2H25.

Exhibit 1 – Chart of the Day: US integrated spot polymer margins have improved relative to 2Q25 average levels.

Source: Bloomberg, Company Reports, C-MACC Analysis, July 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!