Daily Chemical Reaction

Western Chemical Markets Reflect Tighter 1H24 Conditions Than Most Expected, 2H24 Likely to Be More Challenging!

Key Findings

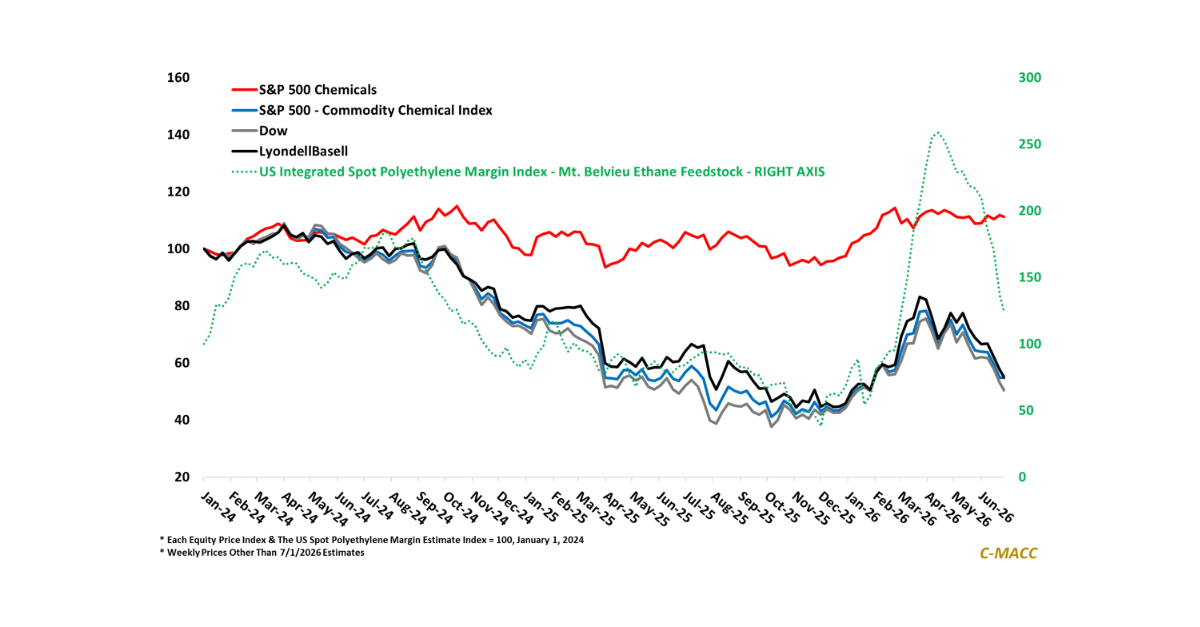

- General Thoughts: Western commodity chemical markets were tighter in 1H24, than most expected at its start because of a mixture of outages and global freight logistic issues – more volume will chase its high prices in 2H24.

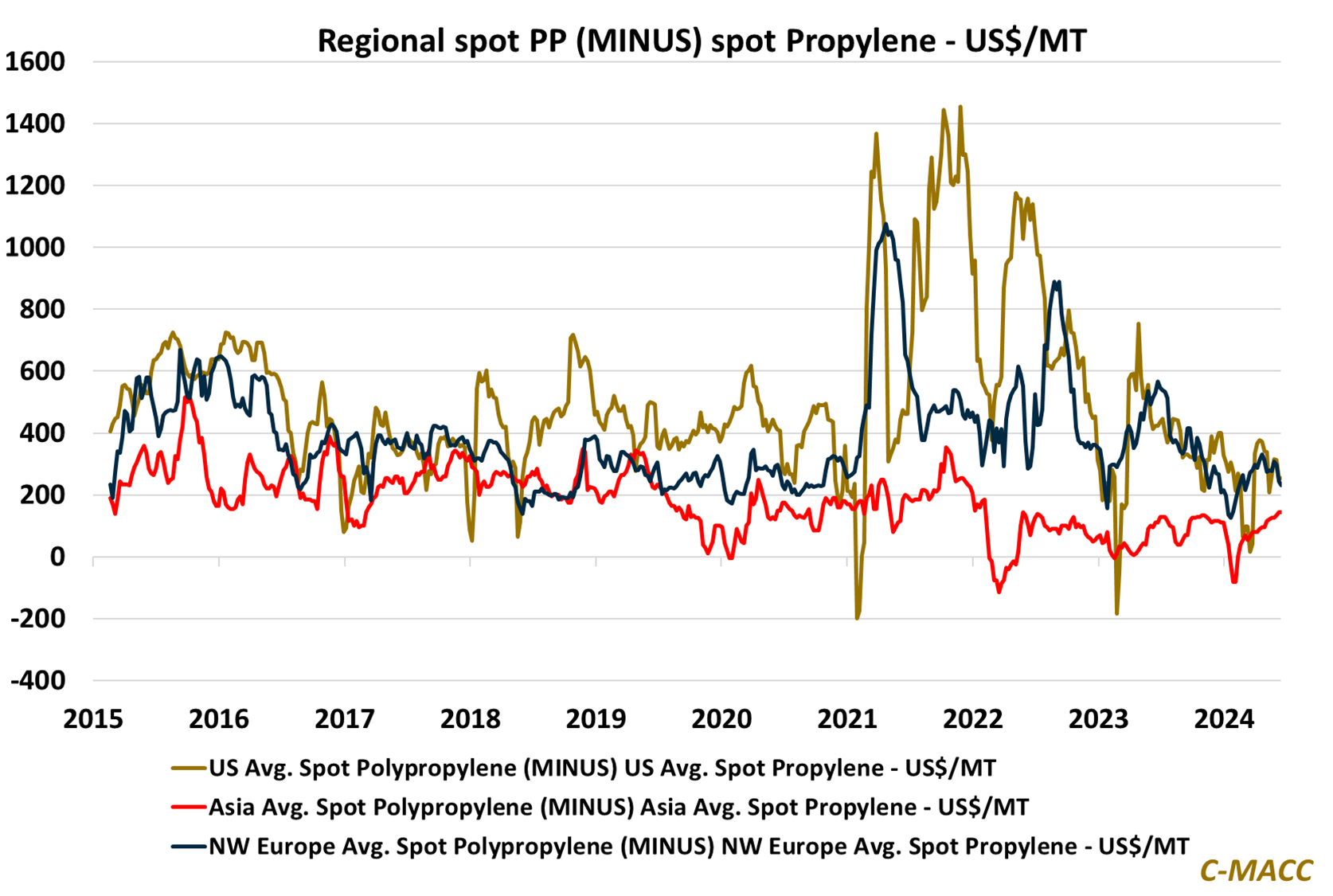

- Supply Chain/Commodities: We discuss the strength of US spot propylene values in June, as they exceed Europe and Asia levels, viewing it as an absolute and relative cost headwind for its non-integrated derivative producers.

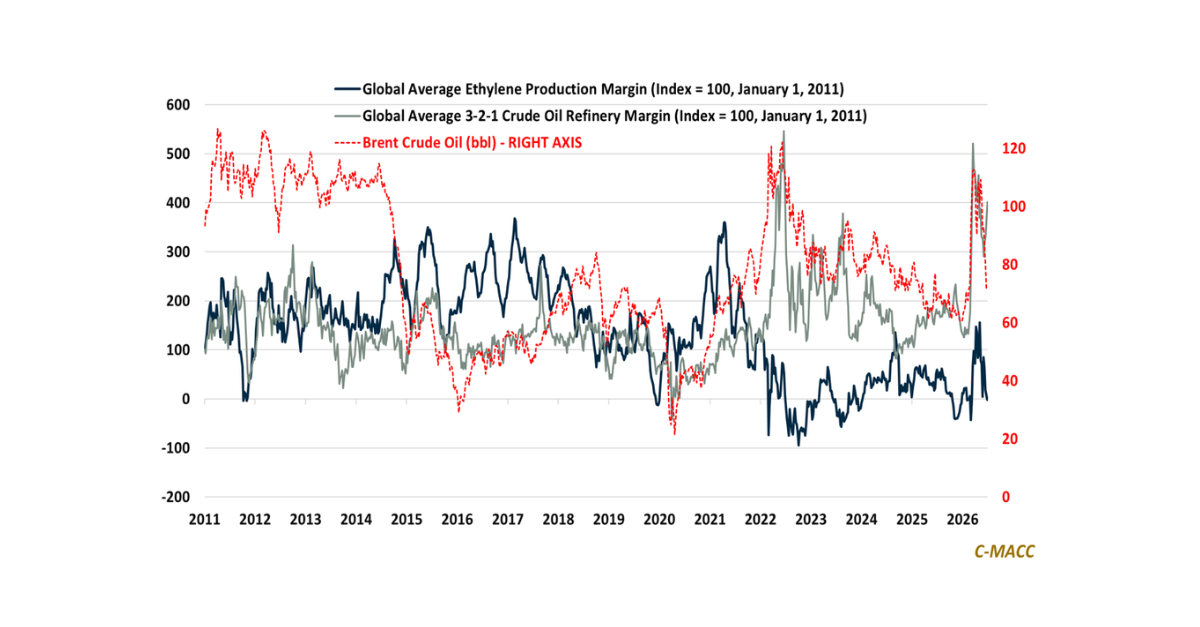

- Energy/Upstream: Recent strength in Brent crude oil, Ex-US naphtha, and propane relative to global natural gas prices and USGC ethane benefits some US chemical producers, such as in ethylene, compared to others in Europe.

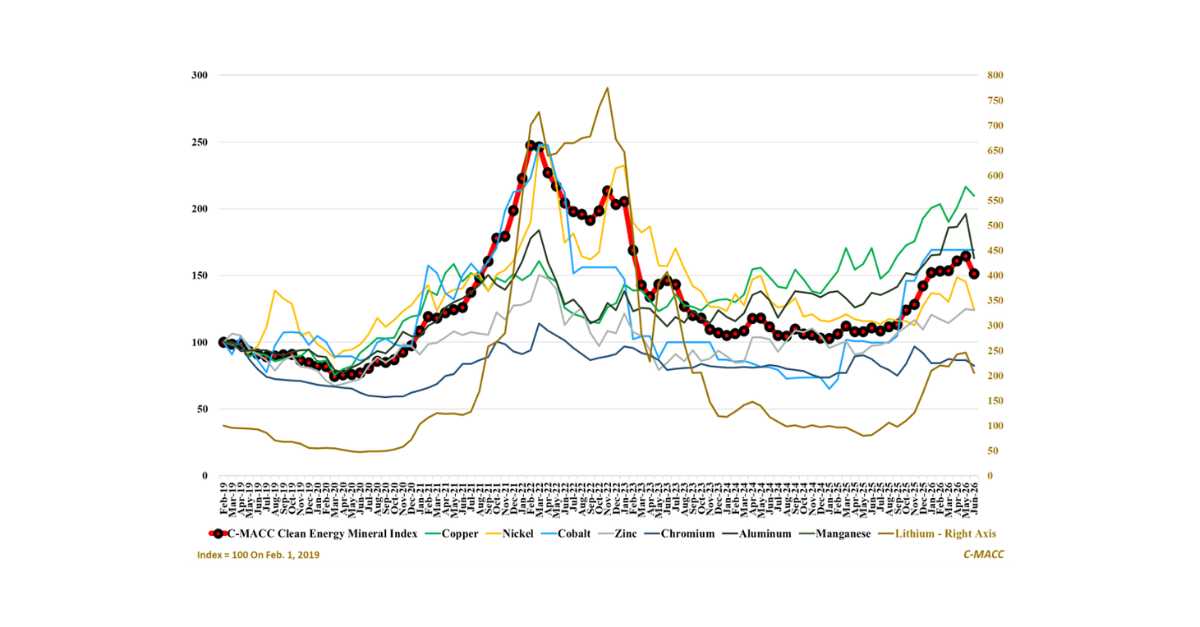

- Sustainability/Energy Transition: We discuss the surge in European (& global) clean steel investment and different clean steel production methods. We also highlight estimates for clean methanol production costs relative to gray.

- Downstream/Other Chemicals: North American chemical rail traffic is more robust than for most AAR sectors YTD relative to 2023, and we flag global container freight rate inflation YTD, adding to global product export costs.

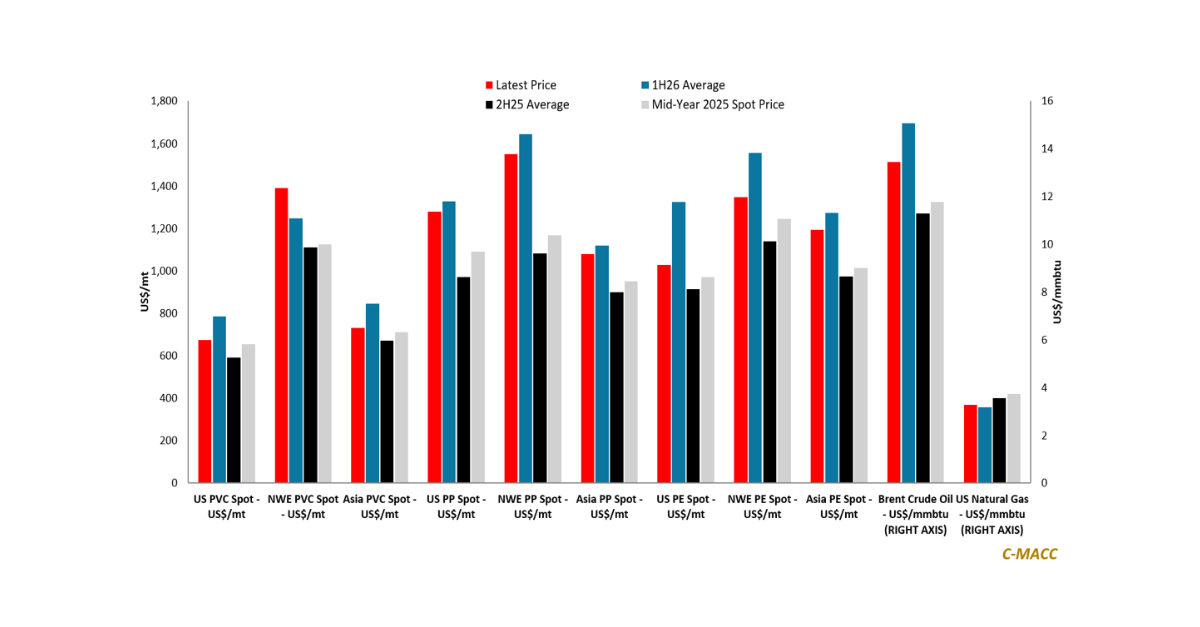

Exhibit 1: Western spot polypropylene (PP) prices remain at a premium to spot propylene compared to Asia.

Source: Bloomberg, C-MACC Analysis, June 2024

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!