Daily Chemical Reaction

European Chemical Industry Restructuring Far From Complete; Strategic M&A Activity To Stay Selective

Key Findings

- General Thoughts: We discuss ADNOC’s announced acquisition of Covestro amid an ongoing European chemical sector restructuring that is far from complete, with some portions needing much more restructuring than others.

- Supply Chain/Commodities: We highlight the US and Middle East petrochemical production cost advantage relative to Europe and flag domestic PE and PVC markets among polymer markets most at risk from US port strikes.

- Energy/Upstream: We discuss the 45v tax incentive and the power additionality requirements for green hydrogen production – we see it as fair to have the same additionality logic applied to data centers amid surging demand.

- Sustainability/Energy Transition: We discuss European efforts to limit Chinese electrolyzer capacity in its second EU hydrogen bank auction, among other factors that differ from its first auction and are likely to drive up costs.

- Downstream/Other Chemicals: We discuss weak European manufacturing data and price expectations, highlight global freight rate trends ahead of the US port strike, and comment on EU market risks from international trade.

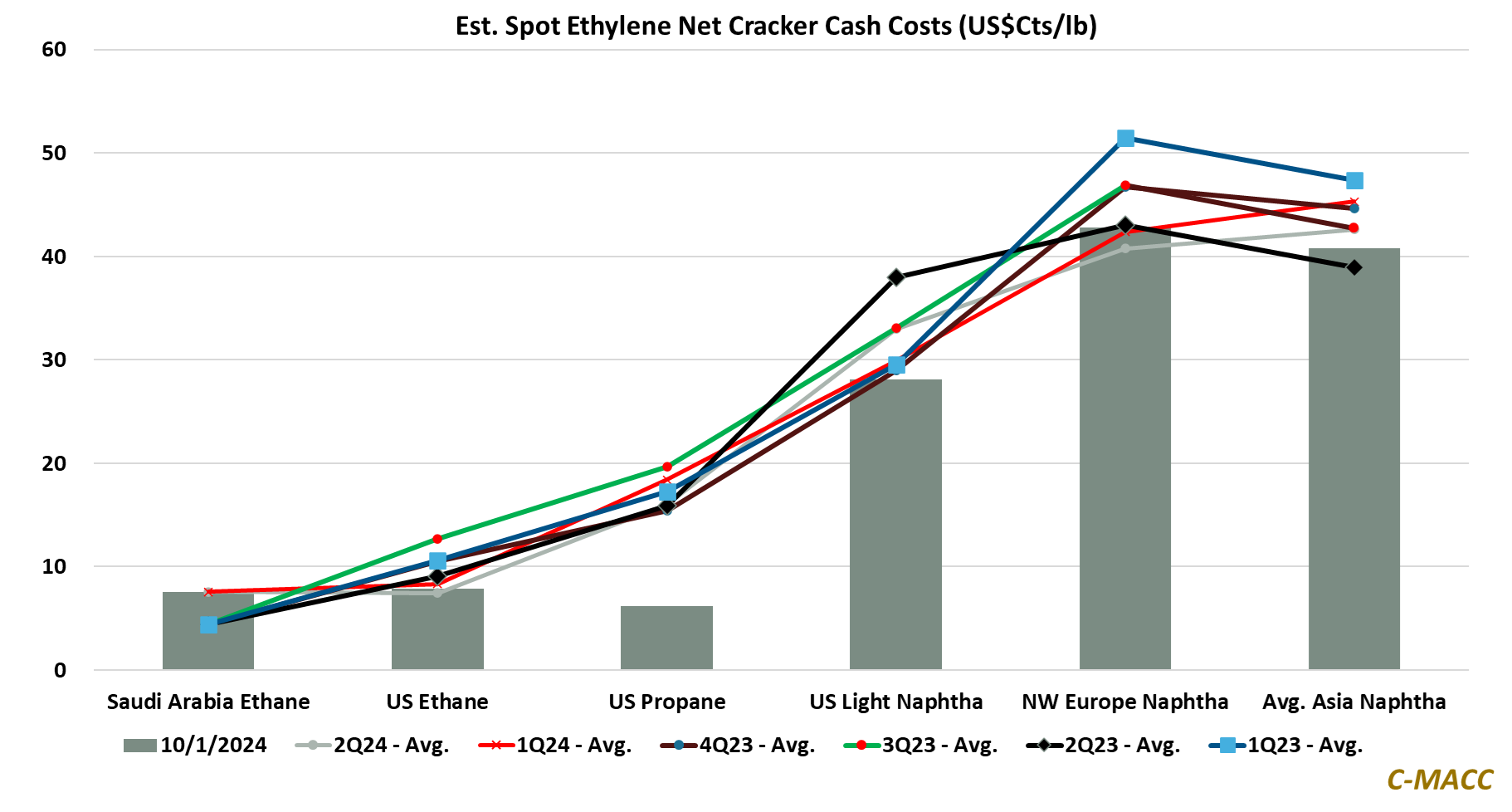

Exhibit 1: European ethylene production costs reflect some of the highest levels globally, making many of its ethylene (and other petrochemical production assets) a restructuring, closure, or backward integration target.

Source: Bloomberg, C-MACC Analysis, October 2024

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!