Global Market Analysis

You Can’t Hurry Consumption: 2Q Gains Face a Tougher Second Half as Power Cuts the Line

Key Findings

- General Thoughts: Company-specific pricing, cost timing, and supply advantages lifted 2Q26 results before end demand improved, leaving 2H26 performance exposed to higher inputs and normalized competition.

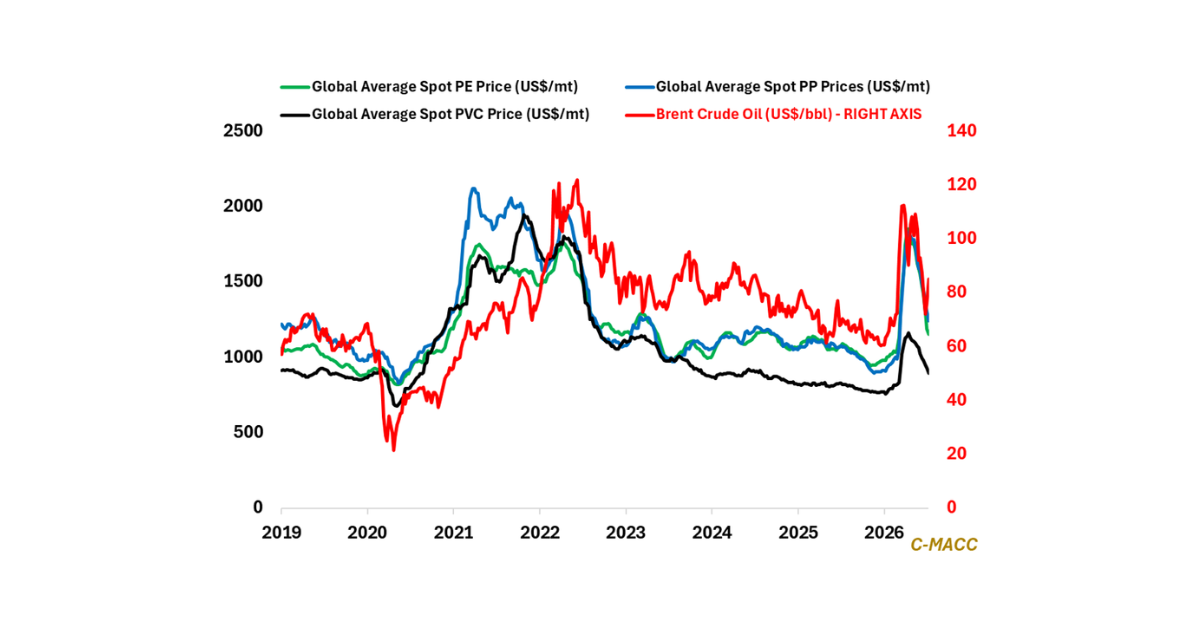

- Supply Chain/Commodities: Butadiene should find support as feedstocks rebound, limiting tiremaker relief and making price retention critical as European tariffs redirect Chinese competition toward other markets.

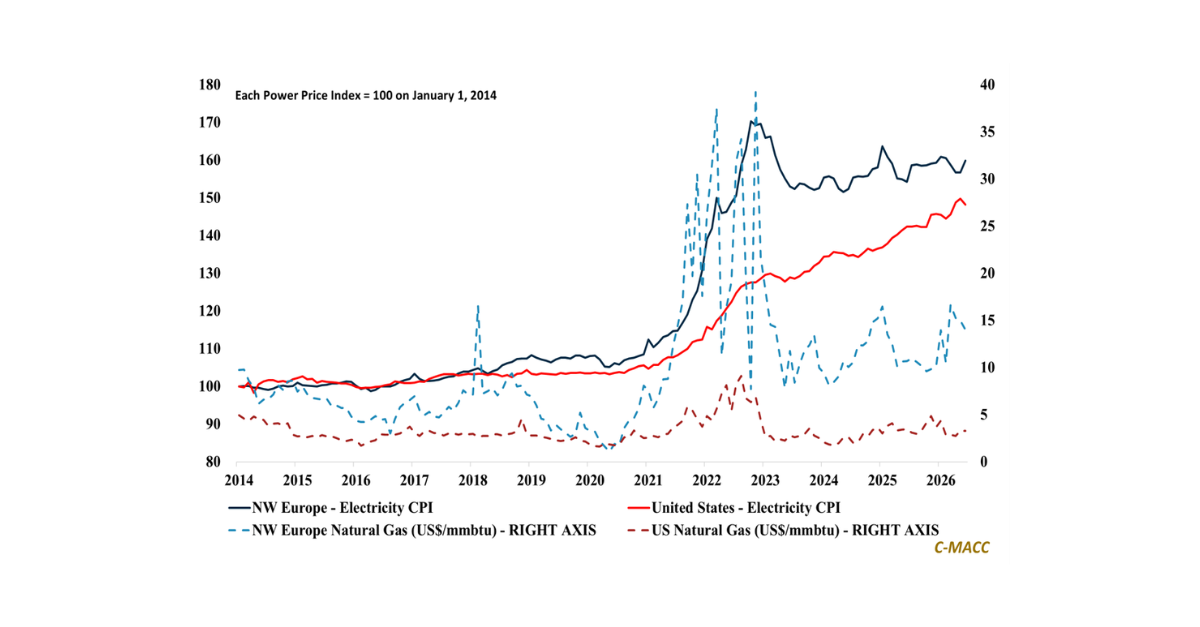

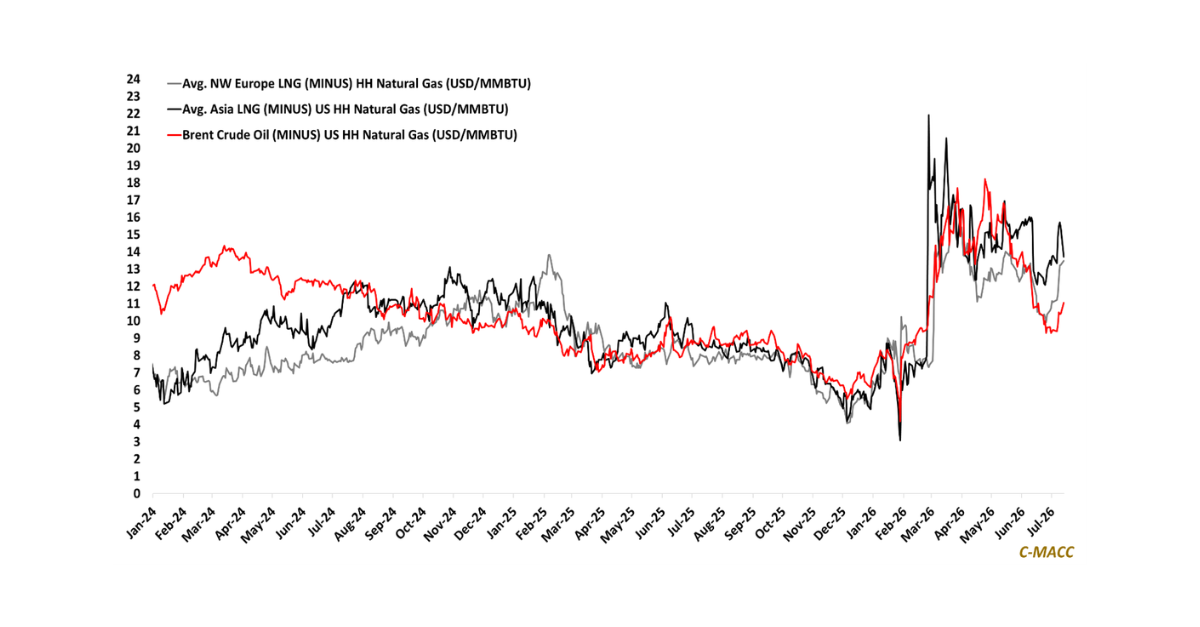

- Energy/Upstream: Europe’s 2Q26 naphtha advantage over Asia has faded, but renewed Gulf disruption could reopen the gap, leaving Asian crackers exposed as refinery runs and cargo access tighten supply.

- Sustainability/Energy Transition: Hydrogen development favors smaller projects with committed buyers, as cheaper electrolyzers fail to rescue oversized projects burdened by poor power economics and utilization.

- Downstream/Other Chemicals: ABB’s 2Q26 backlog shows spending favoring power access, widening the earnings gap between electrical suppliers and automation vendors facing slower process investment.

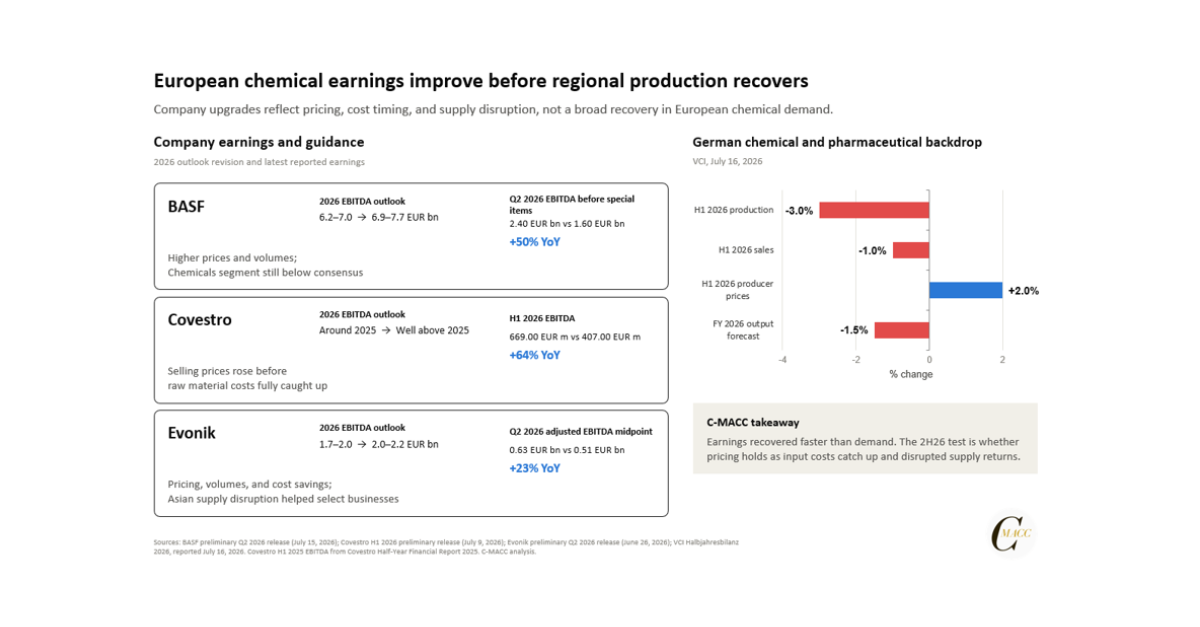

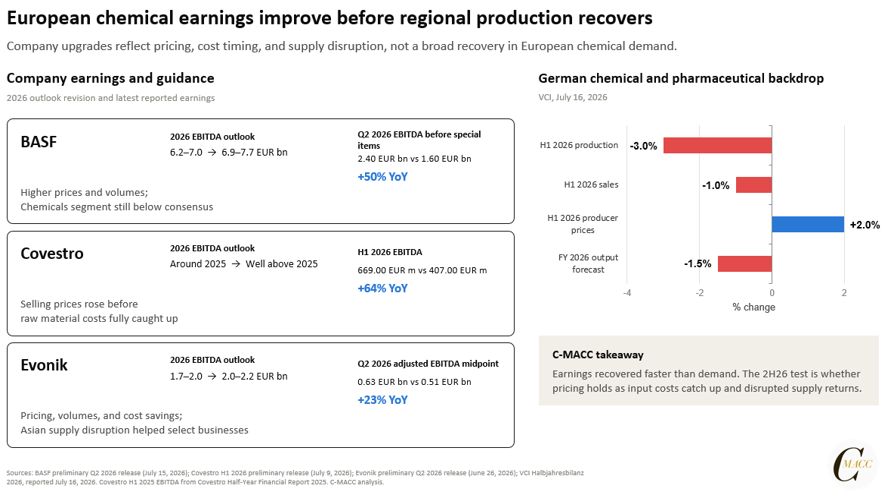

Exhibit 1: European Chemical Companies See 2Q26 Earnings Improve Before Regional Demand Recovers.

* Company upgrades reflect different pricing, cost, volume, and supply effects despite continued weakness in German chemical and pharmaceutical output. Source: Company Reports, VCI, C-MACC Analysis, July 2026

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!